Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2026 edition covers Market Review for the year 2025, some long-term themes that drive investments, and how to achieve a balanced approach to wealth and health. Shiuman’s Corner covers the books I read last year.

Markets

Market scorecard as of close on Friday March 13, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 32,542 | -1.6% | 2.6% |

| U.S. | S&P 500 | 6,632 | -1.6% | -3.1% |

| U.S. | NASDAQ | 22,105 | -1.3% | -4.9% |

| Europe/Asia | MSCI EAFE | 2,933 | -1.1% | 1.4% |

Source: FactSet

- TSX finished sharply lower on Friday, near worst levels. Sectors mixed. Materials the outsized decliner weighed by precious metals prices. Canadian equities finished down 1.64% on the week.

- US equities were lower in Friday trading. Stocks ended near worst levels after reversing earlier gains following latest hawkish Iran updates; S&P 500 finished at lowest level since November. S&P 500 is down 1.6% for the week.

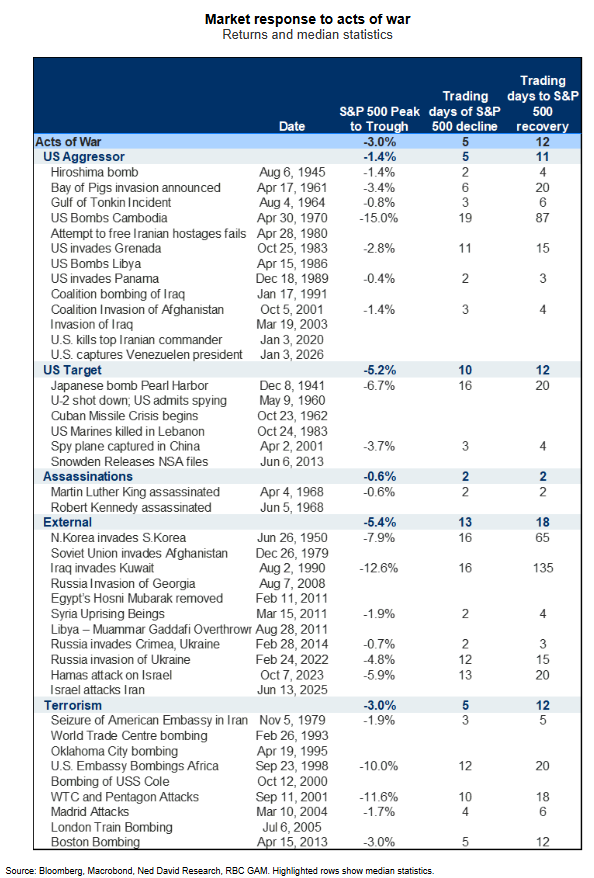

- The conflict in the Middle East materially increased geopolitical risk and injected renewed volatility into financial markets. Equity markets retreated and bond yields edged higher in response to a sharp rise in energy prices amid worries of supply disruptions tied to a potential prolonged closure of the Strait of Hormuz—one of the world’s most critical energy transit routes.

- While geopolitical shocks often generate short-term market turbulence, occasionally severe, they have historically had limited influence on longer-term market direction. Across roughly two dozen significant military conflicts since 1950, the S&P 500 delivered positive returns twelve months later nearly three-quarters of the time.

-

- ECONOMY

- Canada

- As a major oil exporter, Canada is better positioned than global peers to weather higher crude prices, in our opinion, though the broader economic impact is mixed. Higher oil prices support energy producers and government revenues, but they also raise gasoline and transportation costs for households, which may prompt reduced spending elsewhere in the economy and potentially dampen sentiment.

- Prime Minister Mark Carney used a recent Indo-Pacific visit to deepen Canada’s strategic ties with both Japan and Australia, signaling a broader effort to diversify economic and security partnerships.

- Headline inflation slowed to 1.8% in February, though comparisons remain distorted by last year's GST/HST holiday (which extended through mid-February) biasing food prices higher, and the removal of the consumer carbon tax in April 2025, which depressed energy CPI. At this week's meeting, we expect the BoC to recognize growing external uncertainty but continue to hold the overnight rate at its current, borderline accommodative level of 2.25%.

U.S.

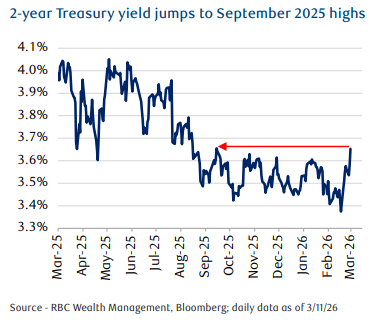

- This month’s slump in Treasury prices raised yields on key benchmark maturities to multi-month highs—particularly the policy-sensitive 2-year yield after recently striking the highs from September 2025. The sudden resurgence in inflation expectations has revamped the market’s outlook for rate cuts by the Federal Reserve.

-

Further Afield

- RBC Global Asset Management calculates that a permanent US$40 increase in oil prices to around US$105 per barrel—with the additional impact from a similar rise in natural gas prices—would initially subtract some 0.8% from eurozone GDP. Inflation in the eurozone could rise by around 1.5 percentage points because of higher energy costs. Both effects would likely be somewhat smaller for the UK.

- Interest rate expectations have shifted following the conflict. Markets now price in one rate hike in Europe (from none previously) and no cuts in the UK (versus two priced in at the end of February).

- Japan and South Korea respectively import over 90% and 70% of their oil from the Middle East, and most of these shipments transit through the Strait of Hormuz. However, both countries have built substantial strategic buffers, with Japan holding around 250 days of reserves and South Korea around 200 days.

Notes About Companies in Model Portfolio

- Costco Wholesale Corporation (Nasdaq: COST) today on March 5 its operating results for the second quarter (twelve weeks) and the first 24 weeks of fiscal 2026, ended February 15, 2026. Net sales for the first 24 weeks increased 8.7 percent, to $134.22 billion, from $123.52 billion last year. Net income for the first 24 weeks was $4.04 billion, $9.08 per diluted share, compared to $3.59 billion, $8.06 per diluted share, last year.

- Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.