Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q4 2025 edition covers Market Review up to Q3 of 2025, the Artificial Intelligence (AI) boom and gold’s surge. Shiuman’s Corner is a about my cycling adventures for fund raising.

Markets

Market scorecard as of close on Friday January 2, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 31,883 | 0.5% | 0.5% |

| U.S. | S&P 500 | 6,858 | 0.2% | 0.2% |

| U.S. | NASDAQ | 23,236 | 0.0% | 0.0% |

| Europe/Asia | MSCI EAFE | 2,910 | 0.6% | 0.6% |

Source: FactSet

- The first day of trading in 2026 ended slightly positive (see above table).

Market scorecard for the year 2025:

| Equity Indices | Level | 2025 |

| S&P/ TSXComposite | 31,713 | 28.2% |

| S&P 500 | 6,846 | 16.4% |

| NASDAQ | 23,242 | 20.4% |

| MSCI EAFE | 2,893 | 27.9% |

- Overall, returns for global stock markets were strong in 2025 (see above table). For only the third time in the past decade, the Canadian S&P/TSX Composite Index outperformed the S&P 500 Index (U.S.).

- Excerpts from the Global Insight 2026 Outlook by the RBC Global Portfolio Advisory Committee:

-

- Artificial intelligence is likely to remain a central theme for decades.

- The bond market may remain more alert to fiscal excesses, leading to a relatively steep yield curve.

- The U.S.’s economic growth advantage could erode as immigration declines and other public policy decisions undermine some fraction of long-term growth.

- The stock market could generate more modest returns given limits to how much further valuations and profit margins can rise from current levels.

- We think “positive” rather than “above average” is the outcome to plan for. The “positive returns” outcome depends on the major economies, especially the U.S., avoiding recession and the current consensus forecast for GDP, earnings growth, inflation, and interest rates to be close to consensus forecasts.

ECONOMY

Canada

- Canadian headline inflation remained unchanged at 2.2% y/y in November, slightly below consensus expectations. The Bank of Canada’s (BoC) preferred core inflation measures—median and trimmed-mean CPI growth—also showed signs of easing, both coming in at 2.8% y/y, below consensus expectations.

- BoC Governor Tiff Macklem said the central bank is preparing for its 2026 monetary policy framework review. Speaking in Montreal at his year-end address, Macklem said the BoC does not plan to reconsider its 2% inflation target but acknowledged that shifting global conditions are increasing policymaking complexity.

U.S.

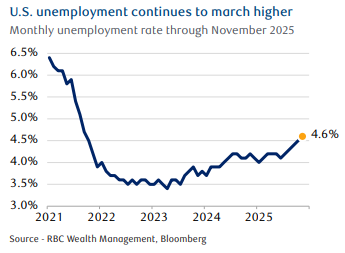

- Economic data released on Tuesday by the Bureau of Labor Statistics (BLS) revealed more evidence of a cooling labor market as the U.S. unemployment rate continued its upward climb in November, increasing to 4.6% from 4.4% in September (due to the government shutdown, no unemployment rate was released for October).

- November’s U.S. inflation data showed prices increasing at the slowest annual pace since early 2021, a significant improvement following months of persistent price pressures. The Consumer Price Index (CPI) climbed 2.7% from a year ago, while core CPI, which excludes food and energy prices, rose 2.6%.

- Further Afield

- The European Central Bank (ECB) held its key interest rate at 2%, as widely expected. The ECB’s December staff forecasts compared to September showed upward revisions to 2025–2027 GDP growth estimates that were driven by domestic demand, especially in the private sector.

- In China, sentiment in the property sector soured again on the back of weak November data. New home prices dropped 0.39% month-over-month, real estate investment fell 30% y/y, and new home sales contracted 28% y/y.

NOTES ABOUT COMPANIES IN MODEL PORTFOLIO

- Berkshire Hathaway (BRK.A/BRK.B) announced Friday it has completed the acquisition of OxyChem from Occidental for $9.7 billion, subject to customary post-closing purchase price adjustments. OxyChem is a leading producer of essential chemistry with operations in the U.S., Canada and Latin America.

- Warren Buffett wrote on November 10, 2025:

-

- “I will no longer be writing Berkshire's annual report or talking endlessly at the annual meeting. As the British would say, I'm 'going quiet. Sort of.

- Greg Abel will become the boss at year end. He is a great manager, a tireless worker and an honest communicator. Wish him an extended tenure.

- I will continue talking to you and my children about Berkshire via my annual Thanksgiving message. Berkshire's individual shareholders are a very special group who are unusually generous in sharing their gains with others less fortunate. I enjoy the chance to keep in touch with you. Indulge me this year as I first reminisce a bit. After that, I will discuss the plans for distribution of my Berkshire shares. Finally, I will offer a few business and personal observations."

Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.