Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q4 2025 edition covers Market Review up to Q3 of 2025, the Artificial Intelligence (AI) boom and gold’s surge. Shiuman’s Corner is a about my cycling adventures for fund raising.

Markets

Market scorecard as of close on Friday January 9, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 32,613 | 2.3% | 2.8% |

| U.S. | S&P 500 | 6,966 | 1.6% | 1.8% |

| U.S. | NASDAQ | 23,671 | 1.9% | 1.8% |

| Europe/Asia | MSCI EAFE | 2,951 | 1.4% | 2.0% |

Source: FactSet

- TSX finished higher on Friday, bit off best levels. Most sectors higher. Canadian equities finish the week up 2.3%, at new all-time highs.

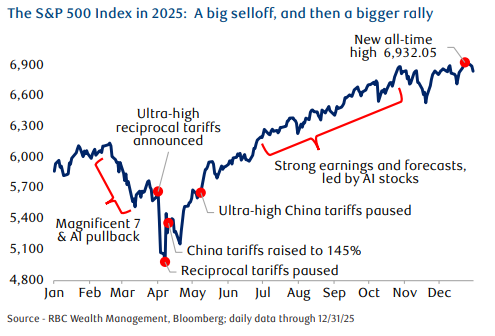

- US equities were higher in Friday trading as stocks ended just off best levels. S&P 500 set a fresh record close and Nasdaq a little over 1% off its record, as both indexes capped of third week higher in past four.

- The U.S. equity market delivered its third straight year of double-digit and above-average gains, with the S&P 500 rising 17.9 percent including dividends in 2025, boosting the total return to 100.6 percent since this bull market began in October 2022 through the end of last year.

-

- Seven stocks represented just over half of the S&P 500’s gains in 2025: NVIDIA, Alphabet, Microsoft, Broadcom, JPMorgan Chase, Palantir Technologies, and Meta Platforms. All of these stocks—even banking behemoth JPMorgan Chase—have at least some exposure to the AI theme.

- This group punched well above its weight. While these seven stocks represented 25 percent of the S&P 500’s market capitalization last year, they accounted for 52 percent of the index’s total return.

- Excluding the Tech sector, the rest of the S&P 500 grew earnings by an average of 9.8 percent from Q1 through Q3 2025—a pretty good clip considering there were tariff headwinds during that period.

- With the U.S. market’s three-year winning streak in the books, it’s only natural to question whether the rally can be extended.

- Since 1945, the S&P 500 has delivered back-to-back above average gains for three or more consecutive years on five other occasions (not counting this cycle), including one streak that ran for four years and another for five.

ECONOMY

Canada

- Employment grew by just 8,000 in December, following a robust 181,000 increase over the prior three months. The unemployment rate rose to 6.8% from 6.5%, driven primarily by a jump in the share of the population looking for work rather than an increase in layoffs. Even at 6.8%, the rate remains below October’s 6.9% and September’s recent peak of 7.1%.

- In 2026, this recalibration of in-migration volumes and types will be a dominant theme. We expect year-over-year population growth to be flat. That’s below the pre-pandemic average of 1.1%, and significantly lower than the nearly 3% growth experienced in 2023 and 2024, which overwhelmed the economy’s ability to absorb it.

U.S.

- The labor market ends 2025 on better footings than previously thought. The unemployment rate unexpectedly ticked down to 4.4% in December as the economy added 50k jobs. Notably, October saw a sizable downward revision (from -105k to -173k) suggesting the government shutdown had a larger impact on hiring activity than previously estimated.

- U.S. prosecutors are investigating whether Fed Chair Jerome Powell lied to Congress about the US$2.5 billion renovation of the central bank’s Washington headquarters. A long running feud between Donald Trump and Powell has unnerved many investors looking for a politically neutral central bank. On Sunday, Powell issued his own video questioning the motivations behind the investigation. Trump, who nominated Powell during his first term, has regularly threatened to fire the chair for not following his demands to slash interest rates.

- This week is packed with data – front and center will be December CPI data, the final reading of 2025 reporting ahead of the next Fed meeting.

Further Afield

- Mark Carney heads to Beijing looking to “elevate engagement.” Trade, energy, agriculture and security will all be on the agenda when the Prime Minister meets Chinese President Xi Jinping this week as part of his five-day visit to China.

Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.