As we turn our calendars to a new year, it is natural to reflect on the past 12 months and assess how our perspectives shaped our decisions. For investors, one mindset worth examining is the Negativity Bias – the tendency to focus more on bad news than good. This bias explains why many are likely surprised by 2025’s strong market performance. Despite worries over US trade policy, ongoing geopolitical conflicts, persistent albeit softening inflation, and talk of AI stock bubbles, the S&P 500 and TSX indices rose 16% and 28%, respectively.

Amid the negative headlines, several softer-spoken yet powerful tailwinds were often overlooked. Despite trade tensions and inflation fears, the U.S. economy grew a respectable 2%, corporate profits rose 11%, and interest rates trended lower. These important fundamentals didn’t shout for attention – they simply delivered another year of strong results.

Four-in-a-row Too Much to Ask?

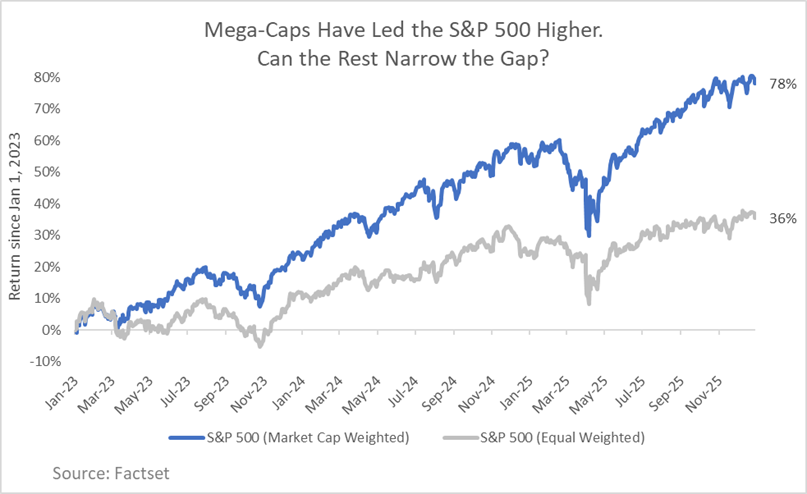

The S&P 500 has now risen at least 15% for three consecutive years. Those with a strong Negativity Bias may argue that this streak means we are overdue for a bear market. History, however, provides a more mixed picture. While it is true that three +15% years from 2019 through 2021 were followed by a 19% decline in 2022, one should also recall the late 1990s when we experienced five consecutive years when the benchmark US index rose more than 19%!

An even more important fact to consider is that a lot of these gains were focused in the largest stocks in the market-capitalization-weighted index. The equal-weighted version of the S&P 500 index has only experienced gains of 9% - 12% in each of the past three years. This suggests that the average stock in the index is far from overextended. We are not suggesting that the large cap stocks need to retreat – this gap in performance could be narrowed if the rest of the market plays catch up.

Few Bear Market Signs Ahead

Those that remain nervous should note that bear markets are generally triggered by one or more of the following: a significant spike in interest rates (think 2022), a recession (such as during the financial crisis), or some exogenous global events (e.g. the pandemic). While exogenous events are impossible to predict, central banks remain in a rate-cutting bias and the US economy is once again expected to post a 2% gain in 2026 (in part helped by the sizable Q1 tax refunds as a result of Trump’s One Big Beautiful Bill).

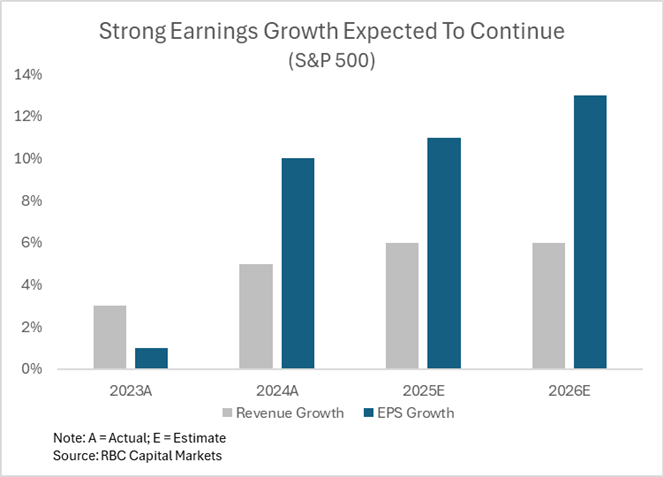

There is also the potential for further productivity gains as corporations deploy AI into their workflows. That was a key reason why corporate earnings growth was so strong in 2025 despite tariff and other headwinds. It may also be why analysts are expecting another strong year of growth in 2026.

Key Risks to Monitor

When pushing against the Negativity Bias, however, one should not become guilty of donning rose-coloured glasses. As such, we recognize several risks that could cause some normal volatility in the year ahead.

- AI-spending retreats. Some have estimated that capital outlays on data centers lifted the US economy as much as 1% in 2025. Some of this spending is from companies such as OpenAI, which are not yet generating the necessary revenue to cover these expenditures. Should this spending take a pause, it could expose areas weakness elsewhere in the economy. It could also further hurt shares of companies that supply hardware and services to the AI industry.

- Interest-rate surprise. While short-term interest rates continued to move lower in the closing weeks of 2025, longer-term interest rates actually rose. This could reflect several concerns. A stronger-than-expected economy and/or the delayed effects of tariffs cause inflation to increase. Some international investors may also be wary of adding to their US Treasury bond holdings at a time when the country’s debt continues to rise.

- Some signs of investor froth. While some measures of investor sentiment are neutral there are some signs of elevated bullishness, including very low cash levels amongst portfolio managers and high margin balances in brokerage accounts. These data points suggest we need to go through a period of selling pressure to normalize investor portfolios.

- US Election cycle. As we noted a year ago, the 12 months after a US presidential election tends to be very bullish for stocks. While markets experienced some policy-induced volatility in the Spring, the bullish post-election pattern still held. One risk for 2026 is that the 10 months leading up to the US mid-term elections (to be held in November) tends to be one of the weakest periods for stocks. The below chart shows the performance of the S&P 500 ahead of the past nine mid-term election years. Even if one ignored the three worst years (1990, 2002, 2022), which were impacted by recessions or an interest rate shock, most years experienced volatility heading into the elections. Encouragingly, one of the most bullish periods for stocks is the 12 months following the mid-term elections.

The Wall of Worry: Why Fear Fuels Market Gains

Paradoxically, the very concerns that may make investors anxious – interest rates, AI-spending bubble, mid-term elections – can collectively form a "Wall of Worry" that markets ascend rather than collapse under. This phenomenon occurs because pessimism keeps expectations subdued, preventing the complacency that often precedes bubbles (the act of many people worrying whether we are in an AI bubble may be what keeps a bubble from forming). When fears are widespread, even modest positive surprises (e.g., stabilizing rates, resilient tech demand, or bipartisan policy compromises) can chip away at the wall, propelling indexes higher as reality outpaces grim forecasts. History shows that markets often thrive in such environments.

Conclusion

After three consecutive years of strong equity returns, while risks are present, we do not see the requisite conditions for a bear market. As we navigate 2026, we will remain attuned to the interplay of human psychology and market fundamentals – mindful of the Negativity Bias that causes many investors to overlook opportunities. By focusing on measures of economic resilience and corporate earnings growth, we believe we can climb the Wall of Worry with discipline, transforming any market anxiety into advantage.

If you have any questions, please do not hesitate to Contact us!