This report is part of the “New normal, new opportunities” series, in which we examine secular trends in a post- COVID-19 world. The series will cover a range of themes that are emerging as a result of social distancing, the workfrom- home imperative, health care developments, corporate implications, and broader societal change. We believe identifying these trends and understanding their investment implications will be critical to navigating the road ahead. Additional reports will be released over the following weeks.

While the online facilitation aspect of this new business model works well in the COVID-19 world, the personal peer-to-peer interaction element is clearly a problem. But even as the broader economy continues to struggle, there are signs the sharing economy may bounce back to previous growth trends in relatively short order. People are social animals, so we would expect social distancing habits to fade in the absence of widespread health fears. The leader in the sharing economy is arguably the ridesharing business model, which has largely supplanted conventional taxi services in metropolitan areas. But a combination of stay-at-home mandates and an aversion to sharing confined spaces served to crater demand since March 2020.

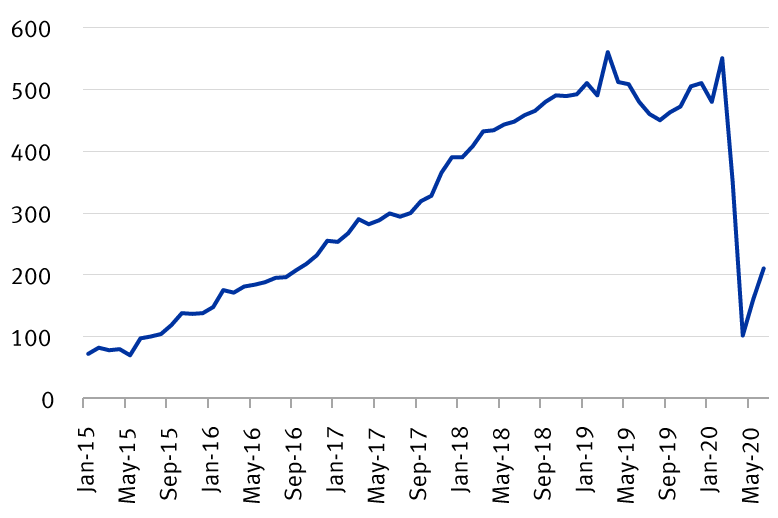

One of the rideshare pioneers, Uber Technologies Inc., reported an eye-watering decline in usage for the quarter ending June 2020, with ride bookings declining 75 percent compared to the year-ago period. This marked a much slower recovery relative to consensus estimates. In countries outside of North America, rides recovered as mobility restrictions were lifted, but not to the extent suggested by cellphone mobility data. People just didn’t want to jump into a shared vehicle.

COVID-19 set the rideshare industry back a few years

New York City Uber trips per day, ’000s

Source - New York City Taxi and Limousine Commission, RBC Capital Markets,

RBC Wealth Management; monthly through 6/30/20

This mirrors demand trends for public transportation, which in most instances showed even weaker demand trends. So who benefits from the aversion to shared transport? The automotive sector, at least in the short term. After the approximately 50 percent decline in light vehicle sales in the U.S. from March to April 2020, sales rebounded 40 percent month over month in May, and this trend

appeared to continue over the summer months, prompting manufacturers to step up production plans.

But we wouldn’t necessarily look to the major auto companies as a hedge against rideshare stagnation, as they face structural challenges of their own. Instead, we’d suggest the auto parts companies may be a better place to look.

RBC Capital Markets, LLC Hardlines Retail Analyst Scot Ciccarelli notes that the “greater usage of personal vehicles rather than public transportation, combined with people opting to fix/maintain existing vehicles vs. purchase new ones” helped drive revenue growth of 16 percent year over year in the June 2020 quarter for a major parts distributor.

We expect other sharing economy business models will eventually recover lost ground, but only when social-distancing habits recede. Online vacation rental marketplace companies, such as Airbnb and Vrbo, suffered an initial drop in demand, but recovered faster than hotels in many locations, as vacationers sought to drive to accommodations where social distancing would be easier to maintain.

However, we believe other businesses, such as those that offer shared business work spaces, may have a harder time of things as work-from-home practices become more ingrained.

Overall, we expect sharing economy companies to thrive again as we emerge from the pandemic. They play to the trend toward renting over owning, and consumers’ increasing preference to spend money on experiences rather than “stuff.” In most instances, we believe the COVID-19 recession will mark a speed bump in their secular growth trends and not a road block.

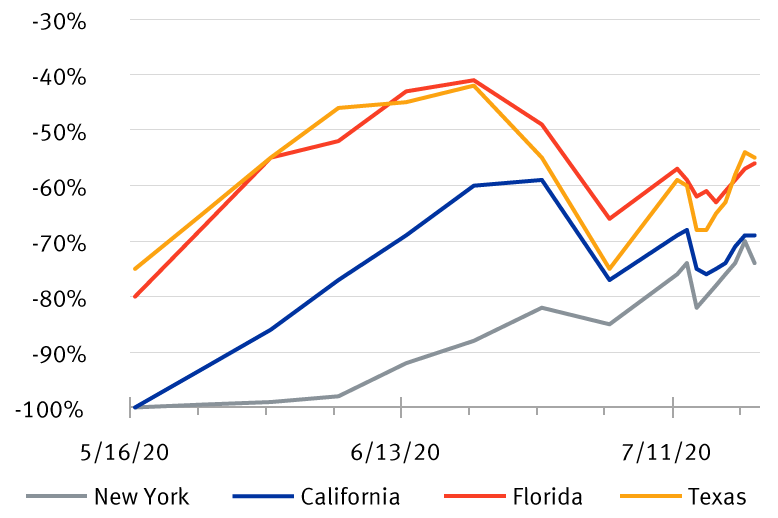

Consumers still wary of enclosed spaces and other people

Change in number of seated diners from the same date in 2019

Source - Open Table, RBC Capital Markets, RBC Wealth Management; data

includes reservations and walk-ins, from 5/16/20 through 7/19/20

Distribution of Ratings - RBC Capital Markets, LLC Equity Research

In the U.S., RBC Wealth Management operates as a division of RBC Capital Markets, LLC. In Canada, RBC Wealth Management includes, without limitation, RBC Dominion Securities Inc., which is a foreign affiliate of RBC Capital Markets, LLC. This report has been prepared by RBC Capital Markets, LLC which is an indirect wholly-owned subsidiary of the Royal Bank of Canada and, as such, is a related issuer of Royal Bank of Canada.

Non-U.S. Analyst Disclosure: Jim Allworth, Mark Bayko, Christopher Girdler, and Patrick McAllister, employees of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc.; Frédérique Carrier and Alastair Whitfield, employees of RBC Wealth Management USA’s foreign affiliate RBC Europe Limited; contributed to the preparation of this publication. These individuals are not registered with or qualified as research analysts with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since they are not associated persons of RBC Wealth Management, they may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

As of June 30, 2020

| Investment Banking Services Provided During Past 12 Months | ||||

|---|---|---|---|---|

| Rating | Count | Percent | Count | Percent |

| Buy [Outperform] | 776 | 51.63 | 238 | 30.67 |

| Hold [Sector Perform] | 635 | 42.25 | 130 | 20.47 |

| Sell [Underperform] | 92 | 6.12 | 12 | 13.04 |

This article was originally published on Aug. 24, 2020

Non-U.S. Analyst Disclosure: Jim Allworth, an employee of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc. contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since he is not an associated person of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.