Financial mistakes even the wealthy make

While a high income can certainly help in the battle to accumulate wealth, it does not guarantee it. In fact quite the opposite can often occur, with those with high incomes often out-spending themselves in order to keep up with the Jones’. This is probably best epitomized in the world of professional athletes, who often earn millions per year in their early 20’s, only to find themselves bankrupt in their 30’s or 40’s.

It is important to remember that that having a big paycheck and a great career doesn't automatically mean you're good with money or that you are automatically going to retire wealthy. You are still going to need professional guidance along the way, whether it be from investment managers, accountants, lawyers, financial planners or ideally, all of the above.

Of course there is a caveat to the above, and that can best be seen in those people who die in the pursuit of “riches”, without ever realizing that they have already achieved great wealth. They just never appreciate it.

So what are some of the mistakes the wealthy make that we can learn from?

Not tracking what you spend

Now this doesn’t mean you have to make up a strict budget and live or die by it, but it does mean that you should have a reasonable idea of what you do spend. Think of it in categories, housing costs, education costs, travel costs, entertainment costs, miscellaneous spending etc.

Not only will this give you an approximate idea of how much you pay for things, but it may also help you curtail unnecessary spending. Those with high incomes often think that they are never going to be able to outspend their income. Not so. Mike Tyson supposedly blew a $100 million fortune over a period of just a few years.

Trying to out earn excessive spending

This can be coupled with the above. Often those with careers that allow them to earn more money the harder they work, get sucked into working 6 or even 7 days a week just to keep up with their excessive spending. Is this really the way to live your life?

Coupled with this is the fact that this being on this hamster wheel of working more just to keep up with excessive spending can lead to saving and investing getting almost completely overlooked. This can then result in very savings being accumulated to show for all the hard work, and making retirement almost an impossibility.

Not having an automated savings plan

Ironically those with lower incomes tend to be much better at this because of the realization that if savings are not made regularly and automatically there will be no excess funds available for investment. High income earners assume that there will always be monies available for investment, which potentially there may be. However not automating saving means that this is often either overlooked, or lesser amounts actually end up getting saved than is necessary.

Not working with a financial professional

Less often in this very connected world, but still often seen in those who have accumulated their wealth quickly, or at a young age, many wealthy individuals overlook the fact that they need professional help in managing their finances. Being successful financially, (or intellectually) does not mean that you are an experienced investor, any more than reading about the NBA makes you a great basketball player. It takes years of experience to successfully navigate the investment waters and is very much a full time job. The two most common mistakes seen in this regard are over concentration in a single investment, or over confidence in a higher risk investment that is sure to be the next Apple or Microsoft.

Not to mention the mental strain of watching the stock markets and global economy fluctuate on a daily basis.

Not doing any tax or estate planning

Equally important as all of the above but probably the most overlooked until it is too late. Individuals that have a high income stream and a certain amount of wealth, are often either too busy, or completely overlook the need for longer term planning. This can often leave them in a hole when they finally do realize that they are mortal, and need to plan on passing their wealth to the next generation.

Not only can this planning help you save taxes but can also ensure that your heirs are well taken care of.

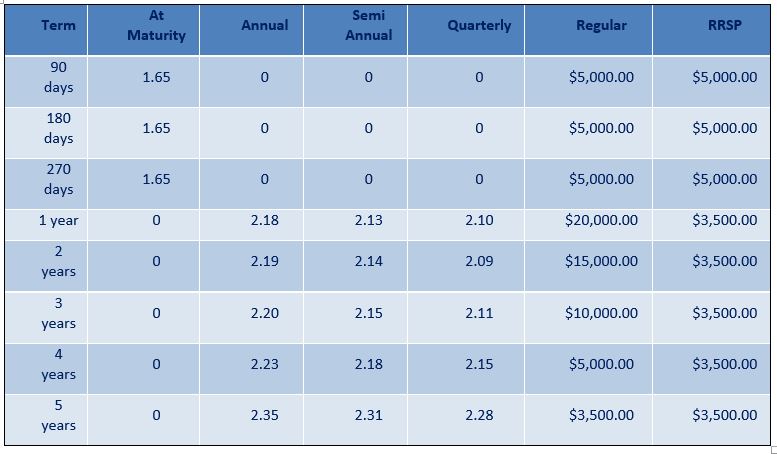

Current GIC rates*

Aug 30th 2019

Privacy & Security | Legal | Accessibility | Member-Canadian Investor Protection Fund

RBC Dominion Securities Inc. and Royal Bank of Canada are separate legal entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Dominion Securities Inc. 2018.

All rights reserved.