Asset Allocation – Contrarian Indicators

We all assume that institutional money managers know what they are doing, but is that really the case, or is it more a matter of just following the herd?

Let’s take a look at some of the consensus historical calls. In 2018 managers were significantly overweight equities, and underweight cash. The global equities market ended down 15%. Conversely, in October of 2016 manager’s cash reserves were at a 15 year high of 5.8%. Wrong again - global equities rose 30% over the next year. In November 2017 cash levels had fallen to 4.4%, the lowest in 4 years, the markets peaked in January of 2018 and then fell 20% over the remainder of the year.

At the market LOW in January of this year (as with other market lows, green arrows), managers were just 6% overweight equity, and the market has rallied significantly. Conversely in January of 2018, at the markets PEAK (see red arrows for other market peaks), equity weightings were 55% overweight.

Currently, money managers are overweight cash, at a 7 year high in their bond allocation, and underweight global equities. Emerging markets are the flavor of the month, with U.S. and European equity allocations relatively low.

Taking a contrarian view what does this tell us?

Buy U.S. and European equities

Sell Emerging markets

Overweight equities relative to cash and bonds

On the fixed income side of things, fund managers are currently 34% underweight (a 7 year high). Historically at this level, bonds have subsequently underperformed.

Finally to inflation. In November 70% expected higher year over year inflation – again a number at a 14 year high. Since then we know what has happened with expectations now for interest rate cuts in 2019 rather than hikes.

As lower inflation expectations usually correlate with lower commodity prices, allocations to this market sector should now be low / reduced.

As clients will know, a couple of months ago we reduced our equity weighting in anticipation of the market reaching a short term peak and entering a period of correction / consolidation – just as occurred. We are now looking at adding back some of this equity and reallocating our fixed income investments.

As always, what is good today may not be good tomorrow, so an active approach to portfolio management will continue to be at the fore of the equity investment process. Please contact us of you would like to know more.

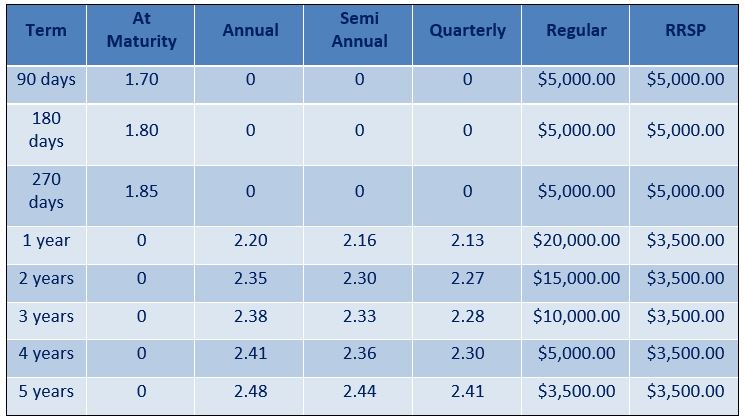

Current GIC rates*

May 31st 2019

Privacy & Security | Legal | Accessibility | Member-Canadian Investor Protection Fund

RBC Dominion Securities Inc. and Royal Bank of Canada are separate legal entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Dominion Securities Inc. 2018.

All rights reserved.