To my clients:

It was an up week for North American stock markets with the Canadian TSX finishing up 2.7%; the U.S. Dow Jones Index finishing up 3.2%; and the U.S. S&P 500 finishing up 4.0%.

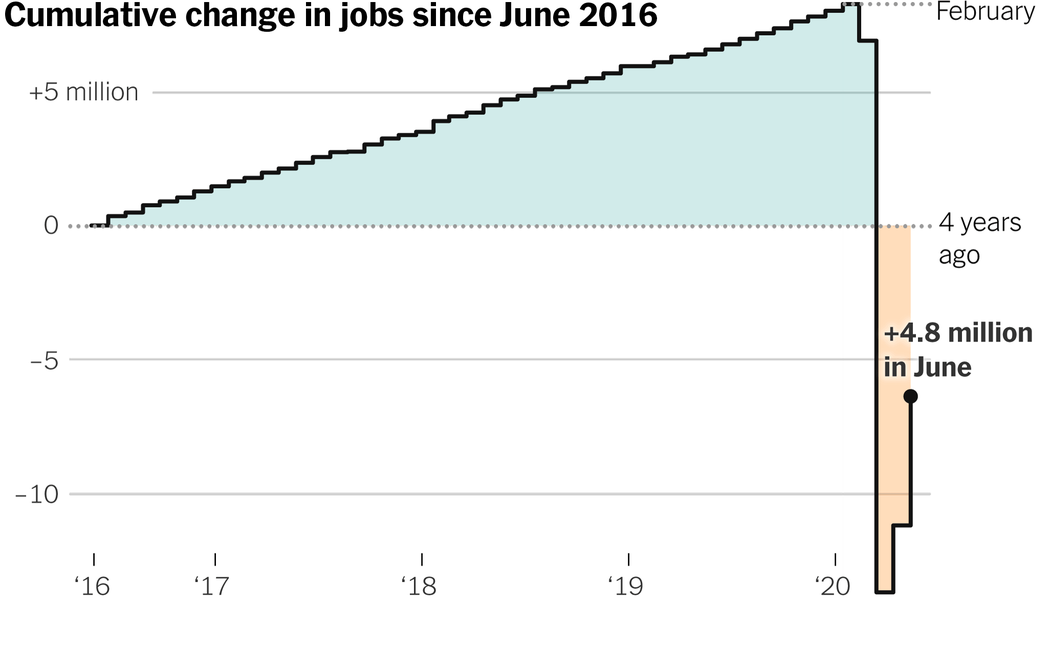

In truth, economic data this week was solid in comparison to the lows set in March and April. The U.S. Employment report released yesterday showed a staggering 4.8 million jobs were added back in June (I won’t say “created”, because these are not organically created new jobs, but rather a rehiring of workers artificially displaced). Likewise, the ISM Manufacturing Index returned to an expansionary reading at 52.6. Ordinarily, this tandem of readings would be viewed as exceptional.

But I will emphasize the first sentence of the last paragraph – in comparison to the lows. The plunge in economic output was historically sharp and deep, and was an artificial construct of an enforced shuttering of the economy. A reflexive and sharp bounce from such lows is not altogether unwarranted or unexpected. Further, given the scale and magnitude of the economic stoppage – the reflexive bounce is also proving to be historically large. But in my opinion, the bounce to date represents a recapturing of the low hanging economic fruit. Gains from here will almost assuredly begin slowing. For example, restaurants which may have reopened back to 50% capacity and rehired employees accordingly will not be returning to 100% capacity any time soon and are unlikely to rehire remaining staff. Also, consider that other slowed industries which were incentivized to keep staff on payroll via various government programs may soon see the end to this governmental largesse.

The preceding doesn’t even take into account the possibility of a broader reversal of U.S. reopening. Covid19 cases in the U.S. continue to surge, with the U.S. now regularly setting new highs in daily case counts as each day passes. Of equal concern is that this surge in case counts is broadly distributed throughout the U.S. In fact, the 7-day moving average of cases reveals that the vast majority of U.S. states are now clearly in well-defined up trends. And many of these trends are, in fact, exponential. Arguments that increased testing alone is accounting for this surge are not accurate. In fact, the percentage of tests returning positive has also been increasing in recent weeks. In other words, not only are more tests being conducted, but a higher percentage of this greater number of tests are returning positive. If infection rates were remaining constant, or even declining (as a certain world leader would like everyone to believe), then one would statistically expect to see a decline in positive test results. That is just not happening. To state the obvious, this weekend’s July 4th festivities are not likely to help the accelerating trend. So, in my opinion, further scaling back of the U.S. opening is highly likely in the weeks and months ahead.

A good way to envision the recovery to date is to consider that the economy is, for all intents and purposes, recovering into recessionary conditions. While this isn’t technically a true statement (because the economy IS expanding from its recent lows and, by definition, any expansion cannot be simultaneously viewed as recessionary), what is true is that the economic neighborhood to which it is recovering is substantially weaker than that which it left in December of 2019. The following chart from the New York Times illustrating the sharp recovery in U.S. employment further illustrates the point. The recovery is clearly evident. Likewise, the distance yet to go is equally evident. And per my arguments above, I would suggest that the slope of the rehiring trend will significantly flatten (and perhaps partially reverse) in the months ahead. As an aside, one other point the chart illustrates is how consistently strong the U.S. labour market had been the last 5-years and, to the extent employment reflects broader conditions, the U.S. economy. This may bode well for the day when the Covid19 pandemic threat is finally put in the rearview mirror.

Given the acceleration in new Covid19 cases in the U.S. to ever higher new levels, I continue to anticipate a better re-entry point to bring clients back to a full neutral position in equities (stocks). As it stands, client equity positioning remains slightly below neutral.

That’s it for this week. All the best and stay safe,

Nick

Nick Scholte, CIM, FCSI

Vice-President & Portfolio Manager

Scholte Wealth Management

RBC Dominion Securities Inc. │ Tel: 604.257.7569 │ Fax: 604.235.9950

3200-1055 West Georgia │ Vancouver, BC │ V6E 3P3

Toll Free: 1.844.665.9900 │Email: nick.scholte@rbc.com

Visit Our Website: www.nickscholte.ca

We accept new clients primarily by referral from our existing clients. If you have family or friends who would be a good fit for our specialized wealth management services, please let us know.

Any recommendations herein are for the exclusive use of clients of RBC Dominion Securities and Investment Advisor Nick Scholte. Any other direct or indirect recipient of this email should consult with his/her own licensed investment advisor prior to implementing any investment action he/she may be contemplating.