To my clients:

It was an up week for North American stock markets with the Canadian TSX finishing up 1.0%; the U.S. Dow Jones Index up 0.7%; and the U.S. S&P 500 up 0.9%.

Let’s start this week’s update with a quick look at the final key economic data points of the 2010’s…

Beginning with the ISM Non-Manufacturing Index (aka “Services”), at a reading of 55.0 it improved from the prior month’s 53.9 reading, and beat the average expectation of economists of 54.5. Regarding employment, today it was announced that the U.S. created 145,000 new jobs in the month of December – significantly under the prior month’s downwardly revised, but still unsustainably strong reading of 256,000 new jobs, as well as missing the expectation of economists for 164,000 new jobs. Generally speaking, the jobs report was “ok” (not great, but not bad either), while the services sector has probably re-entered “good” territory. Combined, from a strategic perspective with regards to portfolio positioning, these two releases are not strong enough to overcome the continued material weakness in the manufacturing sector, and I think I must continue to defer adding back equity exposure for the time being. While I lean heavily toward the view that manufacturing will recover in the months ahead, for now it is likely best to remain prudent. That said, I reiterate that portfolio positioning of clients is essentially at the long-term equity target (as individually set in the Investment Policy Statement of each client), and by no means are portfolios skewed heavily toward defense at the present time either. Hopefully coming data releases will support a decision to add back equity in the not too distant future.

Regarding the weakness in manufacturing, few would argue that the U.S./China trade war has not had an impact. Quite the opposite – of course it has. It is therefore worth noting that Chinese Vice Premier Liu He will be in Washington next Monday to Wednesday (January 13th to 15th) to officially sign the Phase 1 agreement recently reached. President Trump has already said that negotiations on Phase 2 will begin immediately thereafter. I have always said that I suspected a “deal” would get done because it is in both countries’ interest to do so, although the Phase 1 agreement isn’t as all-encompassing as I envisioned when making those assertions. If and when a Phase 2 agreement is finalized is somewhat murky, not least because of the November Presidential election. Trump has already said he might wait to sign a Phase 2 deal until after the election because he thinks he might be able to get a “better deal” if he waits until then. That’s possible. But I’d also suggest that he’s likely to argue he is the only one “tough enough” to take on China (which, frankly, probably has some truth to it) and that if the U.S. electorate wants to see the Phase 2 deal completed, they’d best re-elect him. As such, while I was previously disposed to believing that more material agreements might be reached before the election, I am far less certain now. That said, the general tenor of trade relations has improved, and I’d hope/expect this to be reflected in the ISM manufacturing surveys in the months ahead.

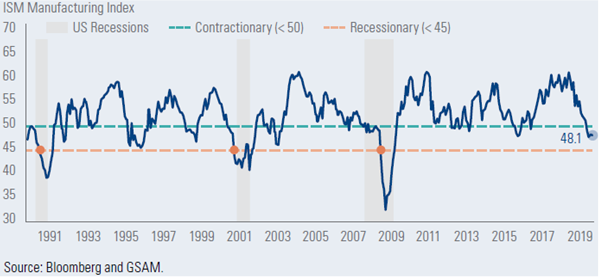

One last thought on the ISM Manufacturing Index. While it is certainly true that the 50.0 line separates expansion from contraction in the manufacturing sector, it is no longer the case that a break below 50.0 is a dire harbinger of economy wide contraction (i.e. recession). As I wrote last week, manufacturing is a much smaller component of U.S. economic activity now than in the two decades following World War II. Through the 1960’s manufacturing represented nearly 30% of U.S. economic activity, while now it represents just over 10%. I further wrote:

“absent sympathetic deterioration in the much larger “services” sector, it is felt that manufacturing must now suffer a sustained drop below an ISM reading of 45.0 to be a harbinger of imminent recession”

Coincidentally, I came across a chart just this week that hammers home the point. The chart comes courtesy of Goldman Sachs and Bloomberg. The solid dark blue line shows the reported monthly readings for the ISM Manufacturing Index going back to 1990. The dotted light blue line shows the 50.0 demarcation line separating manufacturing expansion (above the line) from manufacturing contraction below the line. The orange dotted line represents the 45.0 reading I wrote about last week. There are three areas shaded grey in the chart – these represent U.S. recessions. If one looks at the chart, it will be immediately apparent that manufacturing readings below 50.0 occur periodically and reasonably regularly, and yet recession need not result. It is when the ISM manufacturing reading dips below 45.0 (as represented by the three orange circles) that one would be well served to pay heed. We are not there yet, and I am optimistic that owing to strength elsewhere in the economy as well as an initial improvement in trade relations that we will not get there at all, and the index will spring back above 50.0 in the months ahead.

And now a few comments on the U.S./Iranian affair. Setting aside the apparent downing of the commercial airliner for a moment (see the last paragraph for more), it is apparent to me that neither side wants to engage in a full scale war with each other. I had seen reports early in the week that the Swiss Ambassador to Iran met with the Iranians and delivered a message on behalf of the U.S. indicating that the U.S. knew that Iran must respond to the killing of General Soleimani. That was the extent of the report I saw. However, if true (and I emphasize the word “if” here), it certainly fits with how events played out insofar as Iran apparently delivered a warning to Iraq three hours before the missile attack took place thereby giving inhabitants of the bases attacked time to seek shelter. The attack therefore seemed designed for Iranian domestic consumption (i.e. we stood up to the aggressor United States), yet at the same time avoided crossing one of Trump’s “red lines” with respect to the killing of U.S. citizens. In other words, I speculate that the more complete message delivered by the Swiss Ambassador may have been along the lines of “respond as we know you must, but be sure not to inflict casualties or there will be a significant response”. That such back channel discussions may well have taken place is further evidenced by Trump’s declaration barely 12 hours later when he observed that it appears Iran is “standing down” and indicated that the U.S. was inclined to do the same (I’ve heavily paraphrased here of course). As I watched him saying those words that morning, I was struck immediately by the implausibility of such a statement unless there were some pre-standing agreement in place.

Nonetheless, our commodity (and de facto “regional”) analyst, Helima Croft, writes that tensions are sure to continue. The other “red line” set by Trump is the one of nuclear weapon advancement by Iran. In the wake of recent events, Iran has said they would now accelerate such developments. Much like China has dominated the news cycle for the past two years, I suspect Iran and its nuclear ambitions will press ever more to the fore.

Lastly, on the airliner shot down… many relevant parties (Canada, the U.S., the U.K.) seem to be pushing the narrative that the aircraft was shot down accidentally. I suspect this to be true. It doesn’t take much to imagine the stress of on-edge personnel manning missile defenses in the immediate hours after the Iranian attack on the Iraqi airbases. The airliner was apparently “shot down” (and video evidence looks to support the claim) about 2 to 3 hours after the attack. It is very sad, and especially so for Canadians (a large number of whom were on the ill-fated flight). For my family and I, it has hit even closer to home. My 7-year old son plays for the Coquitlam Metro Ford Soccer Club. An older boy and his father were members of the club (player and coach respectively). Both were on the flight in question, as was the boy’s mother. While we didn’t know the family personally, the soccer club will be holding a moment of silence before all games this weekend as a small measure of respect. Last night I had to explain to my son the circumstances leading to this decision, and what might be expected before his game on Saturday. It was a sad conversation to be having with a 7 year-old.

That’s it for this week. All the best,

Nick

Nick Scholte, CIM, FCSI

Vice-President & Portfolio Manager

Scholte Wealth Management

RBC Dominion Securities Inc. │ Tel: 604.257.7569 │ Fax: 604.235.9950

3200-1055 West Georgia │ Vancouver, BC │ V6E 3P3

Toll Free: 1.844.665.9900 │Email: nick.scholte@rbc.com

Visit Our Website: www.nickscholte.ca

We accept new clients primarily by referral from our existing clients. If you have family or friends who would be a good fit for our specialized wealth management services, please let us know.

Any recommendations herein are for the exclusive use of clients of RBC Dominion Securities and Investment Advisor Nick Scholte. Any other direct or indirect recipient of this email should consult with his/her own licensed investment advisor prior to implementing any investment action he/she may be contemplating.