(August 2022)

Building on our past updates from as recent as May/June of this year I wanted to articulate the main stress points and items that are holding markets down and what the way forward might look like.

First and foremost, I will always say that the main input for any investor is Time in the market- which is to say, so long as you stay invested and committed to your strategy, you will be fine. However, markets have a history of challenging us in this regard, so it’s important to have a game plan. For the most part, short term risks are really just distractions. They dislocate markets and discount investments according to an assessment of change and fear. I don’t know of any investor who has created wealth by being focused on short term events.

The best way to acknowledge and deal with short term risks is to discuss what they mean and review some relevant context. So, while markets have been quite grumpy to start 2022- Let’s review what’s going on and what things we will need to see for market performance to improve.

The current market has layers of disruptive factors relating to COVID-19/ China/ Supply chain, The Russia Ukraine Conflict and then lastly Inflation and rising interest rates.

The COVID-19 pandemic is now firmly in its 3rd year and there continue to be many lingering effects. Indeed, while we did see the market rebound sizably in 2020 from a sizable market decline, economic giants like China are still struggling to combat the virus and continue to take strict measures to manage any outbreak. As such, their economy has not been able to re-open and re-accelerate alongside markets like the US and Europe. Understanding China also helps to understand the ongoing issues with various supply chains for end consumer goods. While it seems the consumer worldwide has had a good appetite to spend, there has been severe disruption and limited supply of finished goods available for the global consumer to access. This has understated global commerce considerably and driven costs higher as more dollars chase fewer goods.

In more recent events, in yet another Olympic year, Russia participates in the winter games in 2022 and then invades a neighbour nation as they did in 2014 into Crimea. This invasion and conflict has had far reaching issues and has created a scarcity of oil and gas and grain in various parts of the world. Thankfully, we have seen some progress in the shipping of grain from Ukraine more recently.

Tangled within all this is the output known as inflation. Higher inflation is definitely a reasonable outcome when you have such a strong employment picture as well as interest rates at emergency levels to combat the pandemic (not to mention additional direct stimulus which was also provided). We have had a lot of liquidity in the system since 2020. Interest rates needed to move higher and central bankers are doing the right thing by saying they will raise rates until inflation comes down. The few caveats would be to what end inflation can be otherwise tempered by solving supply chain challenges directly (China re-opens) and also what peace in Eastern Europe would provide to the price dynamics of oil and gas (and other). In August we saw a recent stabilization of inflation in the U.S. and slight decline in Canada’s rate of inflation. This was viewed as good news. Moving forward, it’s quite clear that any improvement to inflation will see markets advance sizably on the basis that inflation is now under control (and the underlying factors).

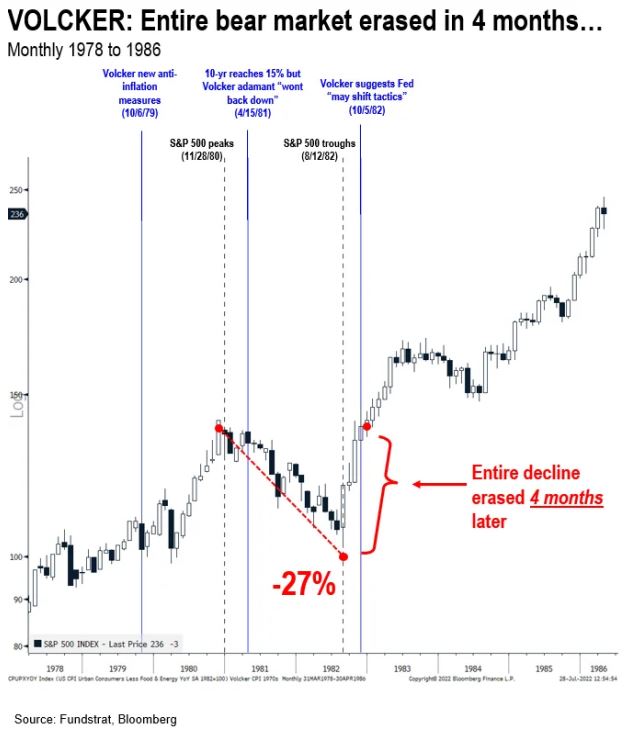

While it is true that it will take time for these issues to be ‘solved’, it’s important to remember that the market is a forward looking vehicle and it will quickly shift to value businesses based on a better future, with better visibility. For historical context, in 1982 when the US was fighting its last war on inflation, once inflation responded to the rate hikes introduced by Paul Volcker it took only 4 months for the U.S market to retrace and build on the preceding market decline of 27% in 1981. Only 4 months.

The bottom line- We won’t know how the ship will turn but any improvement of the stress factors mentioned here will see markets respond very favourably- especially improving Inflation metrics.

Keep Calm and Carry On.

Wishing you a great end to your summer.