The Exponential Age

The term “Exponential Age” is thrown around on social media to justify high valuations in exponentially growing technology companies.

Raoul Pal of Realvision has been one of the proponents of investing in exponential age related companies.

His definition goes something like this:

When interest rates approach the zero bound the valuation of companies is less based on cash flow and more based upon the prospects of exponential growth.

He actually uses an analogy of super-long term bonds when describing the price effect of low interest rates on exponential age companies. If interest rates drop, super long term bonds go up enormously.

It is quite an interesting filter to view investments through.

There have been many derivatives of exponential age narratives throughout history, and each has ended showing there was no exponential age, and cash flows to price ultimately did matter. Who knows? Maybe this one is different?

The reason I bring up the exponential age idea is because I have found myself applying the same logic to real estate prices.

A time not long ago, I used to be able to guess an approximate list price on real estate for sale in my community, before looking at the actual list price. Today, when I look at places listed for sale, I don’t have a clue how high the list price might be.

This is the exponential age for real estate too.

Price has little to do with the cash flow the real estate asset produces any longer.

So what happens if interest rates slowly go back up?

Here we are just a week after the writing of my Triannual Review with the European Central Bank starting to “recalibrate” (taper) asset purchases as well as more signals from the US Fed about tapering.

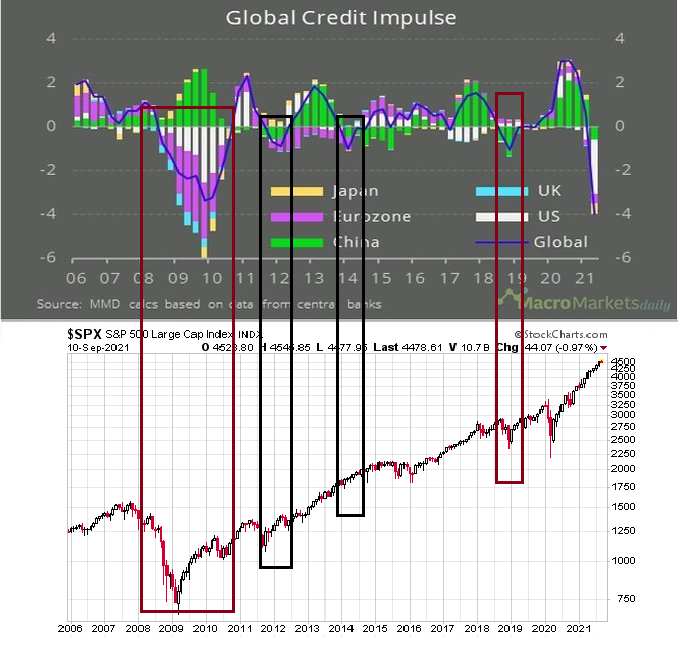

The chart below does an excellent job of breaking down the monetary actions of the global central banks both individually and then in concert. Note the solid blue line in the top window and how it moves in relation to the S&P500 index in the bottom window. (Cam Hui, CFA).

The message of this chart is that credit pulses and stock markets are not a clear correlation, but should not be ignored either.

The Bank of Canada came out of left field last week and stated they might start to raise interest rates BEFORE the start to taper. Had a little smile on my lips when I heard that.

Imagine you are driving your car up to a stop light.

The amber warning lights are flashing that the green is going to turn red. What do you do? You take your foot off the accelerator and begin to depress the brake pedal.

If the Bank of Canada decides to raise interest rates before tapering support, it would be like leaving your right foot on the gas and using your left foot to push the brakes at the same time.

Hmmm?

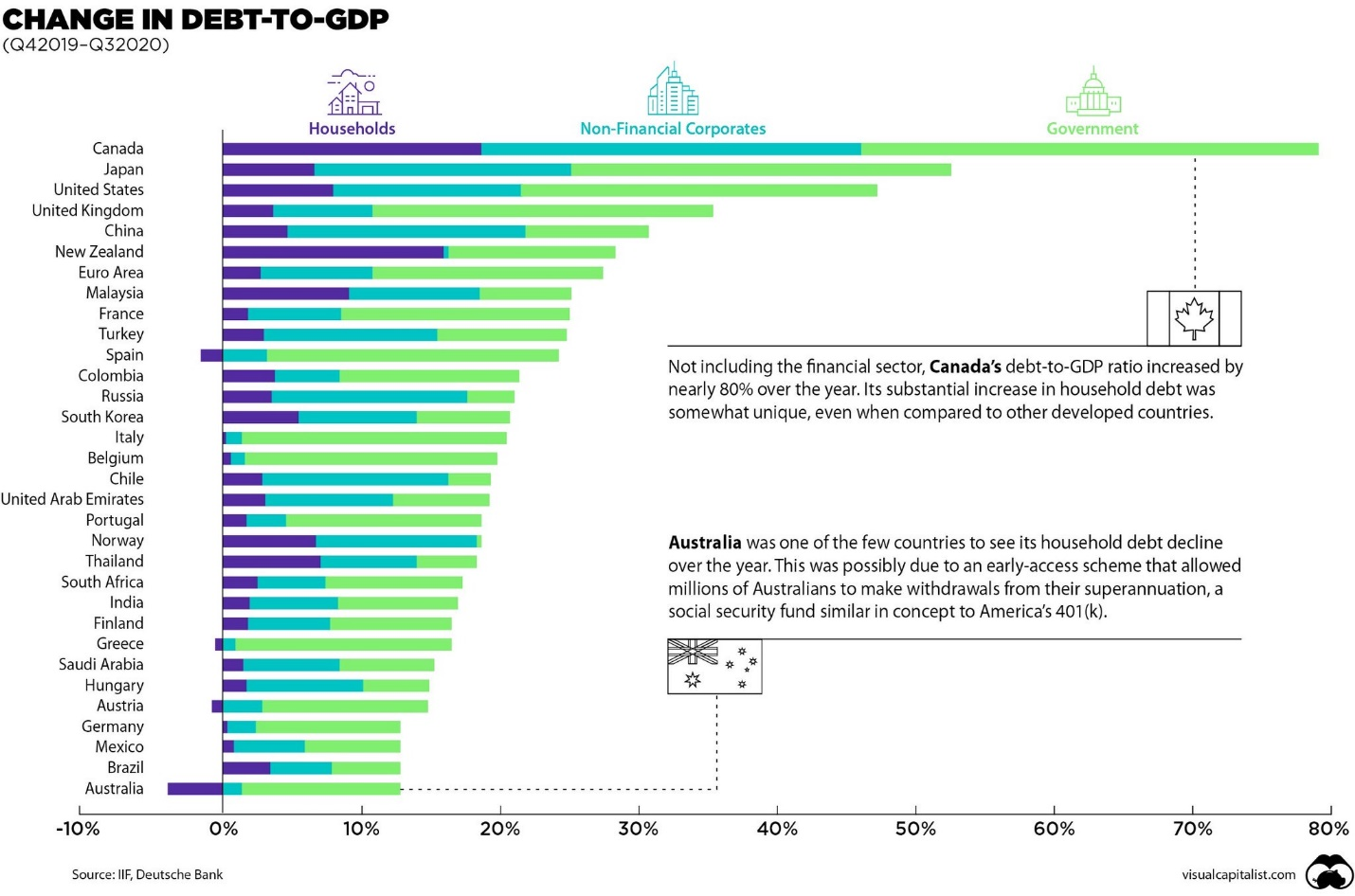

Canada has been the world leader in growing debt relative to GDP the past few years.

Wish our leaders well in whatever choices they make in coming months.

To wind up this short note, let’s look at how extreme the present backdrops to the economic and monetary systems are.

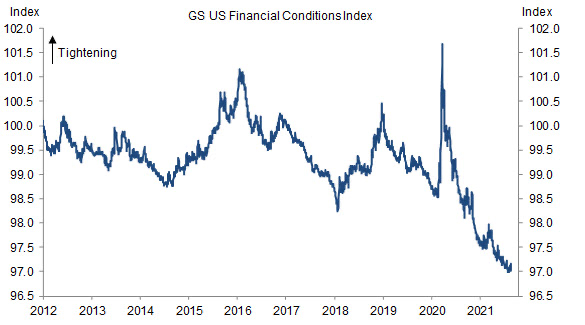

The Goldman Sachs chart below shows US financial conditions the most lax on record. No wonder people are flocking to stock and real estate markets when monetary conditions are this loose.

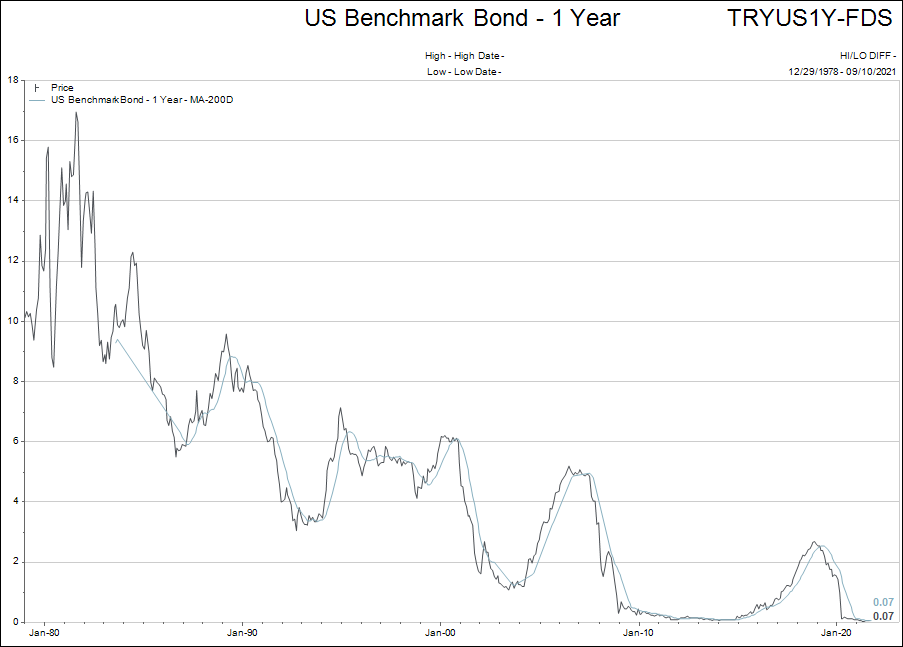

The winds of change will begin when bond yields start to rise. Below is a chart with the yield on the benchmark 1-year US Treasury bond since 1980.

I’d say interest rates are pretty low relative to the past 40 years and there is no change showing up on this chart…yet.

With asset prices as elevated as they are at present and monetary policy still this lax, it makes sense that a reversal of accommodative policy is imminent.

The lead chart shows the global credit impulse wave has already crested. I strongly believe this will take the rest of this decade to unwind to a more moderate level.

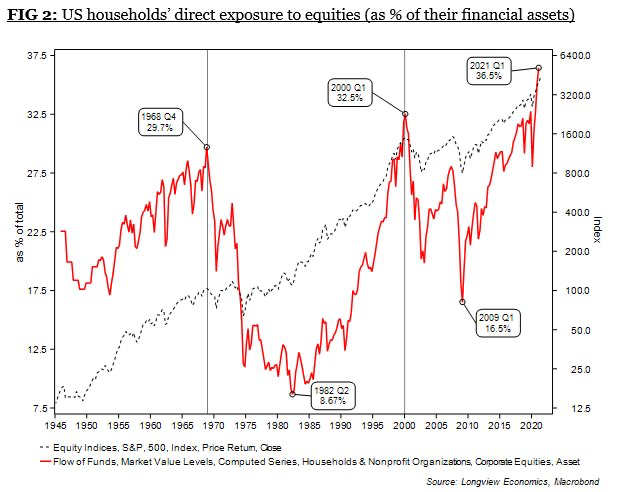

The next chart shows the correlation between the stock markets index level and the amount of money US households have exposed to stocks, and it looks like everyone is in the pool again at present time.

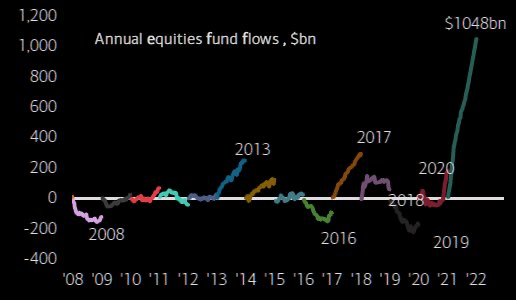

Seen another way, here are the net flows of funds into the US stocks:

The summary point of this note is financial conditions must begin to tighten soon. The difference today from the other attempts to cut back on financial support and then begin to lift interest rates is the economy peaked for the cycle back in May 2021.

This attempt will be done under the following conditions:

- Record high asset valuations

- Record high stock and real estate exposure by retail investors

- Spiking inflation

- Chip shortages and supply chain disruptions

- COVID spikes

Financial markets are entering a time of increased volatility. Don’t be afraid to rebalance your portfolio if you feel the need.

Send me an email to arrange a good time to chat.

Enjoy the week!