The Future

As Yogi Barra famously, said: “It’s tough to make predictions, especially about the future.”

So rather than try and predict the future, why not have a number of possible outcomes mapped out and decide how you would react as the future takes shape?

There has been some excellent analysis, from the every corner of our financial world, about what unprecedented monetary policy applied for too long past the “emergency situation,” might mean for the real world economy in the future.

The best way to summarize the opinions is to drop them into one of two themes:

- That the present financial conditions are sustainable for multiple decades longer with short duration financial emergencies dotting the landscape. The central banks are capable of extinguishing all emergencies with monetary policy and, therefore, perpetuate high asset prices.

- Or, there is an approaching inflection point in monetary policy where interest rates will rise and liquidity will fall reversing asset price appreciation.

The past couple comments looked at theme number two, while the July 8th comment, and the balance of this comment outline theme one.

To keep the asset price appreciation train rolling forward financial repression must continue to be employed.

There are a number of examples in recent history (and right now), of where monetary policy has devolved into financial repression, and monetary over-reach.

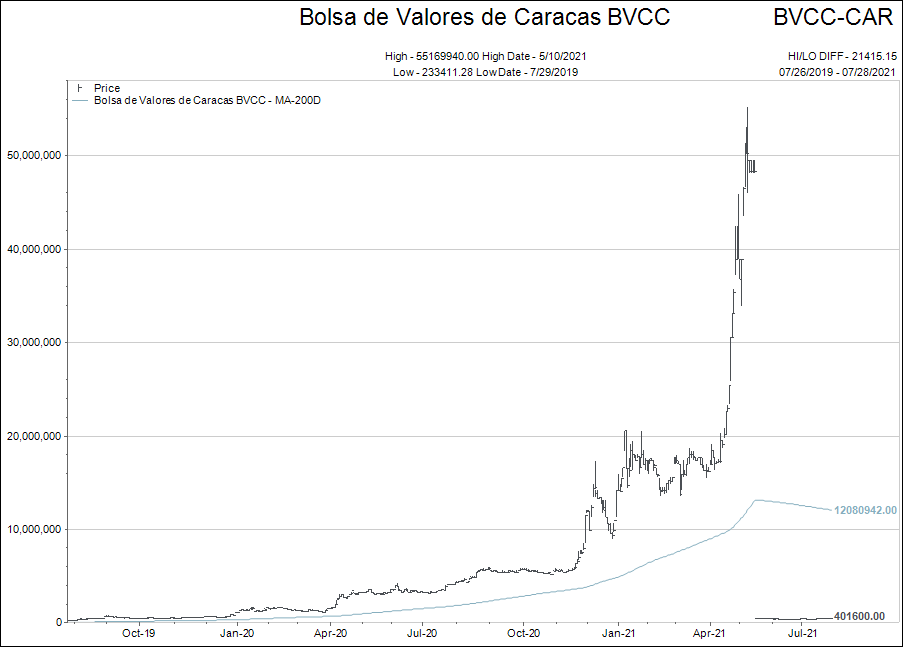

Once these historical examples started to exponentially unwind—Weimar Germany, Zimbabwe, Ukraine and present day Venezuela[i]—they never left the pathway of monetary overreach, and printed their ways to their currencies being valueless.

On the other side of the coin, there is the example of the United States righting the ship and stifling inflation using draconian level interest rate increases in the 1970s.

There was a lot of pain for a period of time, but the currency was saved from the wave of potential hyperinflation. Low interest rates of our present era, mask the level of global overreach in monetary policy.

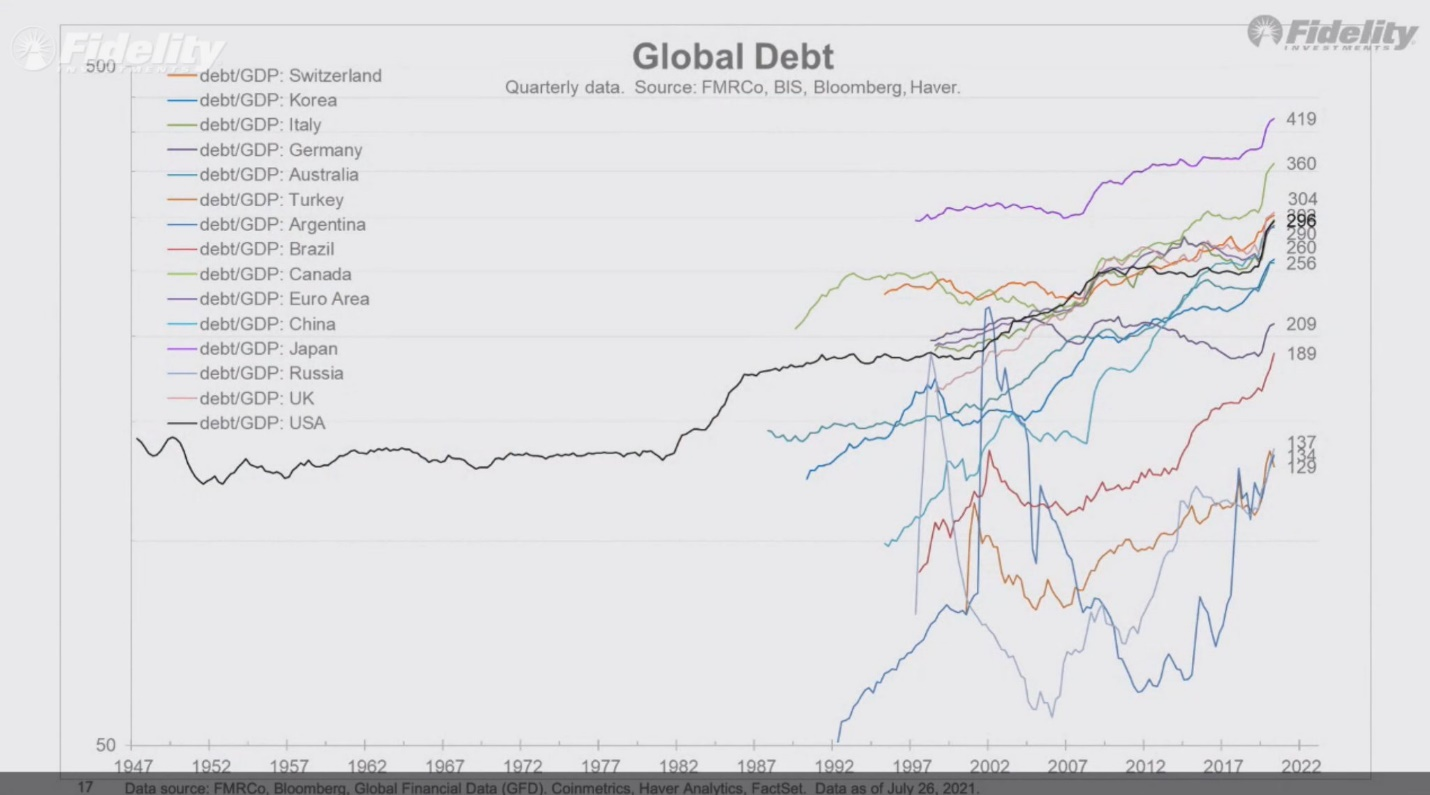

The chart below is interesting to me on two levels:

- It shows the global nature of the ramp up in debt, and

- It clearly shows the overreach of Canada, relative to the rest of the world.

For those arguing the sustainability of the limitless debt model of finance, the narrative runs something like this: The debt bubble is so big now that the central banks have no choice but to support it and never let interest rates rise again.

Or simply, interest rates can’t ever go up!

No matter what our opinions are about the future, we need to have a strategy that is accommodative to possibility of either outcome.

One strategic example I will share with you below, could be employed by an investor to hedge this risk. This is not a recommendation, please contact me if you wish to discuss in relationship to your portfolio.

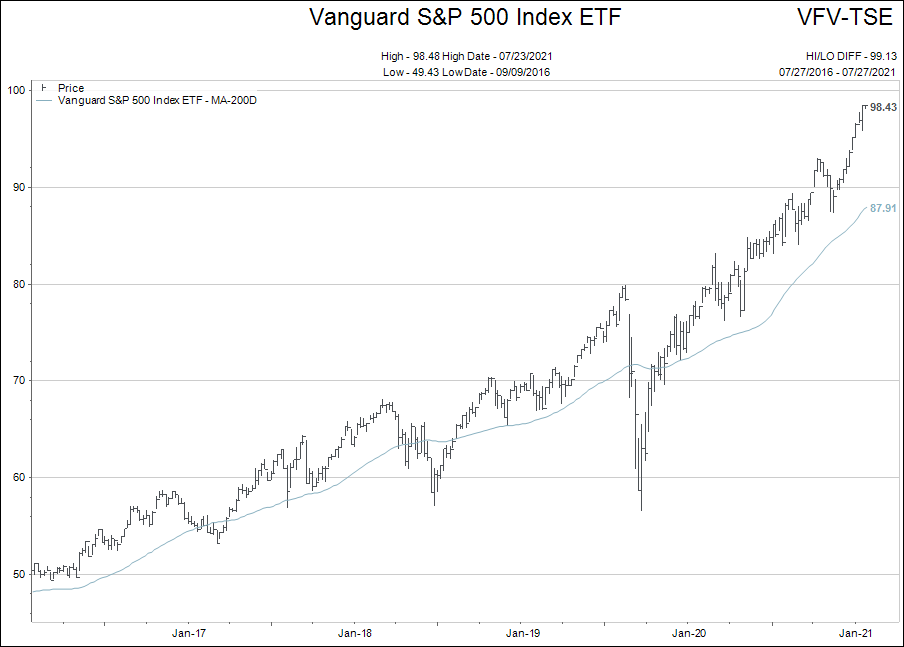

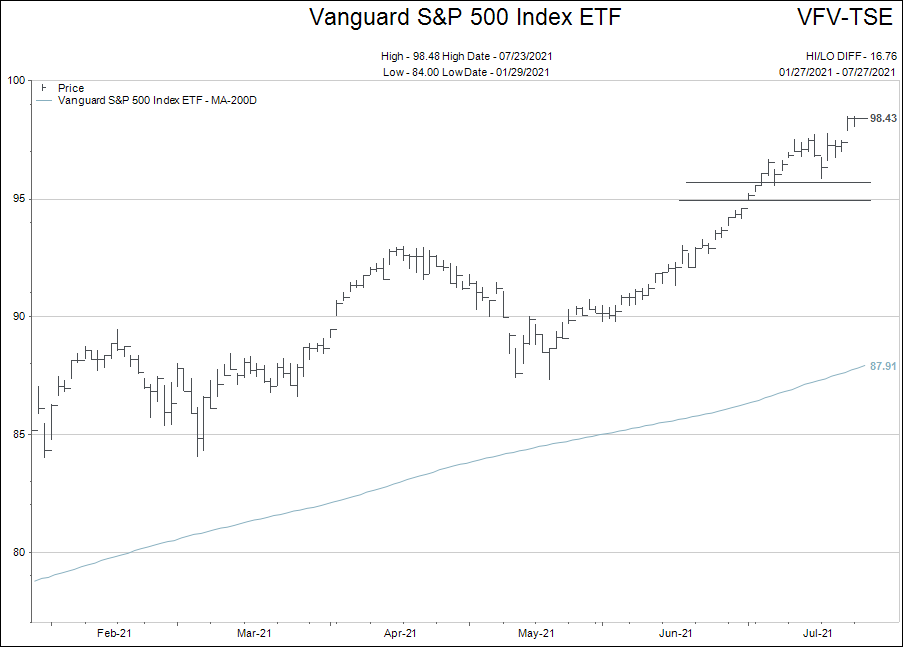

The following chart is of the S&P 500, traded in Canadian currency and is being used for illustrative purposes. Visually, it appears overextended to the upside and in need of a correction.

The challenge is, that this has been true for quite some time and selling early is always dangerous in a BULL market.

So, what can one do?

The chart above shows the Vanguard S&P 500 index, has not traded below the $95.00 level in two months. One can use this level as a trigger point to reduce their general holdings in the stock market IF the above ETF trades below that level.

It is not a fancy or complicated strategy. If you like the idea of building more defense into your portfolio, please let me know and we can decided what works for you.

[i] The following is a chart of the Venezuelan stock market. If you think that stock markets going up quickly against the backdrop of stagnating economic conditions due to money creation, this chart will give you pause to reconsider that position. We all know how life has been in Venezuela the past few years.