VISA and Stock Market Valuations

A client forwarded a research piece labeling VISA an untouchable disruptor company. Disruptor refers to the way a company changes an industry and monopolizes the business model by new or superior technology.

Let me add a couple of the bullets as to why VISA is presented in this way:

- Electronic transactions are a growing segment of commerce.

- Companies like PayPal and Square are taking business from traditional banks and they run on the backs of VISA (and MasterCard).

- New apps like Revolut and N26 use VISA (MasterCard) as their clearing platforms too.

- Smart phone pay apps do the same thing.

- Processing speeds are superior to crypto, especially Bitcoin.

This is not an advertisement or recommendation for VISA, but makes the point that this well-established company, which dominates market share in its sector, is still flourishing in the new digital age.

But what does someone pay for a great company? What price is good value?

The chart below shows the quarterly Price to Earnings ratio (P/E) for VISA. (P/E simply takes the stock price and divides it by the earnings to create a relative valuation of the price in terms of the company’s own history).

As you can see, the P/E ratio pre 2016 ranged between 20 and 36 times. Earnings growth was solid in this period and the stock price has gone up 10 fold since 2012.

At present, the P/E ratio using trailing earnings is 51x ($4.69 earnings divided by $240); that is a big number!

The price would have to fall back to $140 just to get back to a 30x multiple assuming earnings did not change.

Could that happen? Absolutely!

In 2008, the P/E multiple for VISA was 36x earnings. The stock price was $21.00 and earnings were $.56.

In 2009, after the Great Recession decline, the P/E multiple for VISA was 20x, the stock price was $12.20 and earnings were $.61.

Wait, what?

Yes, earnings went up from $.56 to $.61, yet the stock fell from $21 to $12.20.

All that happened was the market sentiment shifted from BULLISH to BEARISH or, greed to fear, and the P/E multiple contracted, so where does market sentiment resides as of mid-July 2021?

This analysis of P/E ratio can be applied to stocks, real estate and bonds. By applying the process above, all of those asset classes are expensive at present time.

So here is the question: What might cause market sentiment to shift?

When P/E ratios are high, there are lots of factors that might cause a shift in sentiment. The most important being a drop in central bank liquidity support.

But there is one huge reason nothing will change either.

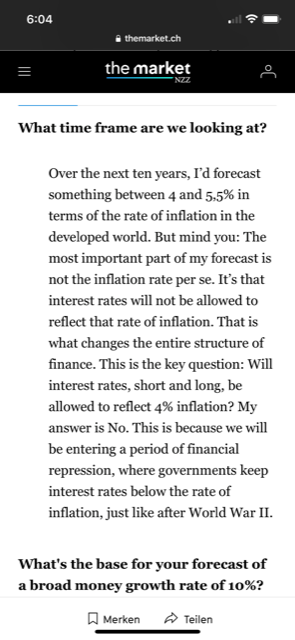

The short excerpt from a Russell Napier interview below summarizes a good case as to why P/E ratios may not fall much in the future.

The statement that interest rates will not be allowed to rise to create a positive interest rate must be considered by investors.

The above is Russell Napier’s opinion, but it is worth considering as a real possibility. It creates a difficult decision for investors trying to evaluate the risk of holding overvalued stocks in light of the financial repression of cash.

My summary statement, as alluded to last week, is that market corrections are likely to be sudden, sharp and relatively short lived.

The injections of new money into the system are expected to bring these corrections to an end and asset prices are expected to rise again, much like what we experienced in March 2020.

Nobody said it was going to be easy.

Please make sure you hold an asset mix of investments that can withstand a 30% correction, without you getting too nervous about your finances. Given the conditions shown below, we should not be surprised if that were to happen.

Where We Stand

The following charts are presented to see how far away from “normal” financial markets have moved.

The above chart plots “price to sales” data. Much like price to earnings, it shows the extreme historical cost of a share of a given company relative to company sales.

The next chart breaks the top five tech companies out of the S&P 500. The gap between the two lines is the net difference of performance of the index with and without owning the top five companies (Microsoft, Apple, Google, Amazon, FaceBook).

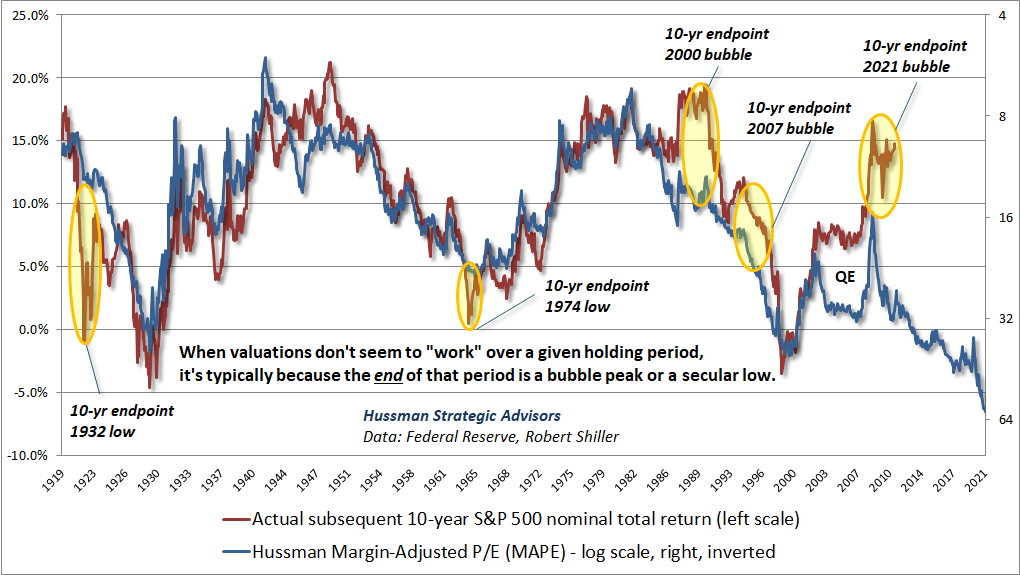

The following chart plots a complicated set of data, so let’s use it for visual purposes only. The key point is that the red line is trailing the blue line plot by 10 years.

Since 1919, the red and blue lines tend to move in sync directionally.

At certain times you can see the red line far above or below the blue line. If the red line is below the blue line, the S&P 500 is considered “cheap.” If the red line is above the blue line, the opposite is true.

The yellow circles on the chart highlight moments of extreme valuation.

It is worth noting how the red line depicting the high rates of return are ultimately reined in by valuation constraints and the two line converge again.

The market is clearly at a “proceed with caution” moment.

To finish the weekly comment, let’s look at interest rates. These charts do not look like a world worried about inflation coming back to haunt again.

I can also show you in one chart why this can happen even in a world frothing with a higher rate of inflation.

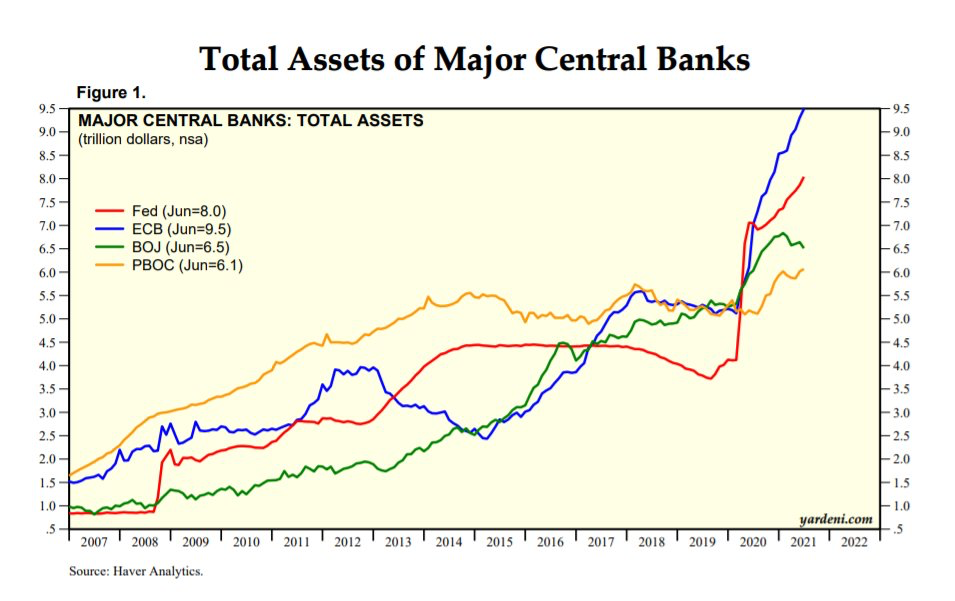

What amazes me, is the comparison of the central bank response to the crisis in 2008, and the COVID liquidity puke in 2020.

For those entertaining the words of global central bankers speaking of a “tapering of liquidity” in our future: Maybe the central banks could just try and stop printing first.

As always, please don’t hesitate to send me your feedback and thoughts! If you have questions or concerns, email me to set up a time to chat and review your portfolio.