Living with Inflation in 2021

Last week, in the Tri-annual Report, the goal was to summarize the financial markets of 2021 as:

- Very expensive on a historical value spectrum.

- But very expensive because the “structure” of financial markets has been changed by understating inflation via long-running central bank interventions which causes a cascade of asset bubbles.

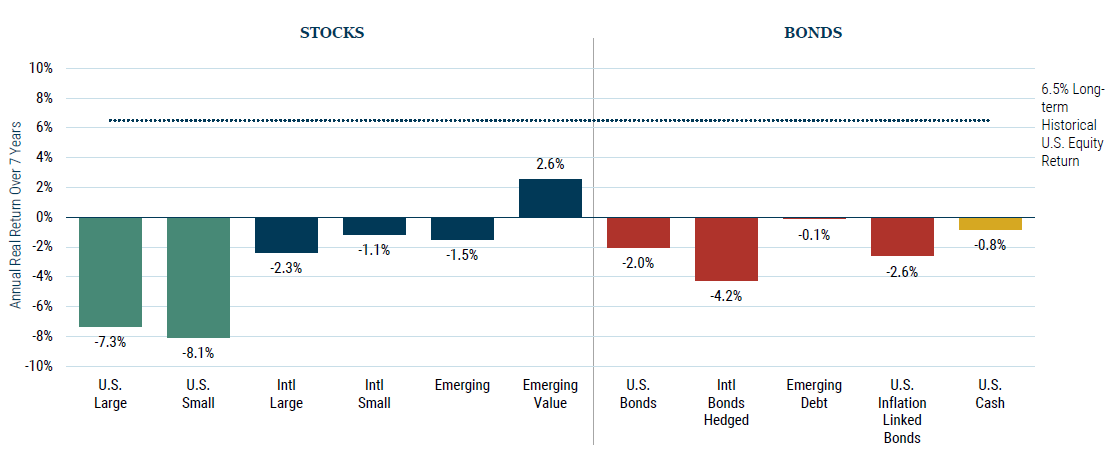

The two statements above were supported by the following chart of historical 7-year forward returns based upon present valuations.

The conclusions from last week can be summarized by saying asset prices are not cheap, but the conditions encourage high valuations continue to be supported by our leaders.

This week we look at how normal people are impacted by the choice of our leaders to continue to embrace profligate monetary policy and turn a blind eye to the ensuing asset inflation.

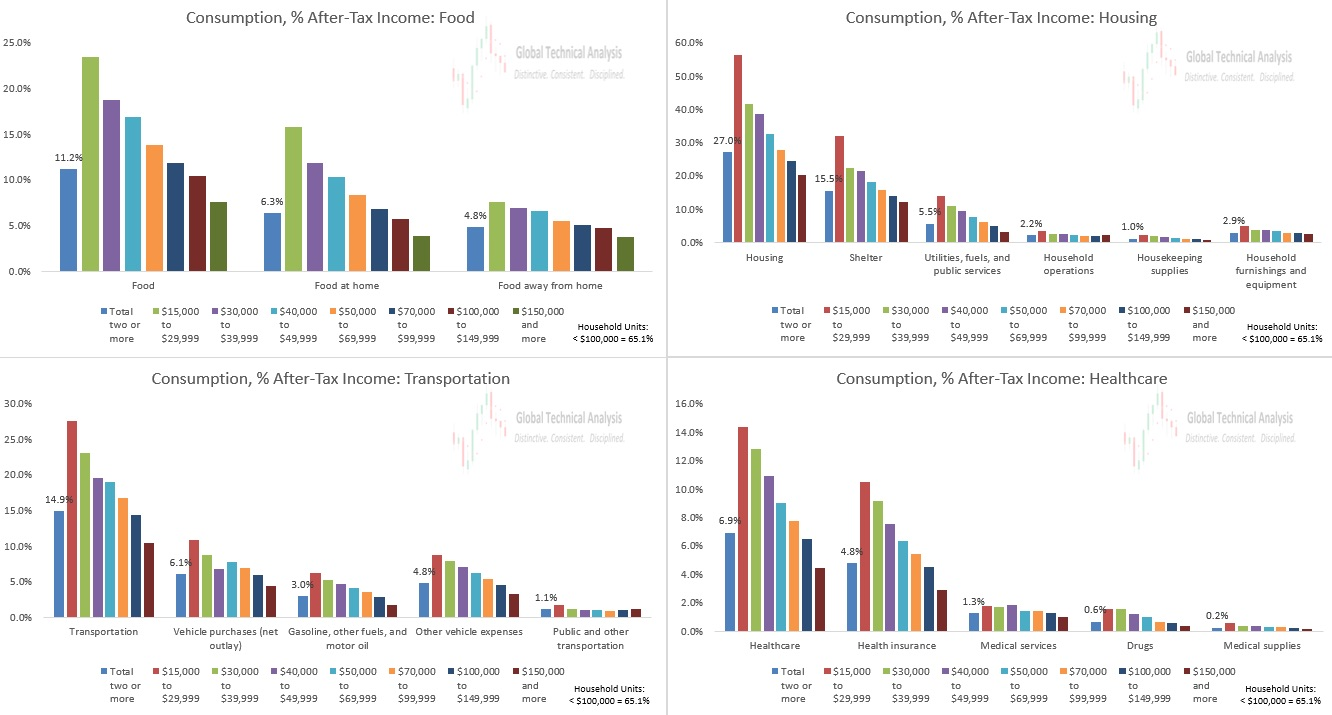

Let’s begin with a matrix of charts. (US data – please spend some time looking at this data as it supports the rest of the letter).

The summary statement with these charts reads: The average household of two or more people consumer 60% of their after-tax income on Food, Housing, Transportation and Healthcare.

This is mathematically correct and accurate but let’s see if we can coax some more real-life impacting ideas from the statistics.

First, let’s define the spectrum of households.

In the US, 65.1% of households have an income LESS than $100,000 income per year. That is the group this report is going to focus on.

Second, let’s not forget all of the single person households which have lower average income levels than the two or more definition. Suffice to say the under $100,000 in income category, when including ALL households in the US, is higher than 65.1%.

Watch what happens to the data when we take out the households earning more than $100,000. (I’ll break it down completely for the food sector of the data and then just include the overall results in the summary).

The average food cost for the entire study was 11.2% of after-tax income. When the households earning more than $100,000 is eliminated from the study the food cost percentage of budget jumps to 16.8% of after-tax income. This occurs because the data set drops out the 10% and 7.5% budget figures for the $100,000-$149,999 and the $150,000+ groups respectively.

So now, here is the data for ONLY those earning less than $100,000 per year in each category:

Food = 16.8%

Housing = 39.8%

Transportation = 17.6%

Healthcare = 11.2%

The total expenditure of after-tax income for those households earning less than $100,000 is 85.4% rather than the above stated 65.1%. That is a huge difference.

Let’s take it one income level lower. The next calculation uses after-tax household incomes of less than $50,000 per year. The total expenditure for this group of households on food, housing, transportation and healthcare is…119% of household income!

Welcome to 2021, where a significant portion of society actually goes further into debt every single year.

Does any of this surprise you? Honestly, I was not surprised one bit.

Will it ever matter? Only if indebted households see their asset drop in value.

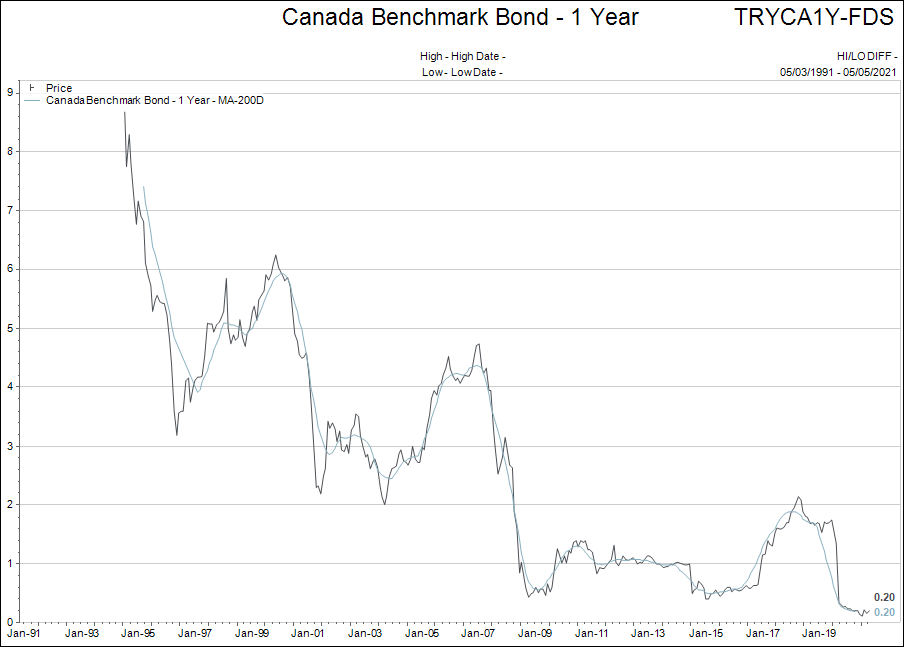

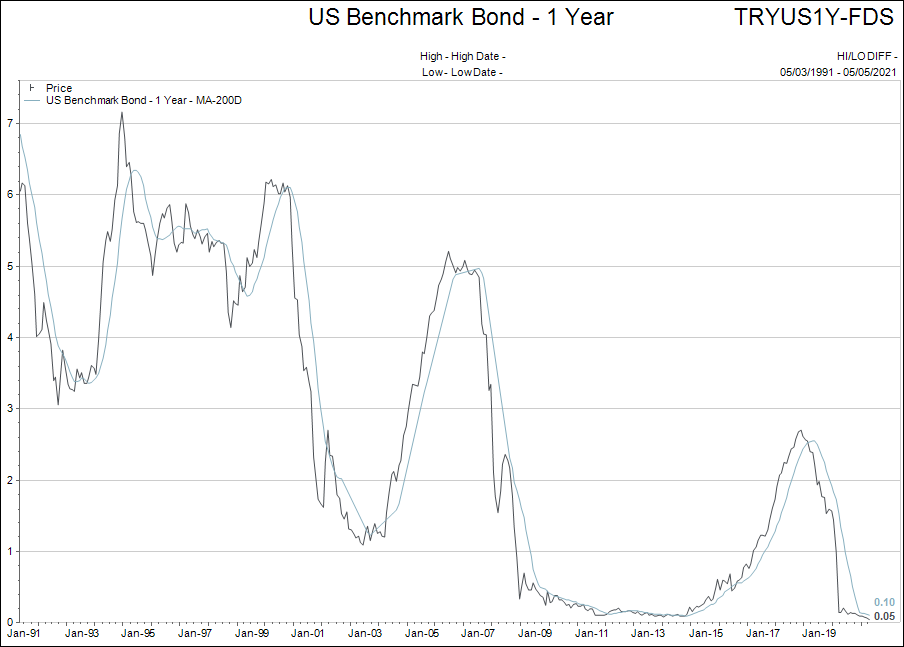

What would cause a drop in asset prices? Higher interest rates.

Therefore the charts of short term bond yields wrap up the comment for the first week in May.

For anyone that found the Tri-annual Review somewhat long and difficult to understand, hopefully this week’s editorial brought it home to more relatable themes.

How can interest rates remain to be the lowest in recorded history with rising inflation and bubbling asset prices?

Something to ponder.

As always, your questions and feedback are encouraged, please email me it you’d like to set a time to chat.