“House Money”

People are feeling the “richer than you think” vibe.

With the ramped up house prices this spring, equity take-outs leading to larger than usual discretionary spending, is on a serious rise.

In a sense, people feel they are playing with “the house’s money” both literally and figuratively.

This week, I am going to swerve out of my lane and discuss some dynamics playing into the real estate markets right now.

News that real estate markets are in a frenzy is not shocking to anyone. It’s doubtful that any of us have had a week go by where we have not been bombarded with some level of conflict about high real estate prices.

Obviously, new buyers feel pressure to buy and lock in a price. Many new buyers, who don’t have the luxury of a “cash or no subject offer,” have just given up; their “subject to” offers are rarely considered in this competitive environment.

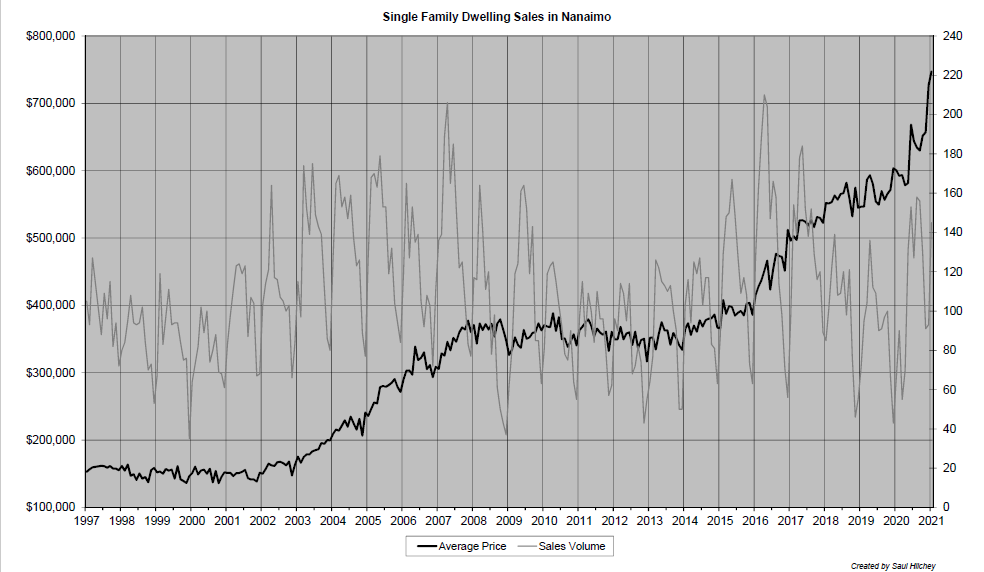

Below is a graphic of the average price of a single family dwelling in Nanaimo along with sales volume in grey. (H/T to Saul Hilchey in our Nanaimo RBC office).

There is stress created at all levels when real estate markets get this amped up and out of control.

- If you are trying to move, you are reluctant to list your home before you find something to buy. You are not sure if you will find an adequate choice AND, on top of that, you might sell your place too cheap relative to what you will pay for a new place if it takes six months to find.

- Realtors working with buyers can spend a lot of time with their clients on many different deals and not be successful in securing a purchase when there are competing bids. This is a frustrating process.

- Builders and trades are unable to offer firm quotes due to rapidly rising commodity costs. As their bids become less reliable, discretionary projects get delayed.

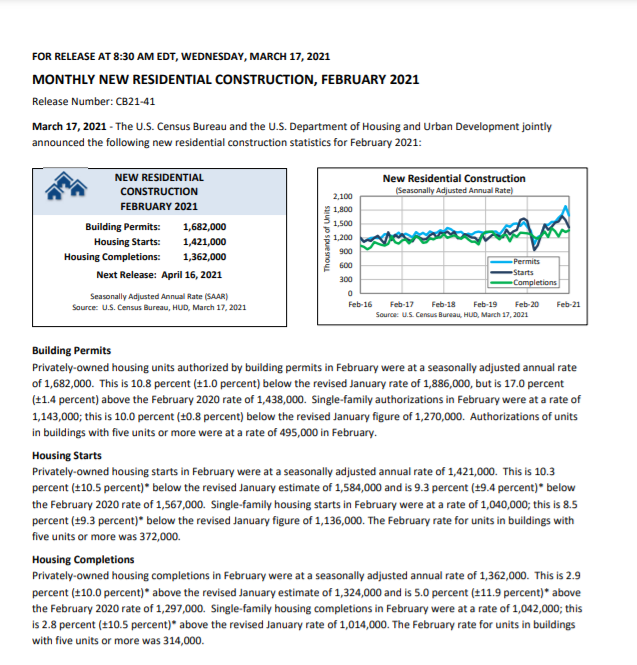

Check out the US housing starts and permit data below from March 17, 2021.

Notice both housing starts and building permits were down 10% in February. Starts being subdued because of February weather conditions can be can rationalized…but permits?

Maybe building costs have risen to a point that people are deciding to wait before even applying for a permit?

It will take a few more months of data points to see if real estate is actually leveling off. I guess I was just surprised by the weak US data for February, especially on the permit side.

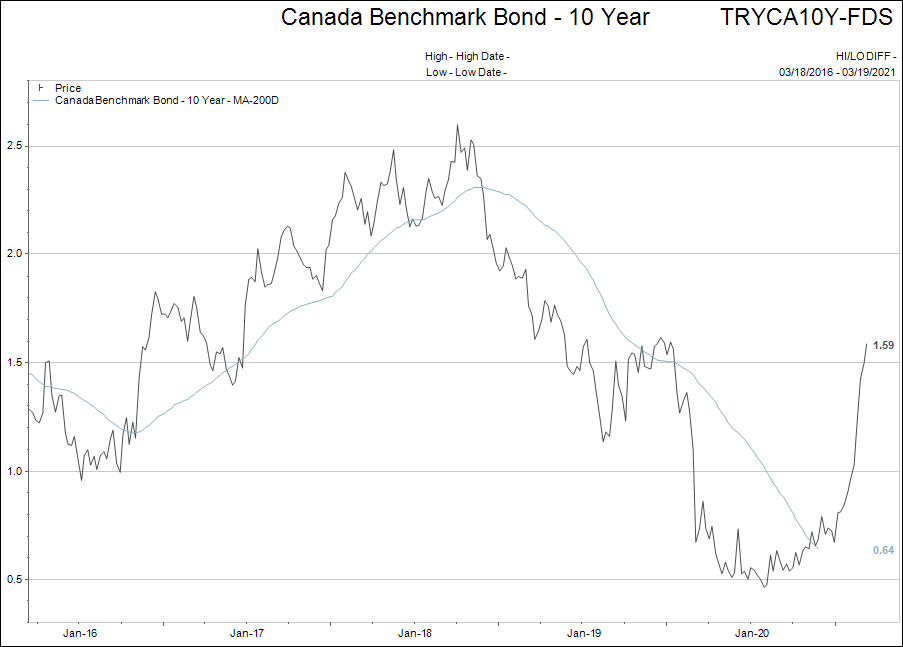

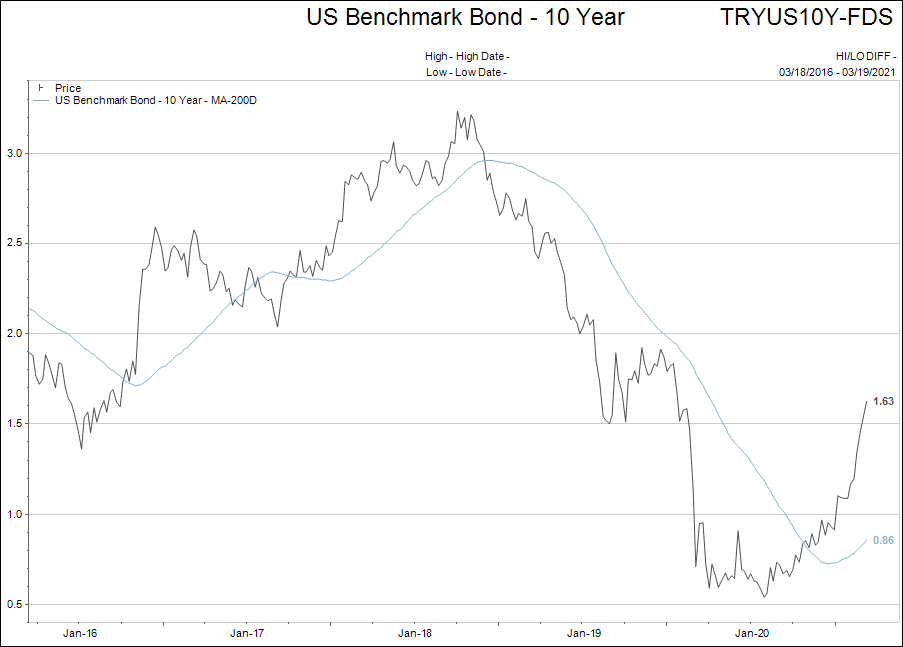

The other key factor playing into real estate is the interest rates. Interest rates are my key theme for 2021 and I promised to frequently review them in these weekly notes.

Below is the yield on the Canadian and US 10-year Treasury bonds.

As yields work their way higher, the pressure on real estate markets builds.

People have bought real estate using floating mortgages that are sub-3% for years now. When the average mortgage is starting to push upon $600,000, the cost of rising interest rates is quickly factored into real estate prices.

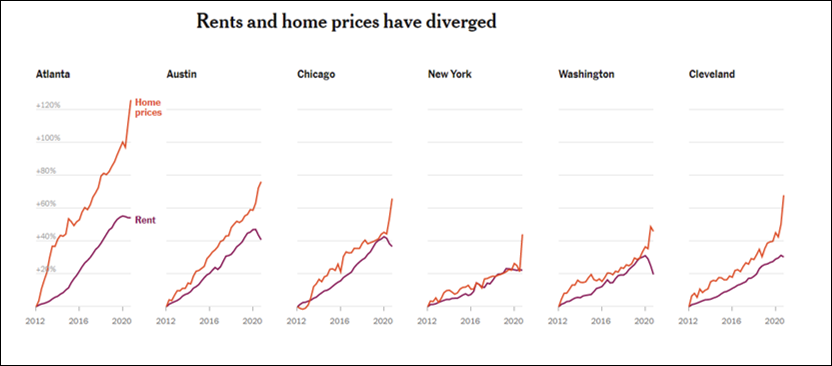

The great irony in the government inflation data is that it captures little of what I am describing above. Let me explain, illustrating with use of the New York Times chart below.

One of the other aberrations of the present time is that, as real estate prices and building costs are rising, rents in major US cities are flat for single family homes to declining for urban condos.

This means that the “rental equivalent of housing” is not reflecting the higher costs of real estate.

When you buy or build a house, the price you pay is not what the Consumer Price Index (CPI) takes as a data point to calculate inflation. It uses the approximated amount you could rent your house for, for its calculation.

For example, if you pay $700,000 for a house that’s worth $550,000 a year ago, but the rental market says that house would now rent for $100 per month less than a year ago, the CPI would calculate that as DEFLATION.

Seriously, the official government data would say the cost of housing actually declined!

What this means is that much of the inflation seen in housing is not being captured in the official data, which therefore, skews the CPI lower and makes it less likely for the government to act to lift interest rates.

On the other hand, the bond market is where investors meet to buy and sell bonds. They are not handcuffed by the stupidity of the hedonic adjustments of the official CPI data. That is why bond market interest rates are leading the government’s choice to raise interest rates.

There are a lot of moving parts to this story. Maybe the best summary statement I can make is to keep an eye on interest rates. Almost everything else in the world will takes is price cue from what happens in the bond markets.

Bank Stocks

The banks have had a nice recovery in price after their swoon a year ago. Rising interest rates and a “steepening yield curve”[1] have been good for the price of bank stocks.

For those wishing to “sell high” I would be comfortable switching SOME of your bank shares to another dividend paying investment.

If you want to talk about this idea please send me an email and I will give you a call.

Two Speculative Buys

Two company stocks have broken out from consolidating patterns. Both are tech names and both have had news that changes their risk/reward structure asymmetrically to the upside.

BOTH ARE VERY HIGH RISK AND OFTEN MOVE 10% IN A SINGLE DAY, in either direction.

If you are interested in building a position, send me an email.

Admin Note

With tax season in full swing, please reach out to Megan if you have questions or concerns regarding any of the information that you have received, or if you would like to authorize Megan to speak directly with your accountant or tax preparer.

[1] The gap between the yields on short-term bonds and long-term bonds increases when the yield curve steepens. ... A steepening yield curve typically indicates that investors expect rising inflation and stronger economic growth.