Congratulations, We Are There:

The Most Expensive Stock Market in History

A client asked the question from the text of the Year End Report last week why was the “great mistake” such a great mistake?

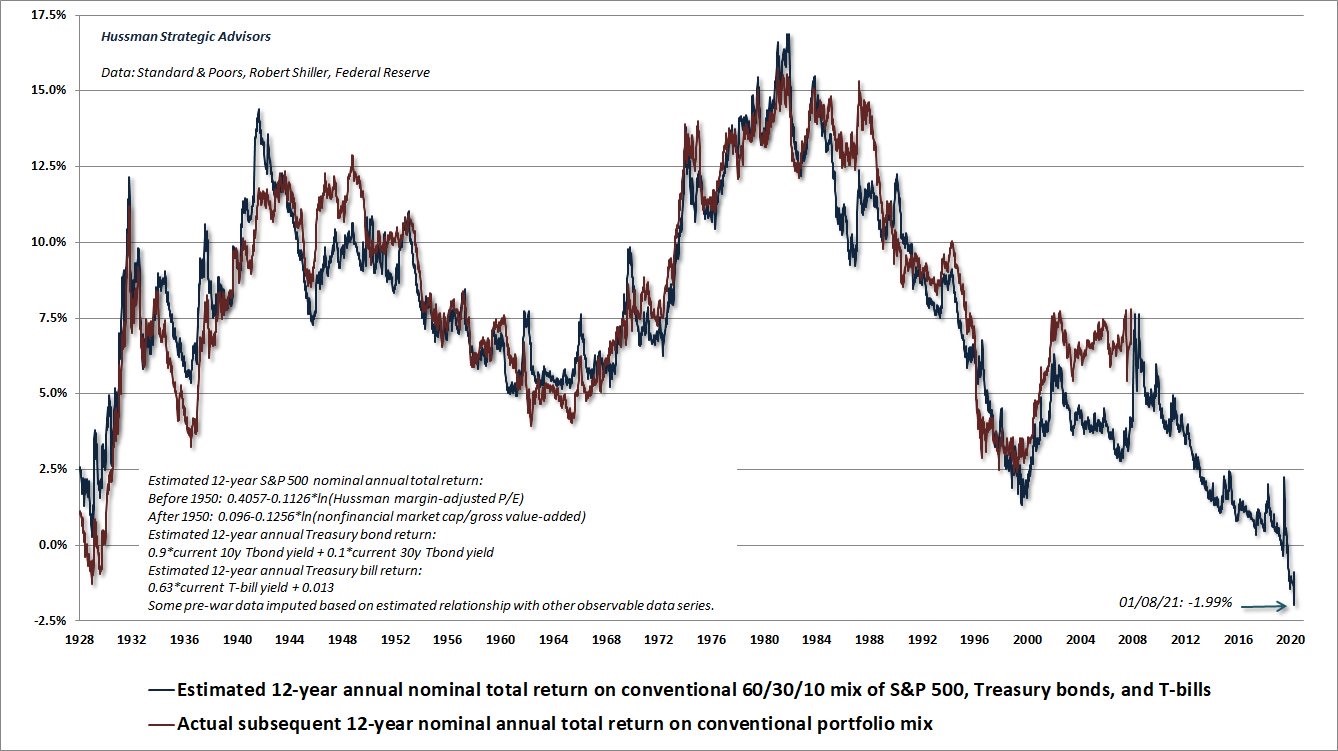

The great mistake references leaving interest rates too low and continuing to print money more than a year after the 2008 bubble bursting; the chart below is the best evidence showing why it was such a great mistake.

It references the expected 12 year compound rate-of-return for US stocks, which now stands at -1.99% (John Hussman of Hussman funds).

The blue line tracks the “estimated” 12 year returns relative to present valuation and the red line tracks actual rate of return.

In general terms, the valuations tracked to arrive at these estimated rates-of-returns are “discounted cash flow” in nature. Why I mention this is because, in an asset bubble, fundamental valuation is irrelevant.

By enabling the bubble to continue to grow the central banks managed to save the banking system, but aided and abetted large asset price dislocations along the way that ultimately drove the world to the point it finds itself at now, with massive wage and wealth disparities.

The easier way to understand the chart above is to envision a $100 bill sitting on your mantle at home. You cannot touch it until January 1st, 2023.

The $100 bill represents the stock market. When you buy a company (stock) it is supposed to pay you back from its profits with capital appreciation and dividends. The lower price you pay for the company, the higher the anticipated rate-of-return.

When the stock markets are “cheap,” the companies you can buy have shorter payback periods for your investment.

Long term, your rate-of-return is based largely upon your starting point valuation of the company you buy.

The question is, what price are you willing to pay to get an acceptable rate-of-return over the two years?

Imagine you have $60 in your pocket to spend today, or you can give it to a company for two years and take the $100 on the mantle.

Most would choose to invest for the two years and have the $100 on the mantle in 2023, since a 65% rate-of-return is pretty good.

What the opening chart is telling you is that, based on fundamental valuation, you are having to pay $102 today so you can get the $100 on the mantle back in 2023.

Why would anyone do that?

There is only one reason why people make this choice, and it is based on the greater fool theory of investing.

In terms of our analogy above, people are guessing that before 2023, someone greedier than themselves will offer some higher number for their $102 investment today that is only going to be worth $100 in two years.

To be fair, the entire stock market is not a bubble. There are some decent values left out there.

But the higher the markets climb and the bigger the bubble grows, the more collateral damage that will be done in the bursting.

As stated in the year-end report, it may not be time quite yet to leave the dance floor, but the first week in January was quite unnerving for me on three levels:

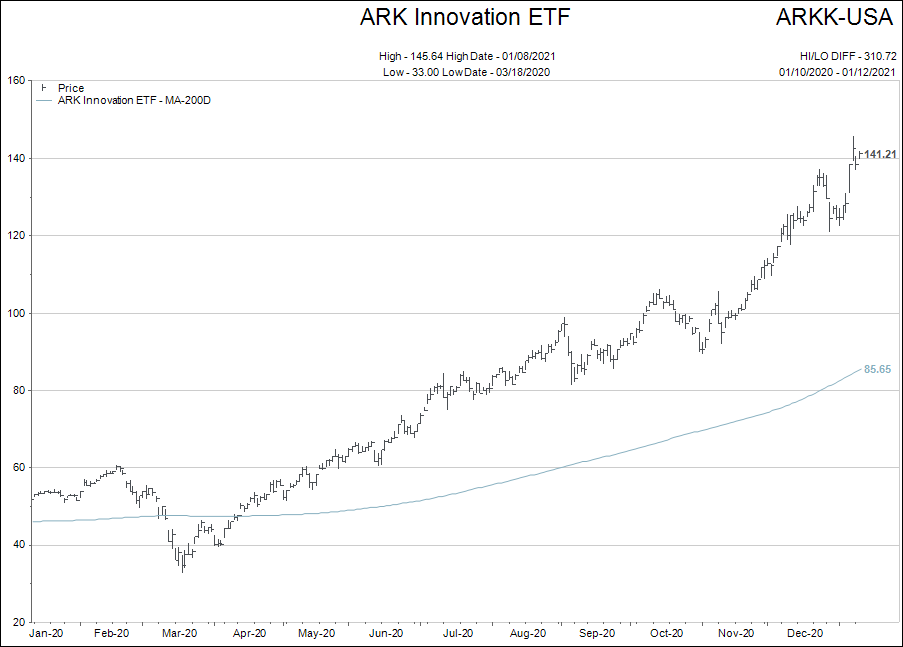

- Stock prices kept rising rapidly.

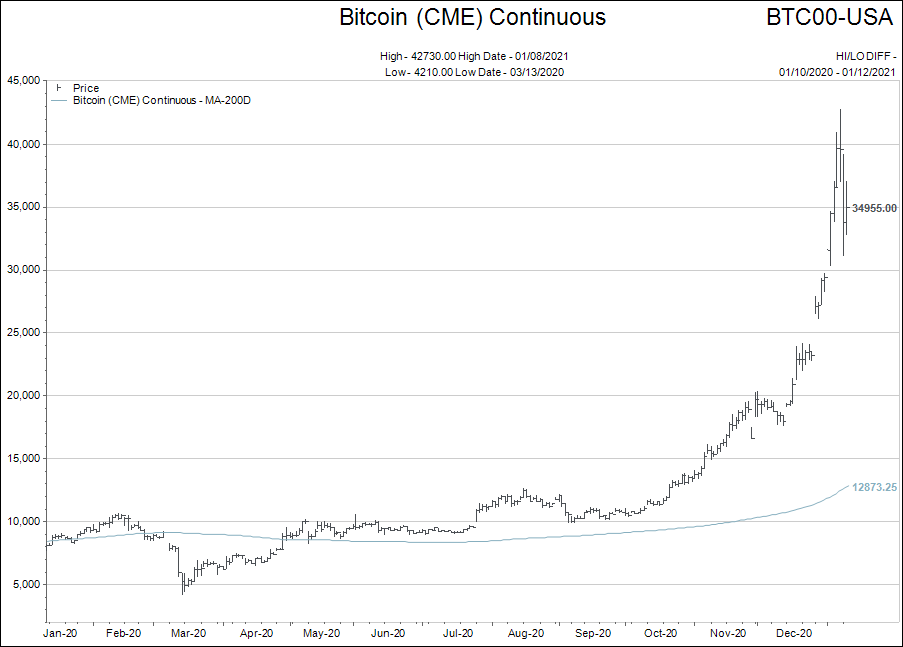

- Bubble assets exploded higher. (Bitcoin, Tesla, SPACs)

A couple of points of reference for the first two charts. (1) Elon Musk, founder and CEO of Tesla, is now the wealthiest person in the world. A year ago, he did not even crack the top 20. His flagship company, Tesla, has never made a profit other than on government tax credits for green energy development. Tesla is an amazing company, but I doubt very much it is worth nearly $1 trillion. (2) Bitcoin is now worth $1.1 trillion. I get the narrative, but I still struggle with how a technology that has been replicated thousands of times over by other “coins” is a store of value.

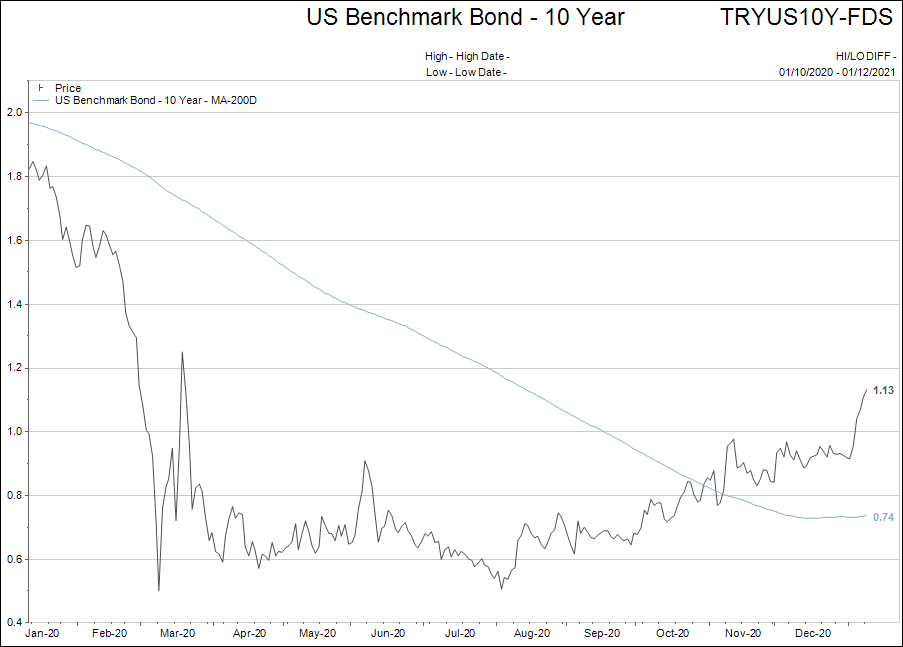

- Interest rates surged higher.

As stated in the year-end report, interest rates are going to be the focal point of 2021, in terms of referencing the health and longevity of the present financial bubble.

Since the start of October, interest rates have been rising and been on a tear higher the past week.

This move higher stands in contradiction to every Fed banker who has been in the media stating that the Fed has no intention of raising interest rates before 2024.

Higher interest rates are kryptonite to the bubbles in asset prices. I have no idea at what level higher interest rates start to matter…I only know they will if they keep going up.

That is the moment where we find the answer to the question posed in the Year End Report.

“Does the Fed implement Yield Curve Controls or do they let interest rates rise?”

At this point the Fed is playing it cool, saying they are not concerned with the rise in interest rates. I will wager that coolness dissipates if the stock markets correct 10% and the interest rates don’t start to fall.

Summary:

Offering advice to clients in the present marketplace is a mix of folly and hubris. Nobody knows what comes next.

Rather than offer advice, my goal is to let the markets themselves lead us to what we need to do next.

As long as the bubble isn’t threatened, we can stand put for the most part.

As always, feel free to call or email if you would like to chat. Next week we will look at some strategies to use once the bubble bursts.