A Little Diddy about Jack and Diane

A Little Diddy about Jack and Diane: (Longish read)

With apologies to John Cougar Mellencamp, I want to take a snapshot life journey with a fictitious couple (Jack and Diane) through the last 40 years of central bank manipulation and understated inflation to help you to see why, at the end of the day, the results really didn’t “hurt so good,” (couldn’t resist).

Jack and Diane met in high school in the American heartland during the mid-1970s. Jack was planning on becoming a football star but, at the time, was working part-time at the general store. Diane was planning to become a nurse and have a family. The summer after high school graduation, Diane got pregnant and in October 1975 they got married.

The hardware store gave Jack full-time work. They rented a cute little place to settle down, and Jack sold his newer pickup truck to buy an older one for a little extra money to furnish their new home.

The 1970s were a time where wage and price inflation were rising from what had been a very long term stable base. Homes were in high demand and good paying jobs were becoming more abundant. The service sector was a fraction of the size that it is today. Labour unions were strong as employers needed to keep their workers because they were hard to replace.

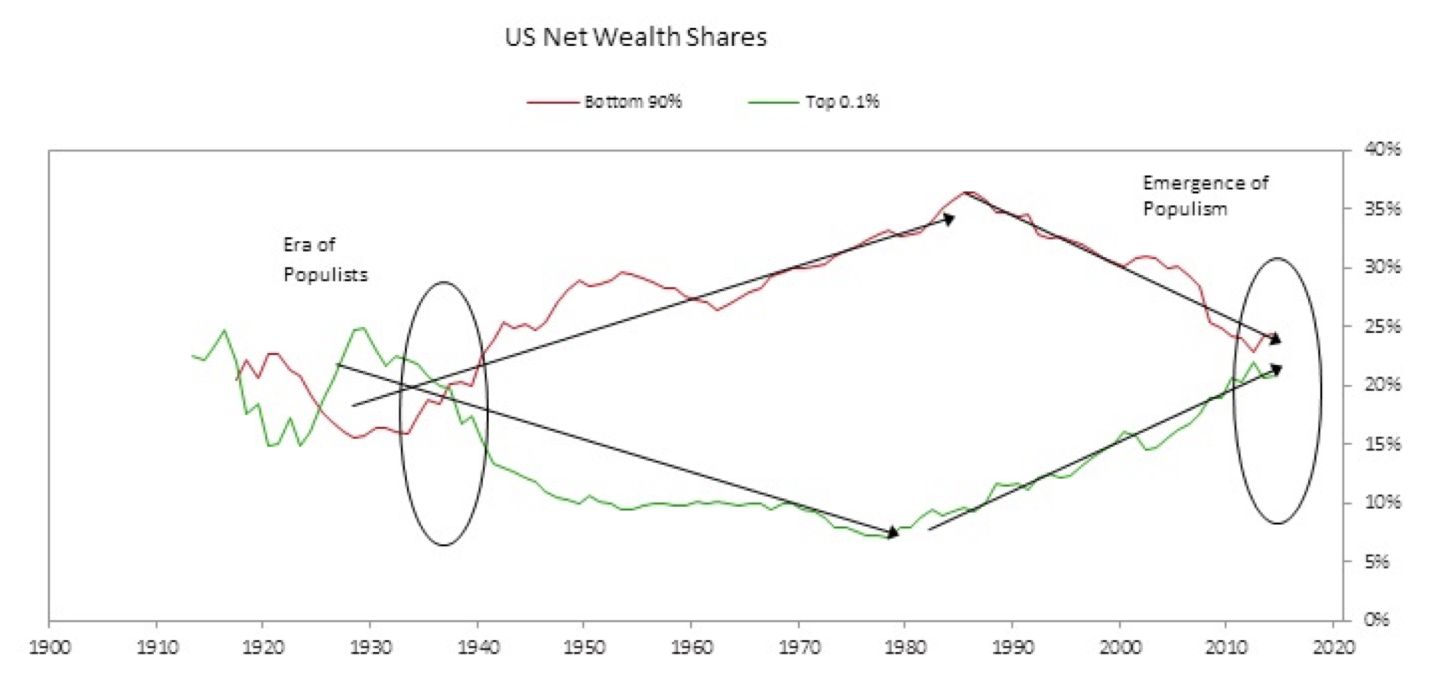

Interestingly, this time in history marked a generation low in the wealth and income inequality.

The steel mill across the county line was expanding. They were offering higher paying union jobs and on the job training for trades.

Diane had picked out a pretty little pink house with a white picket fence and enough room for now two-year-old Carla, and her soon-arriving sibling, to have their own bedrooms.

Jack thanked the owner of hardware store for giving him full-time work when he needed it, but it was time to learn a trade to last him and his family the rest of his life.

Diane’s parents helped with the down payment; Jack got the new job at the steel mill that was billed as “the last job you’ll ever need.”

Jack and Diane could not sign the purchase agreement for their new home fast enough. Home prices were rising….and so were interest rates.

The late 1970s were a unique moment in financial history.

They were literally the “upside down” of the present day MMT based financial narrative. The economy was experiencing significant supply-side restraint and prices of everything were ripping higher.

The other reality of 1977 – 1981…the government measured inflation accurately. This means that Consumer Price Inflation (CPI) was based on a non-hedonically adjusted basket of assets that remained consistent. It also meant that Asset Inflation (home and stock prices) were used as a component of measurement in the calculation.

The chart below is taken from Shadowstats.com, and shows the CPI inflation rate calculated as it was in 1980, in blue and then shows the government published CPI with hedonic revisions in red.

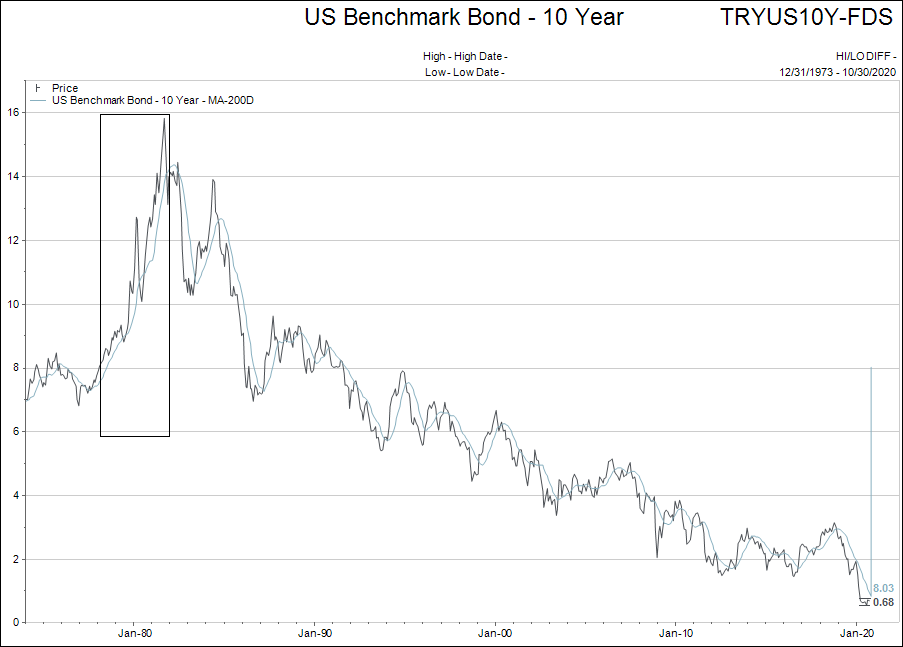

The Fed Chair of the time was Paul Volker. He made a choice to get ahead of inflation by lifting interest rates. It took some time and 20+ per cent mortgage rates for Volker to have his way with inflation…and there was some serious pain for the American economy in the process.

Thankfully, Jack and Diane had locked in a 30-year fixed rate on their mortgage in 1977. The interest rate of 10.5% seemed high at the time but now, in 1980, it was downright cheap.

They were not out of the woods yet.

Home prices had stagnated and there were lots of “For Sale” signs popping up. The steel mill was starting rounds of temporary layoffs to try and keep everybody employed at less than full-time. The union would have none of it. They said “the company is bluffing weakness before our next contract so vote down the proposal to less than full-time work.”

A year later, the housing market fell apart, the steel company shut down for a “period of time until markets improved” and Jack, Diane, Carla and new addition David, found themselves in a tough spot.

They used up their meager savings from the previous five years and Jack found some good paying work in Alaska to make ends meet. They were considered…lucky!

The interest rate peak of 1982, was a moment where the Fed looked into the financial abyss and did not like what it saw. It was the Biblical equivalent of God swearing to never destroy the earth again by flooding when the Fed decided to never again to tell the truth about inflation and never destroy economic growth with crushingly high interest rates.

In hindsight, this was where the roots of today’s “upside down” financial world took hold.

At the time, in the early 1980s, that day of reckoning for these looser monetary choices was known to be far off in the future and, therefore from the political spectrum, an eternity away.

By hard work, sacrifice and scrimping, and lots of family/community support, Jack and Diane made it through 1982/1983. They kept their house and Jack was one of the first people called back at the steel mill.

Life was getting back to normal but their young family was right back to where they started financially. No equity in their home and no savings.

But that didn’t last long…

The Fed had a brand new plan.

With lower interest rates and higher leverage, it was an asset inflation based plan.

Politicians loved the backdrop of this plan. No more worries about the brakes being applied at the wrong time; hopefully no more economic screeching stops.

Jack and Diane were getting ahead finally. And their little town where they lived was prospering again. Good times were back…life was good.

It was time to buy a nicer home. Bigger yard, a pool in the back for the kids. Interest rates were much lower again. Time to get their slice of the American dream.

Wall Street loves to be 20 minutes smarter than everybody else.

With bank regulations easing, lower interest rates, and a healthy economy, Wall Street saw opportunity in the massively undervalued assets sitting on American corporate balance sheets.

Investment firms like Drexel Burnham and names like Michael Milken exploited the new financial landscape making obscene profits for the time.

If you want to get a flavor for the time watch the original Wall Street movie from 1988, or just the famous Gordon Gecko “Greed is Good” speech here.

What had been happening was that working people were getting ahead, but the wealthy people were getting waaaay ahead.

The formula that is still true today, became a reality then: More assets equal more wealth. And more wealth equals more wealth to inflate via higher asset prices. The gap between rich and poor was magnified by asset ownership.

Jack was offered an option at the steel mill to put some of his wages into the company stock. The steel company would give him $0.15 for every dollar he put into the plan. Jack and Diane figured their budget and put as much as they could into the plan. Who turns down an immediate 15% rate of return with stock market growth attached?

The plan worked great for about two years, but in early 1987, some guy the media referred to as a “corporate raider” came and bought out the steel company to seize control of the undervalued real estate assets and the over-funded pension plan.

Jack gained $1,085 on the $2,200 worth of stock he had put into the plan when the buyout took place. This was cause for a celebration but a year later, lost both his job and his pension plan from the steel company. The steel mill itself was deemed “collateral damage” in the leveraged buyout carcass mauling by Wall Street.

The 1987 stock market crash seems almost quaint in terms of today’s bloated financial reality.

Don’t get me wrong. It was a huge deal.

It defined the beginning of my career in the investment industry. But the financialization of the world was only about to begin, not coming to an end as so many thought at the time.

The bond market again played a huge, but different role in the stock market crash of 1987.

It was not the high yields on US Treasury bonds that started the cascade down this time…it was the “junk bond market.”

It was amazing to see how interconnected the financial markets had become in 1987. Stocks, bonds, currencies, futures, options, Ted Spreads, bank lending…they all seemed to converge so that when one had trouble they all had trouble.

The 1987 stock market crisis was also the baptism by fire of newly minted Federal Reserve Chairman, Alan Greenspan.

The once “hard currency/gold affectionado,” quickly earned his stripes to be known as “EASY AL,” who never saw a problem that lower interest rates and more central bank liquidity wouldn’t solve (Alan viewed later after being named world savior).

Interest rates were quickly suppressed, banks and savings and loans were recapitalized via the Bill Seidman directed initiatives that led to the “Resolution Trust.” The US Federal Reserve backstopped it all. It was genius and magic all rolled into one…

The aftermath of 1987, gave Wall Street the greatest gift in the history of finance. It was also the gift that just kept on giving.

The gift was named “moral hazard.”

What it meant was that, as a bank or a brokerage, I could lever up my balance sheet as far as possible, and while the economy ripped higher I could enjoy massive profits. But if things went south and asset prices fell, I would be bailed out and left in business to enjoy the good times once they returned. Taxpayers would pay my bills.

Jack and Diane packed up their family and moved back into a smaller home. The steel mill reopened but with lower wages and more contracted out work. Jack actually made ok money since he was working a side hustle putting in sprinkler systems on weekends.

Diane was doing some bookkeeping from home too. Maybe they didn’t have as nice of house as before but they owned this one clear and nobody was going to take it away from them.

The kids were at the ages where they were involved in tons of activities too. Now they had the extra money to support those activities. Both Jack and Diane hoped their kids would go to college someday so they started to put a little money aside for that too.

These were good days, the best days, for their family. They didn’t have a lot but they were happy with what they had.

The next 12 years were great years in general for American society. Interest rates fell continually, asset prices rose substantially, the economy was rolling ahead nicely.

Technology was making life easier every day. The jobs market was shifting in terms of both opportunity and skill requirements. Traditional manufacturing was being shipped off shore at an amazing pace, but many new opportunities in service and technology were ripe for the picking.

Play your cards right, and you could strike it rich.

In 1999, Jack and Diane, once again, decided to buy a new house. They chose a place with a little more property this time, and the potential to add a rental suite for the present and to eventually use for aging parents someday.

There was no more need to work weekends. The steel mill was competing on global markets. To be fair, the wages were about the same in 1999, as Jack was earning in 1979…about $19.00/hour when trade unions were at their peak. To compete with countries with cheaper labour, the wage was still just over $19.00 an hour, and it certainly did not go as far as it did in 1979.

But the long stable period of work, and the lessons Jack and Diane learned in the 80s, helped them save and make conservative investments on their lower real income so they would not get caught short again.

Other than a small hiccup in 1998 (that was again pacified by a double dose of Greenspan’s lower interest rates and monetary infusion), the 1990s were good.

During the summer of 2000, Jack and Diane were sitting at their kitchen table with Carla and her boyfriend who informed them that they were engaged to get married the following summer. The family celebrated the announcement with dinner out at the nicest restaurant in town. They couldn’t be happier.

When Jack and Diane were alone after dinner they talked about how they were going to pay for a wedding and do the upgrades on the new house all at the same time.

Jack said he had been talking to a few of his buddies at work and said that the stock market was like a giant money printing press as long as you bought something with a .com in the name…

The Federal Reserve had flooded the financial markets with liquidity to preempt the Y2K fears that computers would crash around the world due to the inability to incorporate going for a 19 prefix to a 20 prefix. The Y2K bug was no big deal, but the liquidity pumped out by the Fed went into asset prices in general and tech stocks specifically.

The Fed being preemptive to an economic problem was new territory. Easy Al Greenspan was only setting a stage that would be played over many times in the following 20 years.

Jack woke up at 6:00 am and turned on CNBC. He saw the stock market futures were green again. Scott McNealy, CEO of Sun Microsystems, spoke about the future of every home having high-speed internet connections and smart appliances. John Chambers of Cisco systems explained the endless possibilities of the fibre-optic highway human productivity.

Diane got out of bed and told Jack he was going to be late for work.

“I don’t know why I bother going to work anymore. I can make way more money sitting here and trading stocks. We have made more than $50,000 since January.”

Diane got that look in her eye…”Jack, you be careful and get your butt out the door to work.”

Jack smiled, “Ok, I know…but we need to go to the bank and get a mortgage to do the renovations and pay for the wedding instead of selling our stocks now. In six months’ time we will sell the stocks and pay off the entire mortgage.

The stock market stopped climbing in July 2001. Then came September 11th.

Jack, we cannot afford to lose this money. Those stocks need to go. If you have any profit left in those things when the market opens again please sell them. I’m scared.

Jack admitted he was scared to…what was happening to the world. Jack agreed to sell the stocks.

But almost immediately, the market started to recover. Jack knew he shouldn’t have listened to Diane. He bought back just one stock with all the money, Amazon…and it fell from $23.00 down to $9.00 where he sold it and swore he would never speculate in stocks again.

At dinner that night Jack confessed to Diane that he had turned their $120,000 account he had so proudly told her about over and over again into $35,000…just slightly less than what they had saved to begin with. Jack said they were lucky, some of his buddies at work were down 90% or more.

The 1998-2001 tech bubble killed a lot of portfolios and worse, scared a lot of people out of the stock investing period.

The bubble needed to be reflated. The Fed had an answer to this problem. Guess what it was? You know, I’m not even going to bother to write it down this time.

By 2007, the economy recovered, stocks recovered and Jack and Diane were now empty nesters at the young age of 52-years-old. It was said you could not even recognize their town in the Midwest. It had grown so much over the past 25 years and it seemed that growth was accelerating.

Jack and Diane started to talk about retirement. By losing the original pension plan assets in the steel mill’s leveraged buyout, Jack’s pension was not going to be enough for them to make it on in 10 years or so. Losing a bunch of money in the tech bubble added to their concerns about the future.

“We are never buying stocks again no matter what you say Jack.”

Jack replied: “You got that right, but I noticed a bunch of advertisements for really cheap mortgage rates on real estate loans that you didn’t even need to put any money down. Some even said they would give you 10% more money than you need for the purchase. Real estate in America is a rock solid investment. Look at our town, it is growing leaps and bounds. We can use our home as collateral and buy two rental houses. By the time we retire they will be worth 50% more than they are now and we can sell them or just collect the rent….”

Once again, Wall Street saw another opportunity to create some extremely profitable products for them that allowed average people to indulge their desire to get rich in an overleveraged way.

The Federal Reserve stoked the fire with crazy liquidity and lower interest rates. Now Fed Chair Ben Bernanke believed it was as simple as pulling a “financial lever” here or pushing an “interest button” there.

But by 2007, two things had become clear. One, the real estate bubble was global, and two, it was growing out of control.

The Fed began to lift interest rates while keeping a flow of liquidity to the financial markets. It was a good plan but the level of greed on the part of Wall Street and the people ran over Ben Bernanke’s subtle attempts to reign things in.

By the summer of 2008, the real estate bubble was crashing everywhere in the world except Australia, New Zealand and Canada. The Fed had to act fast and huge. The movie the Big Short based upon Michael Lewis’s book of the same name does a great job explaining this period.

Jack, what are we going to do? This is crazy. How can a 1% interest rate go up to 7%? Who does that to people?

Jack was out of answers. He had seen this coming and knew about the “teaser interest rates” on the mortgage products they used but figured the houses could just be flipped it if was a problem when the higher interest rates kicked in.

Jack looked at Diane. “We go to the mortgage broker and we see if we can just give them the two rental houses back and they allow us to keep our own with the original mortgage…

By Christmas of 2008, the real estate markets had completely fallen apart. The mortgage companies that were creating these exotic mortgages were in no mood to discuss anything with anybody. Actually, they were often already bankrupt. The leverage on Wall Street was insane. The Fed was going to have to save the day again and bring moral hazard to a whole new level.

The difference was, this time the Fed knew it was in too deep and realized just how much their decision to bail out Wall Street again was going to change the future. But what choice did they have?

Jack and Diane lost the rental houses and their home. Their little town just stopped working. The malls were shut, the businesses shut, and everything screeched to a halt economically.

Jack luckily kept his job when over half of the steel mill was laid off.

They moved in with Diane’s parents for a few months and then went back to a little pink house rental near the first home they bought in the 1970s.

Diane said with tears in her eyes, “We didn’t do anything wrong. We were only trying to get ahead. Why does this keep happening to us?”

The interesting thing about this little ditty about Jack and Diane, is that I actually agree with Diane’s lament.

Humans being human will make risky choices when presented with opportunities that “everyone else” is participating in AND that are being enabled by our leaders.

The economic crash of 2008/2009, was the point in time where some better leadership was required.

It was definitely a time where a new vision of the future was required.

It was absolutely a time when the central banks needed to stop enabling bubbles and get out of the game of enabling the moral hazard of our global financial institutions.

As we know, none of that happened…

Diane’s father passed away in 2015, so Jack and Diane moved back in with Diane’s mother to take care of her.

Jack was tired of the steel mill, but he had to keep going back. As a matter of fact, if his body would hold out and if the steel mill would let him…he would never leave.

But that wasn’t going to happen. The mill had mandatory retirement dates.

…Jack and Diane’s son, David, had moved away to California and been working with a technology company that he received shares in. David had bought himself a place in San Jose about 12 years earlier…just a studio. But he sold it after the real estate crash in 2009, and since his job income was growing quickly, bought a nice house in the suburbs via short sale. It was now worth nearly $2,000,000. David’s company was going to go public and David would end up with about $8,000,000 after tax.

David called his mom and dad and invited them out to San Jose for a visit and a break from reality.

When they got there he gave them a cheque of $1,000,000…

The Jack and Diane story has a happy ending.

I like writing happy endings when I write, but as we all know, the Jack and Diane story is all too common in the US, and there are not many “David’s” out there to bail the parents out.

We are now living with a new bubble.

It is a bubble in government debt and it creates higher asset prices in virtually everything. Some refer to it as the “everything bubble.”

This story takes a look at a long series of bubbles that were all facilitated by central banks that swore they would never do what Paul Volker did in 1976-1982. But maybe, just maybe they need to do something different.

I saw a great Tweet the other day that described the global central banks to a tee. “Kicking the can down the road doesn’t stop when you reach the wall. It stops when you break your toe.”

Where the next four years takes us under whichever party wins the US election is likely going to be historical in terms of centuries. Personally, I see the central banks still having the “river card” in coming year’s rather than the politicians.

We will see…