Stock Market Reality

I am shocked. Shocked, that the US Federal Reserve continues to print money!

The clear sense of sarcasm never really comes through in written forms of communication, but I’m sure those of you who know me know I have no doubt the Fed will keep right on printing.

Actually, the trendy way to say it is: “Fed makes printing press go Brrrrr.”

Even closer to the truth is that every central bank in the world makes printing press go Brrrrr.

The playbook never changes, but the circumstances that need to be overcome are immense.

In the US, there are 40 million unemployed, corporate profits falling more the 25% and martial law due to rioting.

These are serious issues that higher stock prices don’t do much to solve, but as they say, if the only tool you have in the box is a hammer, then the entire world looks like a nail.

Today we are going to dig a little deeper into exactly how and why stock prices remain resilient.

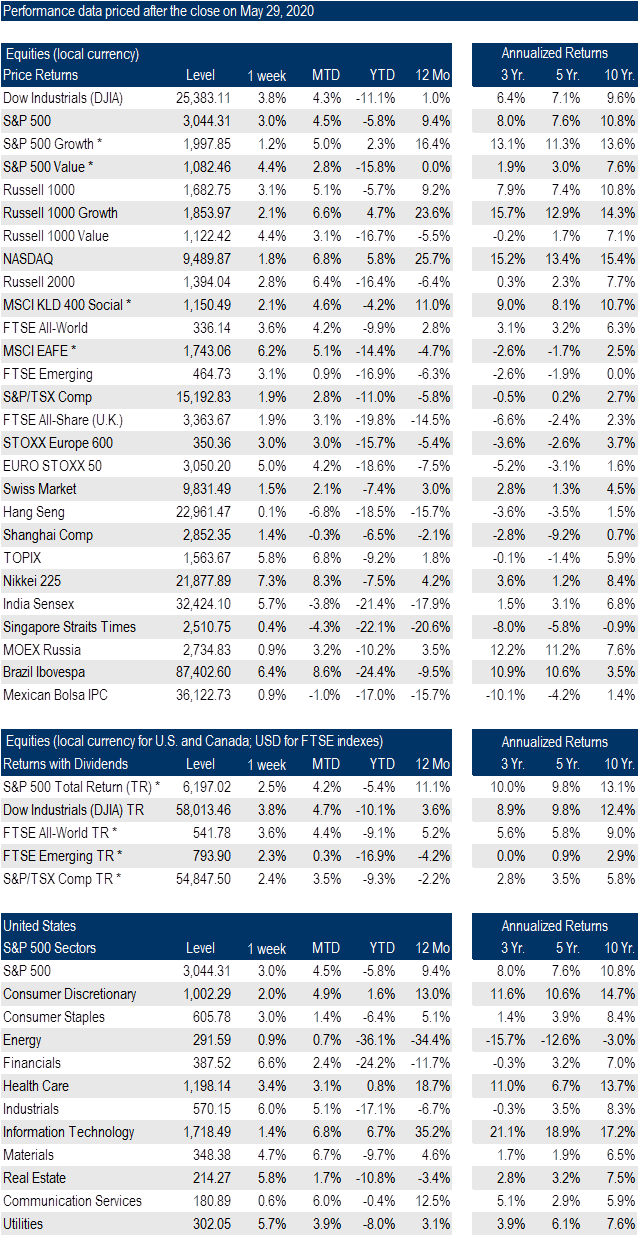

The next page is filled with the short and long term rates of return of the majority of major stock market indexes.

- These rates of return are current up to the end of May.

- Please notice the outperformance of the US indexes.

- S&P/TSX Comp is the Canadian stock market.

- The bottom section shows the rates of return with dividends included.

Outside of the US, the rates of return are pretty pedestrian.

Now, let’s take a closer look at HOW the US market managed to perform so much better than the rest of the world.

The blue line is the price return for the six stock index of Facebook, Amazon, Alphabet (Google), Apple, Netflix and Microsoft.

The red line is the S&P 500 without the six stocks above included in the index. Or the S&P 494 to be more accurate.

The yellow line is the global stock index without the US included.

The chart goes back to 2015 where it was indexed at 100.

Amazing, right?

This story gets even more interesting though.

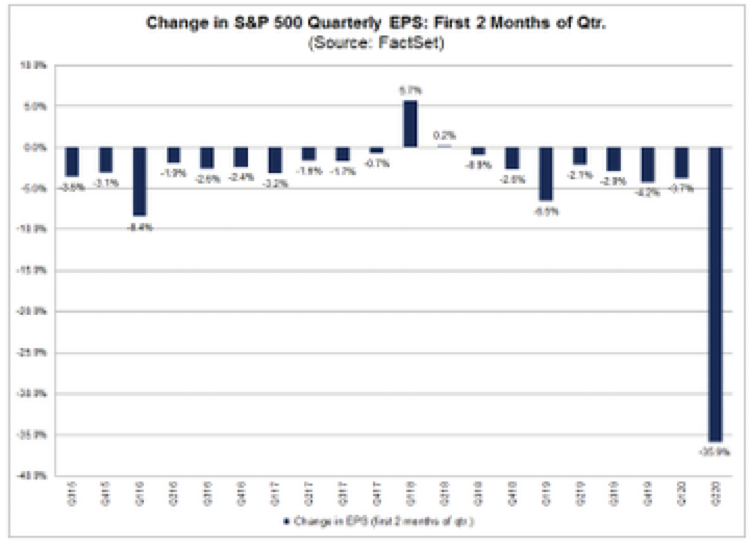

The next chart shows Factset S&P500 earnings estimates back to April 2020. Those are a lot of downward revisions.

Nick, what are you trying to say in these first three graphics?

Basically that liquidity is driving stock markets. Investors have no place else to turn. Bonds pay nothing…GICs pay almost nothing. They have to chase yield.

Fair enough, I have no problem with that as long as people know what they are doing and what they are getting for their investment dollar today.

Now let me get to the absolute nugget I am trying to wrap my mind around at the present time.

The Fed saved the day in 2001.

The Fed saved the day in 2009.

So far, the Fed has saved the day in 2020.

Why was the Fed successful at saving the day in 2001 and 2009?

What are some of the differences in 2020 that could cause a different result?

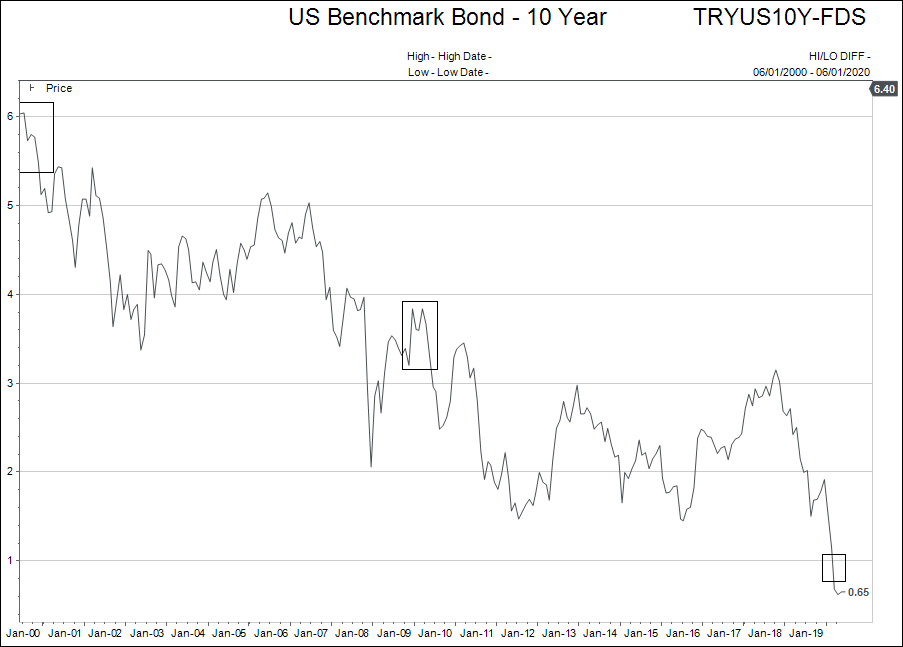

The main difference that jumps to mind is the starting level of interest rates.

In 2001, the US 10 year Government bond was yielding 6%, and in 2009, the yield was nearly 4%.

This time, in 2020, the yield is less than 1%.

Lower interest rates are not going to be as powerful part of the arsenal for the Fed this trip through since there is little room to lower them.

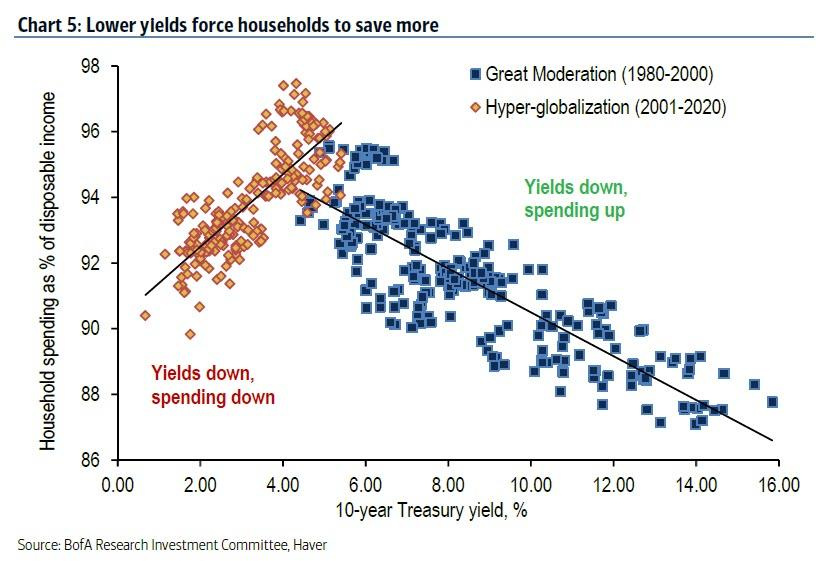

Actually, the next chart shows that the low interest rates are the Fed’s enemy in terms of stimulating the economy, but a “dream come true” for asset prices.

Below is a scatter chart of a monthly plot of what the US 10 year Treasury bond was at (x axis) and the percent of total household income spent (y axis).

It makes total sense to me that when the 10 year bond is yielding 8% - 16% that people would save more. Those are pretty good returns in a bond.

As 10 year interest rates approach 4%, people spend the highest percentage of their income meaning that they save the least. This makes sense too, it is cheap to borrow and 4% isn’t a great return.

But look what happens when interest rates get below 2%. All of a sudden, people start saving a larger percentage of their take-home pay.

Why?

At near zero interest rates, it is cheap to borrow and you get nearly nothing on your savings in interest.

This same curve was seen in Japan and in Europe which are both way ahead of North America in this zero interest experiment.

I get how that can be good for stock prices in the shorter term…but think about it: Does it make sense long term if economic recovery is muted?

Last pieces of the puzzle.

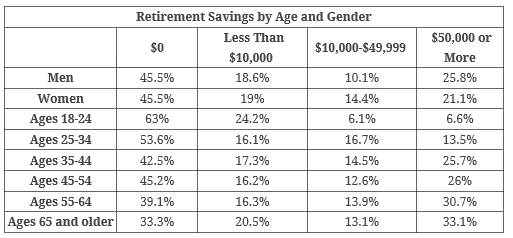

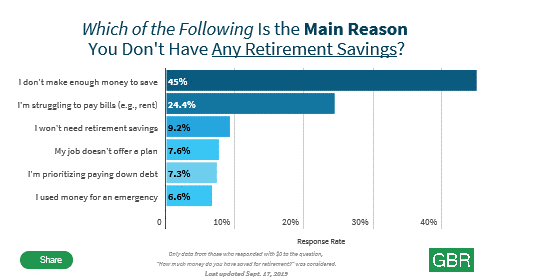

The matrix below is from 2019 in the US, and shows retirement savings by age and gender.

That should get your attention. Here are the reasons people gave as an excuse as to why they have no money saved.

Summary:

It’s time to tie this all together in a tidy package.

The “glass half full” view of the stock markets is that it is the “only game in town” if you want to make a rate of return on your capital.

Everything discussed in the editorial above is irrelevant if you just need to make some return on your money to live in retirement.

I can just hear people say: “Yes, there is a risk to your capital invested in stocks, but at 1% or lower in a “guaranteed investment” the only thing guaranteed is I will go broke.”

So you hold your nose and buy…

The “glass half empty” says this makes no sense and the realities of the worst recession since the 1930s, a global pandemic which is now endemic, and racial violence in the streets will cause stock market prices to come back down to earth.

The relative weighting of glass half full and glass half empty in portfolios is based upon how much income someone needs to create.

When I look at the average financial plan done for clients a rate of return of around 4% is required to make it work.

That is not going to happen in GICs and Government bonds.

Therefore, investments with yields that carry some risk must be used to create the portfolio.

I’m not saying it was fair for the central banks to force that situation upon investors…but that is the truth.

Please feel free to call and chat about this comment, or email your thoughts and feedback.