Financial Market Narratives

Before we start the weekly comment, I want to highlight an important point about where the financial markets find themselves at the present time by way of analogy.

The family was gathered together after the memorial service for a dear friend.

As a group, they didn’t see a lot of each other. They were individually busy and collectively not a close family. But there is something to be said for making appearances.

Among the older adults, comments like “it was such a tragedy” and “how will his family go on?” were mixed with “I always knew something like that would happen to him. He brought a lot of this on himself. Who knows what he was into?”

Was it an accident? Was it suicide? Maybe even murder?

The police were still involved, no information other than what was in the public news was available.

The younger family members were sitting together mostly talking about their beautiful lives. The deceased family friend was not a topic of interest in this circle.

Rather, it was the usual “this is my exaggerated, awesome life” conversation, with a little smattering of gossip to keep it lively. After a few more drinks, this group might be worth a listen, but that was a few hours away yet.

There was a knock at the door. A woman nobody knew came into the room and locked eyes with one of the young men. She was tall, well dressed and commanded the rooms attention as she entered. The targeted young man walked over to speak in private with the woman. The room went quite as if everyone wanted to hear what she had to say.

After a few words were exchanged she kissed him on the cheek and left. The young man paused, looked back at his family, then turned and walked out the door.

If this were the opening scene of a movie or start of a novel, the question you would be asking yourself is: “What was the connection between the woman and the young man?”

The insinuation is there is also a connection to the deceased, but there is no way to prove that point by what I have described so far. Actually, you don’t even know for sure that he followed her out when he left the room.

Now, imagine the conversations that would occur in the room after the young man left.

Nobody would know anything about the woman or why the young man left, but that would not stop the stories, speculations and outright lies that would be flying around the room.

Why? Because that’s how the human mind works.

We struggle with sticking to the facts. Especially when there are not enough facts to know for sure what is actually happening.

We like to create a narrative that fits our experience and then tell that story like we know it is true.

In so many ways, this is where the financial markets find themselves in how investors, pundits, analysts and the media are handling the lack of clarity of what is going on in the economy.

Due to the lack of facts, people are just making stuff up that fits with what they believe, or in many cases, want to be true.

That is not a condemnation. That is humans being human.

The economic narrative at the beginning of 2020, was a story that had been in place for the past 11 years. Due to its longevity, it was rarely challenged by mainstream financial types.

The COVID-19 induced recession and economic upheaval created a huge disruption for the long-standing narrative. Many new and frightening narratives began to take shape.

These narratives were crafted out of a lack of data and were influential in “locking down” the global economy until more information could be gathered. The results from these choices were both good and bad.

But now, still in a place where the world lacks good data the narrative has shifted yet again.

There are those who say the right thing is to gradually re-instate the economic system prior to COVID-19. This will allow for safer conditions for those who fall ill and make outbreak transmission lines easier to retrace.

There are others who say, this only delays the inevitable. Everything should be opened and people should be allowed to make their own choices as to what they want to do and not do.

But here is the key.

As convincing as both of these groups can be in the narrative they spin to support their position…nobody really knows what the right choice is due to the lack of facts.

On April 24th, I shared a comment that showed a BULLISH, neutral and BEARISH forecast. (You can see it here)

Any one of those three forecasts have not become any more or less likely to occur in the past month. Not even slightly…

My encouragement to readers is to stay nimble in your approach to your portfolio of investments and remain open to real data points as they are announced…not politically charged narratives contrived to suit individual positions on both sides of the political spectrum.

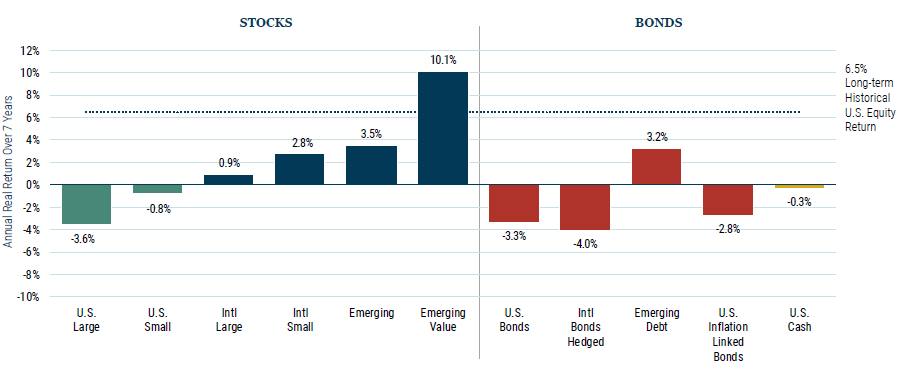

A Deeper Look at the GMO Rate of Return Chart

The following chart was posted last week. A number of you asked about it so I thought I would feature it here with a deeper description.

The chart is updated on a quarterly basis by GMO. Historical commentaries are also available online, if you're interested in taking a closer look, please let us know.

The return figures on the graphic represent “annual real rate of return over a seven year period.”

Let me spell out the link between the GMO graphic, the global shift in the COVID-19 response, and the narrative driven financial markets.

If markets are viewed through the lens of historical valuations normal economic conditions, the compounded returns above would be expected.

But markets are not valued normally, they are near the most expensive of all time. Nor are global economic conditions anywhere near normal, they are in disarray.

Therefore, a narrative must be told to justify current prices on financial instruments and real estate.

The narrative is backed by the liquefying actions of the central banks and these actions are now beyond any logical description in magnitude.

As an aside, I took the United States from Confederation to September 2007 ($7,379,052,696,330.32) to print as much debt as it did in the past two months. ($7,262,665,000). Think about that for a few moments.

Supporting asset valuations is getting to be an expensive proposition.

I answered those who asked about the GMO chart last week, that it does not tell you anything about what financial markets will do in the short term. It does tell you a lot about your expected long term rate of return.