What Do Apple Shares and Nanaimo Real Estate Have in Common?

Let’s start with the answer to the question in the title and then work backwards.

“Both have prices that are supported by artificially low interest rates.”

First, take a look at the price of Apple shares. Below is a chart of Apple stock for the past five years.

The shares were trading around $100 at the beginning of the chart, and now the shares are trading at a value north of $300.

Let me ask you a question: How much growth has the sales and profit of Apple seen in the past five years to justify such price appreciation?

The stock is up 200%, have earnings gone up 200%? Or maybe just 100%? Hmmm?

Let’s look at the sales or revenue amounts:

Only 10.4% sales growth in TOTAL over five years, and 2019 is actually lower than 2018.

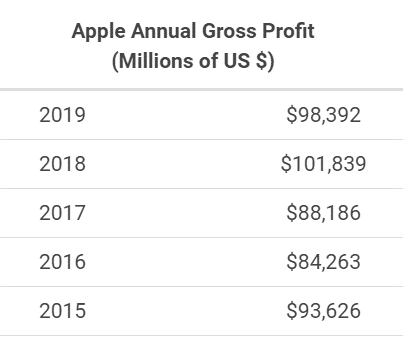

Next let’s look at profit:

Ok…4.8% total profit growth.

But the stock is 200% higher…wait, what?

I must admit, I am being a little misleading. You see, Apple has bought back $317,000,000,000 worth of their shares since 2015.

Therefore, let’s look at PER SHARE earnings.

At least, when you include share buybacks you end up with per share profits increasing a total of 22.5%, but does that still justify a 200% price increase?

Hold that thought…

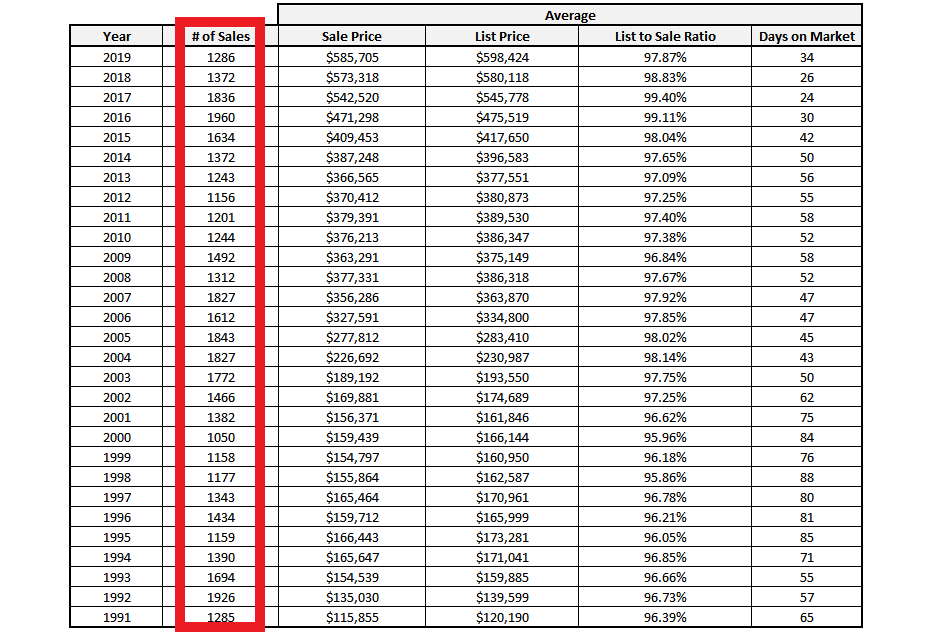

The next set of data is a look at Nanaimo single family real estate pricing.

The following chart is shown with permission from the newsletter of Dan Morris, a realtor with Royal LePage Nanaimo Realty in Nanaimo.

This is a fantastic data set and is similar in theme across many Canadian real estate markets.

Looking at the sales price column, note how 2019 ended at an all-time high for Nanaimo.

At the same time, notice as home prices accelerate higher two other things typically happen:

- Days on Market tend to get lower

- The number of sales tends to go higher.

As home prices go “flat,” the opposite of the above two points tends to be true.

So now check out the number of sales for 2017, 2018 and 2019.

Wow, that is a huge deceleration in the number of sales. Actually, if you look at 2019, you can see the number of sales drops back to levels seen in the late 1990s when Nanaimo was a much smaller town with fewer homes in total.

But the average price just kept going higher, even though the number of sales dropped dramatically!

How does this happen?

From a supply/demand perspective it simply means that, yes, there are fewer “buyers” in the market place. But at the same time, there are fewer “sellers” as well.

What does that mean?

It can mean a few things, but what jumps out at me is how the low interest rates keep supporting the high prices by:

- Keeping potential buyers at the highest possible “amounts they are able to borrow” relative to their maximum payment structure and,

- Allowing people to refinance at lower interest rates and stay in homes that are already forcing them to borrow money every month to balance their budgets.

Now let’s tie these two stories together.

What becomes clear is that both of the extremely high prices for Apple shares and homes in Nanaimo are supported by the artificially low interest rates.

Since interest rates have been low for nearly 11 years now, the world has come to see these borrowing levels as permanent.

If interest rates were 6% and mortgage payments were 50% higher on the same amount of mortgage, home prices would be nowhere near $600,000 in the Nanaimo market.

If Apple had to borrow money at 6% to fund their share buybacks they would not want to be paying $320 for their shares. Investors would not want the shares at that price either; they would likely by a 5% risk free bond investment rather than precariously overvalued stocks.

Therefore, the concern becomes an overly indebted world where assets have gone up to extreme valuations and finally stop going higher.

Summary:

The unintended consequences from many years of accumulating more and more debt, enabled by artificially suppressed interest rates, are slowly but surely piling up.

Does that mean I believe the world has reached its debt limit? No, not really.

I don’t think there is a debt limit…as long as the financial world remains confident and takes on more debt.

But what if something shakes that confidence? What if conventional wisdom comes to believe there is too much debt?

Then, all of that “manageable debt” becomes unmanageable.

The world is not there yet, but the stories of Apple stock and homes in Nanaimo both tell us that:

- Prices are stretched to the upside.

- The amount of buyers at the present prices are shrinking.

The old expression that “volume direction precedes price direction,” doesn’t always apply immediately, but usually applies at some point in time.

We remain vigilant and dynamic in our asset mix derivation process AND cognizant of the changing investment themes.

As always, please reach out with any questions, comments or concerns you may have, and have a great week.

Also, if you haven't had a chance to already, Megan wants you to hop on over to our Upcoming Events page to see what seminars we have in store and to RSVP as seats are limited and are quickly filling up.