New Highs in Stocks…

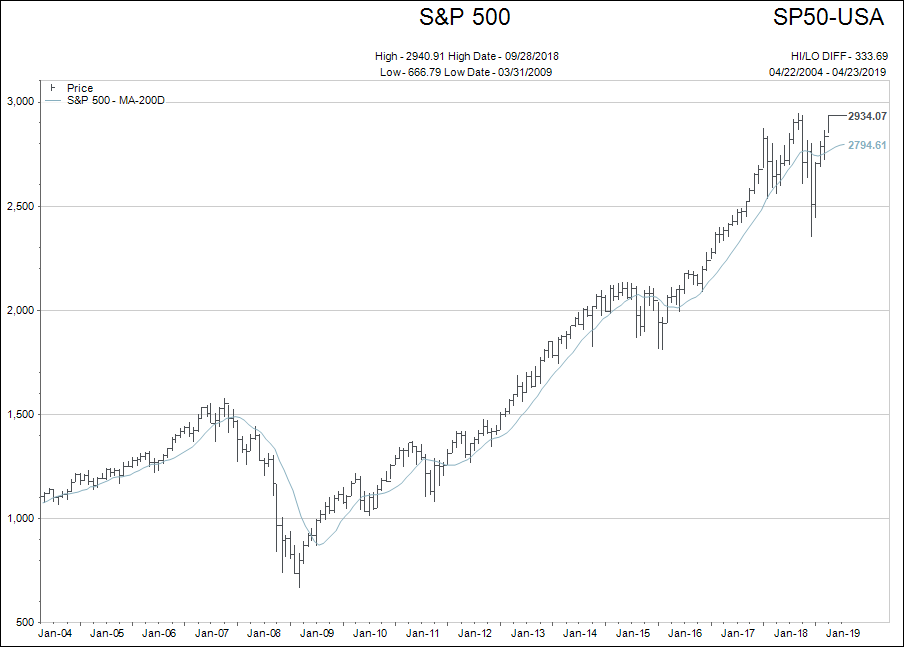

The S&P500 stock market has made a new high in price.

The round trip from January 2018 to April 23rd 2019, is complete.

When the first market correction took hold in January 2018, I really believed the end of the Quantitative Easing “BULL Market” ignited in March of 2009, had finally arrived.

The summer 2018 rally higher looked to me like a “head fake.” The US Federal Reserve, Peoples Bank of China, and the European Central Bank were either raising interest rates and withdrawing liquidity or “on hold.” So I was pretty sure it wouldn’t last…

…And the rally didn’t last.

As stated many times this year though, that all changed in January 2019!

The central banks of the world decided they needed to band together and keep “giving us this medicine that keeps us sick.”

How? By going back to their “easy money” habits and thereby:

- Anchoring deflationary expectations.

- Crushing corporate risk taking and encouraging financialization.

- Spurring greater wealth inequality.

Below, I will make three comments speaking to what we are witnessing.

Each category makes me feel a little different.

From the “Market” perspective:

New highs are new highs.

There is no way to make that story a negative. There is also no way to tell how much higher stock prices will go. Go with the flow…

BULLISH is as BULLISH does…to rephrase that great pop-culture philosopher, Forrest Gump.

All kidding aside, it is fine to stay invested, add stocks thoughtfully on small pull backs, and be disciplined with stop losses.

At the same time, it is key to remember that nobody really knows if the US central bank will pivot back to a less accommodative position again.

Now that stock markets have recovered, if central banks start uttering statements like “inflation is gaining momentum,” or “we might not end Quantitative Tightening in September….” Well, things could get interesting.

It remains important to keep our focus on the global monetary conditions too.

Since writing the sentences above, the Chinese politburo made comments about Chinese monetary conditions not being loosened any further, and their market fell 3.2% in four days.

It is safe to say, financial markets are at a place they have never been before in history.

Oh, markets have gone up sharply in the past, but not with interest rates this low AND with central bank expectations to LOWER rates further, rather than raise them, even though stocks are sitting at all-time highs.

These are definitely not the stock market conditions of pre-2008. They are not even the markets of pre-2018! The financial world changed in January 2019.

From a “Human” perspective:

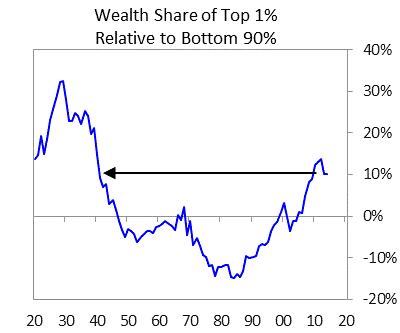

The run up in financial assets since 2009, has created a wider and wider gap between the “haves” and the “have-nots.”

The idea behind the process of raising interest rates SLOWLY in 2017 – 2018 was to try to “normalize” the financial world again. Interpreted, to “normalize” was meant to stop the process of wealth and income disparity and ease the rapid spread of the “financialization”* of stock markets.

Friends, the goal of normalization is OVER.

Therefore, it could be expected that problems of wealth/income disparity, pension fund underfunding, yield curve flattening, and financialization will grow in magnitude.

From the human life perspective, that will be good for you if you are “financially established” and not so good for you if you are “young, poor, middle class, or on a fixed income.”

The trends in the two charts above do NOT make for a planet full of happy campers (I don’t think many would dispute this fact).

With the growing number of “unhappy campers,” expect to see Modern Monetary Theory (MMT) take center stage in both the media and in politics.

Ideas like free tuition, paying off student debt, free healthcare in the US, even mailing out cash cheques to citizens, will be debated.

Please don’t miss the logic behind why these “freebees” are going to be floated by politicians. When you are boiling the frog in water, you want the frog to be as comfortable as possible for as long as possible.

The raising of interest rates and slowing down of printing money in 2017 – 2018 was an attempt to try and equalize the “human” aspects of the financial markets again. That process is over for now and, by ending it, inequality is once again allowed to flourish.

From the “Psychological” perspective:

I believe this is the first time I have brought up the idea of a psychological aspect to what has happened in 2019. This is my opinion, but it struck me over the Easter weekend as I was doing some research for another project I am working on.

Whether you are BULLISH or BEARISH on financial markets, people tend to agree that the age old fundamentals that once offered a “road map” to making investment decisions are not as simple to read or act upon as in the past.

One article I read stated that “the more sophisticated of investor you were at the present time, the more likely you were to be BEARISH on stock prices.”

Why?

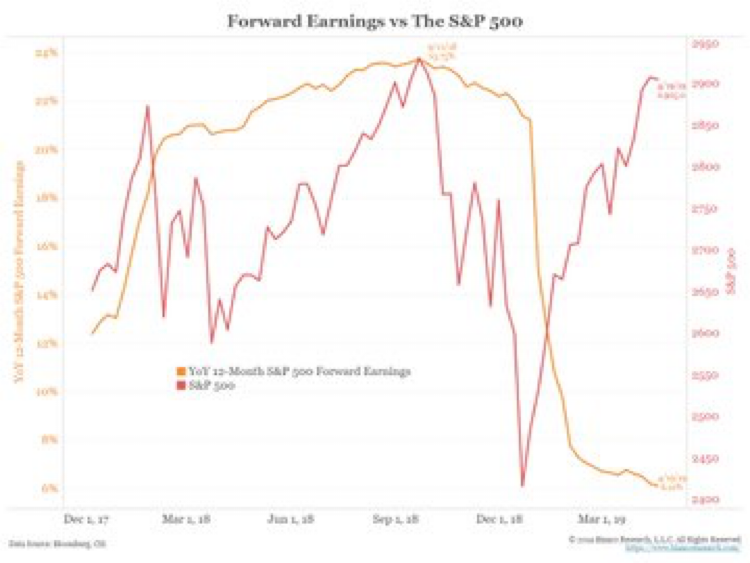

Because, both technically and fundamentally, stock markets have rallied beyond the usual standard deviations without any real correction, AS WELL AS against the general trend of global earnings and the economy.

It is hard not to act on your psychological impressions. We trust them to keep us alive in everyday life. They are a huge part of who we are…

So what happens?

It appears that investors have become paralyzed in making decisions. The usual “buy and hold crowd” are even leery about adding new money to investment strategies right now.

Hey, this is showing up in the real estate markets too.

Interest rates have dropped substantially, real estate prices are off a little bit, and there are a few more places to choose from. But sales volumes remain low. It will be interesting to see if volumes pick up in coming months.

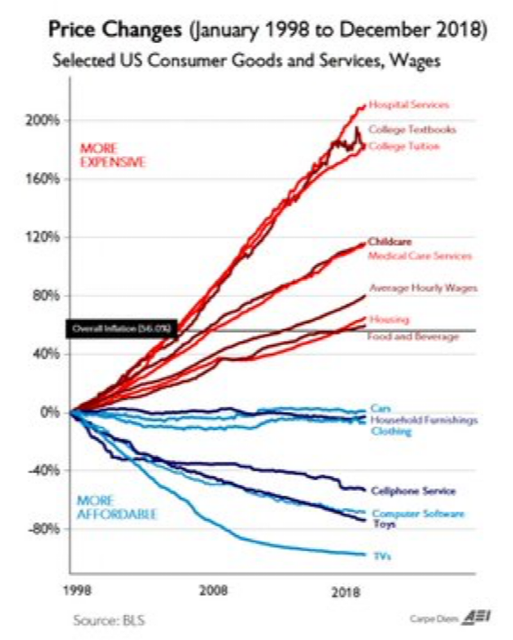

Let me add one more chart to drive home the paragraph above.

If you remember back to the earlier chart above that broke the income gains into the top 40% and the bottom 60%, and recall how the top 40% has made the vast majority of income gains since 1970, you will get a lot more out of the graphic above.

The “average hourly wages” trend line in the graphic above includes EVERYBODY.

If you just graphed the bottom 60% of wage earners the trend line would fall between “clothing and cellphone services.”

So, to summarize the chart above for the bottom 60% of wage earners:

They were fine as long as the bought cell phones, toys, software and televisions. But, God forbid, if they wanted to eat food, live somewhere, go to university, buy gasoline, or take care of their kids.

At the beginning of the editorial I stated I felt different about each category viewed in the comment body, so let me clarify.

The market perspective never really bothers me. Markets do lots of weird and wonderful things, and in 31 years of working in this industry, I have learned to “roll with the punches” so to speak.

The human perspective is a burden to me. Historical eras of income and wage inequalities resulting in financial repression have never ended well. The policies that cause inequalities end up benefiting a smaller percentage of the population as time goes by. In the end, the poor and middle class end up pushing back at the elites.

It saddens me to see the growing number of families negatively impacted by the choices of our political and financial leaders.

The psychological perspective is more difficult to explain as a feeling. The best analogy I can offer is the feeling a sports team has when they have played as hard as they can by the rules and then, all of a sudden, the referee makes a game changing mistake on a call.** As a player, you just feel like all that work and effort wasn’t rewarded and the end result was not justified.

As an investor, that’s how I feel when I look at so many of the indicators that usually led to certain market results don’t elicit those same results anymore.

The psychological impact of the abrupt shifts in the central bank policies when measured against their earlier spoken intentions are also frustrating.

I speak to, and read blogs of, professional investors who have been in the investing business for decades who feel the same way.

All you can do is get over it.

But, deep down, you do wonder about the value of your hard work and years of experience.

For what it is worth, I really do believe there is a bigger story playing out before our eyes.

Human history has seen many examples of where classes of people are exploited by other classes of people. I guess I hoped we had learned a little more from this history about what happens to EVERYBODY when the world becomes too unbalanced…guess that hasn’t happen.

Give me a call any time, or shoot me an email with your questions and comments. Also, check out Megan's post about notable items! It's the end of tax season, and we've got a lot of exciting and informative events in the next couple months that you are not going to want to miss.

-------------

*Financialization – Using adjusted earnings (rather than GAAP) and share buybacks to make companies appear cheaper than they traditionally would have.

**Think of the Kansas City Chiefs in the Championship Weekend game against the New England Patriots where questionable “roughing the passer” and blatant “pass interference” calls went against them and cost them the game.