Executive Summary:

- “Great Mistake” – Central banks let Quantitative Easing (QE) run for more than a year back in 2010.

- Ten Years Later – The slow pace of raising interest rates continued. Central banks never took back the “great mistake” for fear of stalling asset price increases, but in the final quarter of 2018 stocks declined anyway; real estate stalled too.

- “The Panic of 2019” – No it wasn’t investors that panicked…it was the central banks! The Bank of Japan, European Central Bank, and US Federal Reserve all pivoted from tightening monetary conditions back to loosening them.

- “Great Mistake II” – Panicked central banks offering an outlook saying they will not raise interest rates for the rest of 2019 and project only one rate hike in 2020. Also central bankers stay open to a new set of interest rate cuts if stock prices decline again. What happens if inflation comes back, especially “bad” inflation? How will stock markets respond to an interest rate increase?

Rational:

What an incredible difference in market conditions the world has witnessed over seven months? After a three month 20% drop in the last quarter of 2018, stock markets have recovered to near all-time highs.

Do you really believe economic conditions changed that quickly?

Me neither.

What changed quickly was the price of the stock market.

One more rhetorical question: Is the central bank’s mandate to guide and influence the stock market or the economy? Hmmm?

At the end of the day, the belief in “The Narrative” is what keeps me fascinated in my work.

What is “The Narrative?”

Well, not to be sarcastic, but just put on CNBC or BNN for about an hour and you will get a pretty good idea of the basic investment narrative.

If you don’t have an hour I will summarize it for you:

Buy stocks even if earnings are weakening, debt levels are high, economic data is slowing, and valuations are at the third highest ever level in history BECAUSE the central banks have your back.

We do live in interesting times! For old timers like me, it makes one feel out of touch with the fundamentals of investing learned over your career.

Truth is…we all have to play the hand we are dealt. This includes you…

The body of this review is going to move through the past seven months and end with a lookout into August 2019.

September 2018:

Stock markets enter the final trimester of the year on a high note. Interest rate yields continue to flatten across the yield curve at slightly higher levels.

Other than being technically “overbought,” there is no immediate reason to expect financial markets to change direction at present, but this should not be taken as a reason to be complacent.

My investment thesis remains the same as it has been all year:

- Financial markets will continue to ride a wave of liquidity higher until the liquidity dries up.

- The central banks around the world are in the process of switching from Quantitative Easing (QE) to Quantitative Tightening (QT). This change in the liquidity tide, coupled with SLOWLY rising interest rates, will stop the longest BULL market in history and asset prices (real estate and stocks) will fall.

- The central banks will panic when assets fall (maybe 15% - 20%) and return to a QE bias in the global monetary policy. The change from QT back to QE will create another leg higher in asset prices.

- Our goal is to be fully invested in the stock market AFTER a 15% - 20% decline in asset prices takes place AND the US Federal Reserve panics back to QE. This narrative gives our model a clearly defined technical picture to enter and exit investment positions assuming the scenario above.

Please remember, the timing of all of this remains unclear. My goal is to stay patient and let the central banks act, even though it is a painfully slow process; they realize they are taking the patient off 10 years of life support.

Reflecting on those words written in September of last year, I must admit, they ring pretty true today!

The central banks put on a brave face and slowly raised interest rates while reducing “liquidity” via Quantitative Tightening right into a 20% decline that bottomed on December 24th, 2018.

Within the next two weeks, the Bank of Japan, European Central Bank, and the US Federal Reserve all stated plans to stop raising interest rates and pause QT….full stop.

Well, not exactly full stop. Each central bank wanted to appear like it was still “vigilantly trying to take back 10 years’ worth of stimulus” but, in the end, they all caved in completely and went back to their old bag of tricks.

…and investors, like Pavlovian dogs, went right back to their old habit of throwing caution to the wind and buying stocks.

January 6th, 2019 – March 31st, 2019

Just in case you missed it, check out the two year chart below of the S&P 500 index.

There are two things I find interesting about this chart and I would like to take some time explaining them to you.

- The sheer violence of the rally in the S&P 500 from early January until the present.

Rapid moves higher after stock market corrections are not typically made with such conviction. Usually, the market will rally, then fall back and “retest” the lows, and then regain confidence and rally again.

Not this time.

Stocks rallied right from the “basement” and never looked back.

Clearly, “someone” knew the central banks were caving in for real. Remember, it was not until mid-February that central bank officials ACTUALLY stated that they had reversed policy…it was mid-March when the plan was actually laid out formally. It appears that many knew what was coming.

- The steep rally still has not made a new all-time high price.

The expectation is that a new high is only days or weeks away. Until then, mild respect should still be paid to the BEAR market rally case.

One reason the BEAR case still needs respect. The global purchasing managers index (PMI).

That chart still has a very weak tone. It represents the cumulative index reading for the entire planet.

Shown in a more directionally sensitive form on a shorter time frame.

If the real economy keeps slowly weakening, stock prices will prove to be too expensive to hold at present levels.

This is where I like to remind people that the stock market does not represent the economy. Just because stocks have recovered, it does not mean the economy has recovered.

The opposite is also true; just because the stock market goes down, it does not mean that the economy has equally weakened (it was never that bad).

This brings me to the “Great Mistake II” I believe the central banks around the world have made.

In the first paragraph of this report I asked the question: “Do you really believe economic conditions changed that quickly?”

I doubt the economy was weakening so quickly that the global central banks had to panic back to negative interest rates and printing money.

Therefore, the key to looking forward into the coming four months is to see how the central banks walk the line in their rhetoric as we get better economic numbers at the same time they are promising to leave interest rates the same for almost another two years!

April 2019 – July 31 2019

Let’s focus on two themes looking forward for the next four months.

- Inflation is growing, but it is not the “good” inflation where asset prices steadily rise. It is more like the “bad” inflation where “wages and non-discretionary items” (food, gas, etc.) rise in price.

- The central banks have painted themselves into a corner in terms of interest rate policy. Therefore, they are unlikely to respond by raising interests much if bad inflation continues to trend higher.

When we add our two themes together the net result leaves the middle class and the poor in vulnerable positions.

The reason for this vulnerability is inflation in basic living requirements impacts those on fixed incomes who also have limited savings far more than the wealthy.

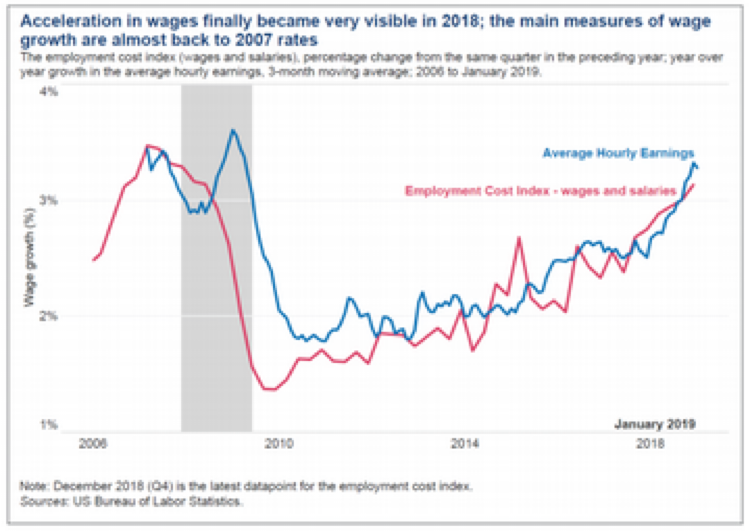

The chart below represents the situation with wage inflation at the present time. Wage inflation is welcome news for the middle class and the poor.

But the wage acceleration appears to have come far too late in the “post Great Mistake” economic cycle (Ray Dalio, Bridgewater).

Just think in terms of food, gas, and living expenses…how does the red line in the chart above keep up to the pricing of these items?

We need to remember why these types of expenses are so important to contain.

If you pay an extra $40.00 per month for gas, $60.00 per month for food, and 3% per year for rent or keeping your home up and running you are simply paying more money for zero increase in lifestyle return! If you never experienced an offsetting raise in income in the year your household is now further behind in economic terms.

Those lifestyle cost increases are cumulative, and it is rare for the prices to go lower again. Therefore, when basic living costs rise faster than income people have less discretionary money to spend in their budget.

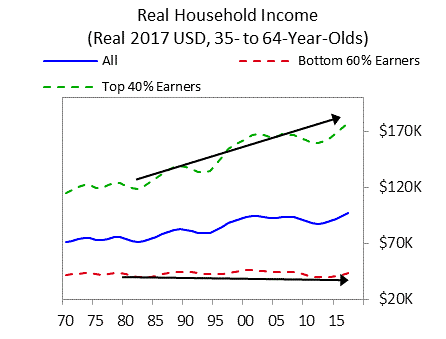

The past 20 years has seen a crazy surge in consumer debt levels. Individuals have borrowed at low interest rates to maintain their lifestyles as wages lagged behind cost of living increases.

Now that wages are rising it will help people keep up BUT it also fuels more “bad” inflation!

Many times, this cycle is exactly what causes central banks to raise interest rates!

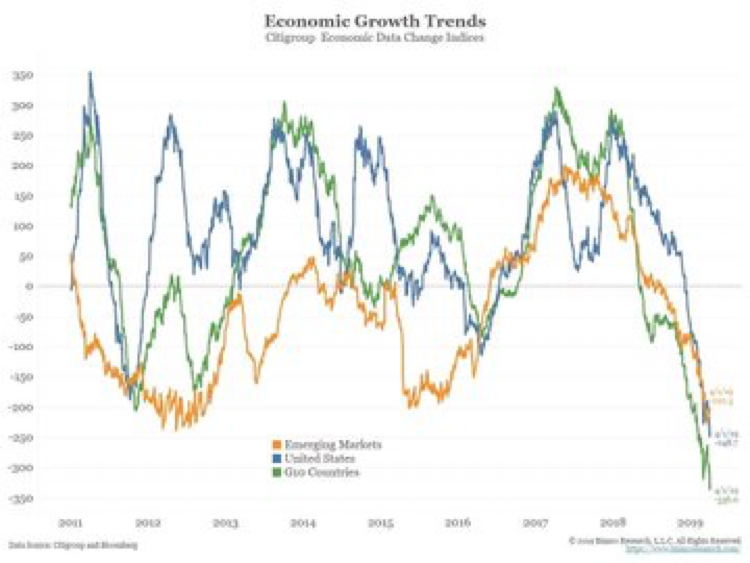

Let’s look at the data (not including the Q4 2018 stock market decline) that caused the central banks to cave in to their plan to raise interest rates.

Global growth continues to slow.

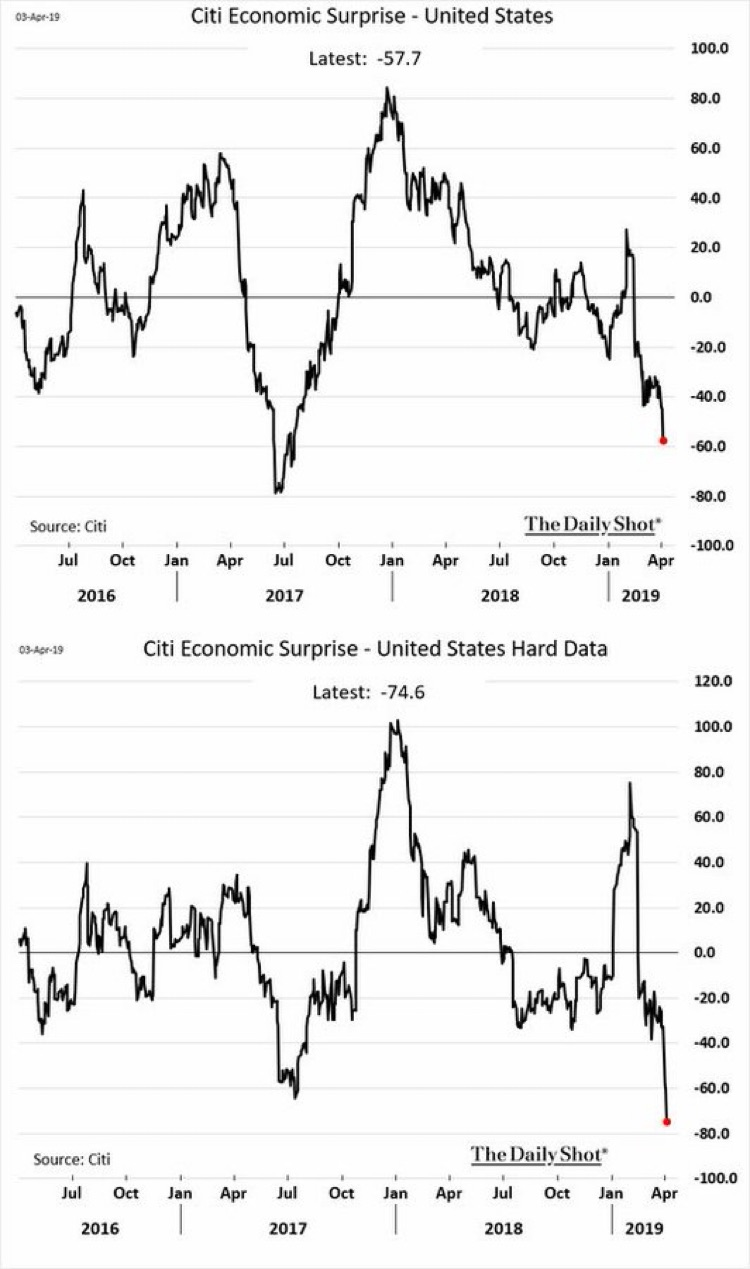

American “economic surprises,” which means numbers that exceed or miss expectations, have been weak.

Now you can see how the central banks have painted themselves into a corner.

The central banks have put all their verbal policy commitment behind the weak economic charts, and ignored the “bad” inflation data in their promise to cut interest rates and end Quantitative Tightening.

If the economic data even modestly improves, which is what I would expect, and the bad inflation continues to ramp higher, the central banks are going to be faced with a serious dilemma. Stay tuned…

What does this mean for investors?

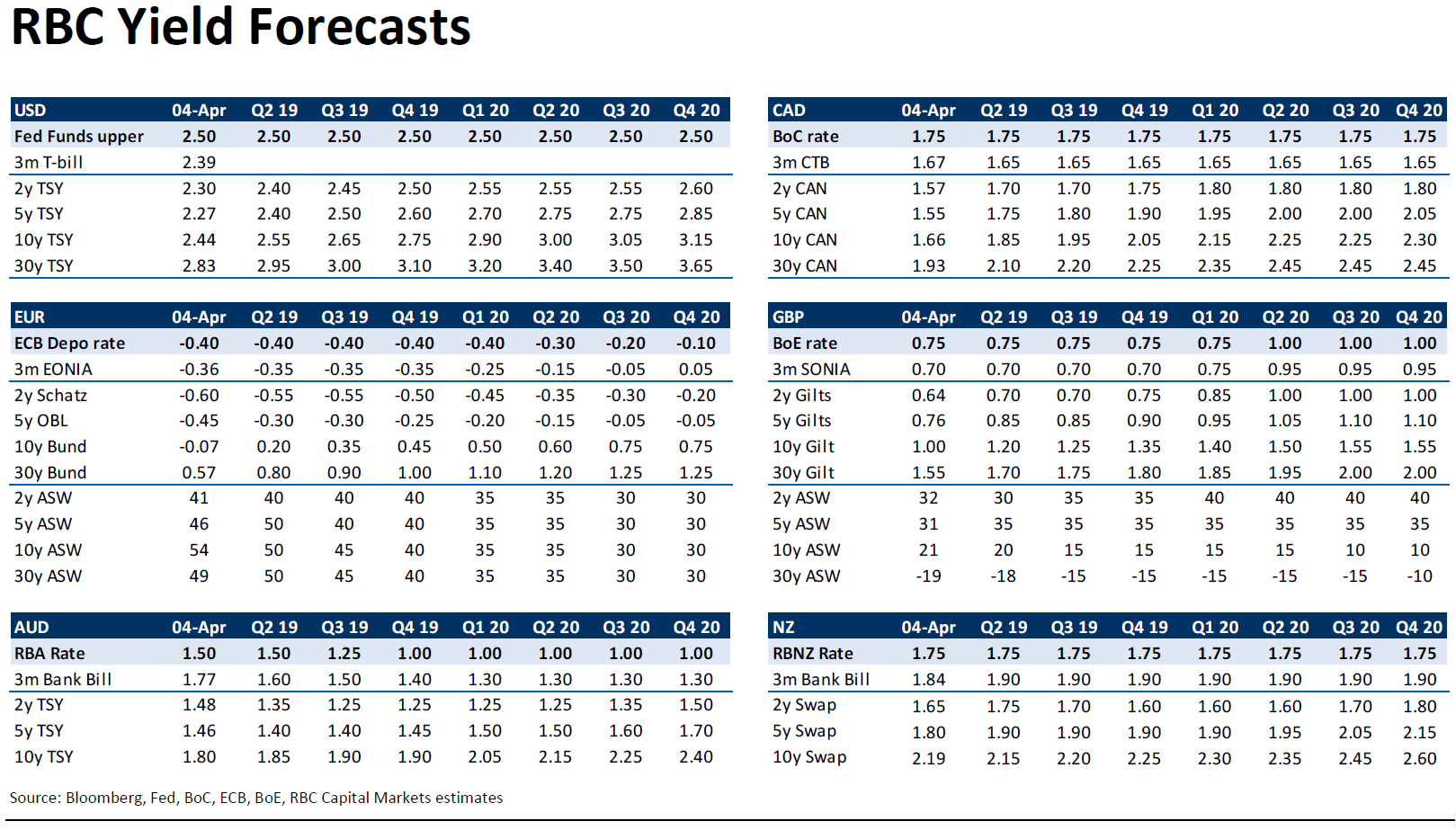

Let’s start at the RBC Yield Forecast from April 4th 2019.

Those rate projections are benign relative to only three months earlier.

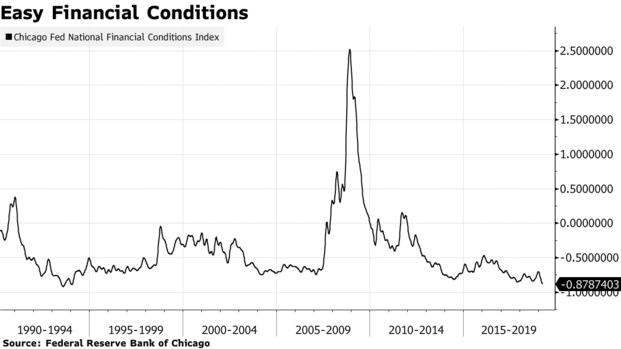

I find myself taking “the under” on these interest rate projections even though economic financial conditions are the “easiest” in history. In this context, easy equates to availability of money to borrow at low interest rates.

By taking “the under” and expecting even lower interest rates than those forecast, it brings me back to the themes published in my “Client Only” publication from last week.

The theme of that publications is “stocks are OK for now but there are a number of other investments that are cheap and look interesting IF the stock market falters and the economy remains sluggish”. If you are a client and did not receive it, email me and I will provide you with the password to our new “For Clients” page on the website.

Summary for April 2019 – August 2019

Even though stock markets have done a “round trip” of 20% down and then up since September 2018 leaving them basically unchanged in value, the macro economic outlook is in a completely different place than it was last summer.

- The charts in the body of this report allude to how significant the slowdown in global growth has been.

- Central banks have pivoted 180 degrees into “interest rate cutting” mode from “interest rate hiking” mode.

- Stock markets are priced against the trend of both earnings and economic growth as of April 2019.

- Stock markets are now back aligned with the “don’t fight the Fed” mantra of owning stocks when central banks are easing financial conditions.

The BULLISH commentary also states that the global slowdown is “transient” in nature and due to pick up in the second half of 2019.

Fair enough, that is entirely possible.

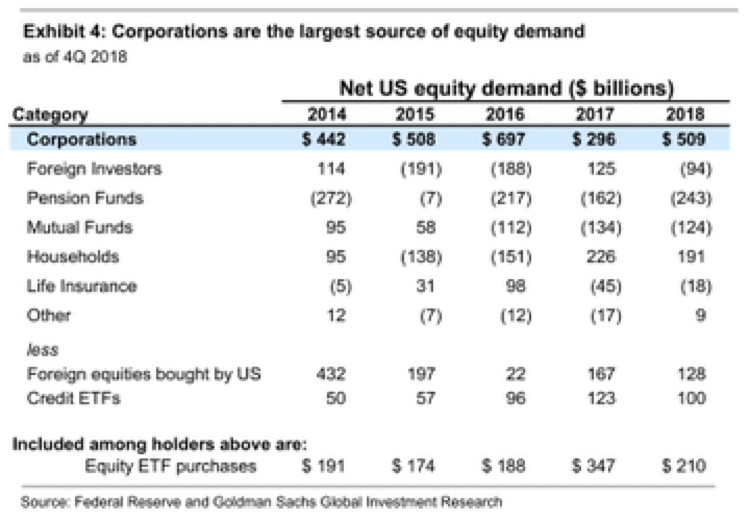

The key for investors to realize is that a huge part of the rally in stock markets is NOT based only upon the narrative of a “second half pickup in economic activity.” It is based on the same old narrative of the central banks will save the day again with liquidity and low interest rates and corporate share buybacks. Note: the “corporations” line in the graphic below…wow, that is a lot of NET purchases.

Dear reader, I am not saying the BULLISH outcome is not going to happen. As a matter of fact, it probably is the case!

We all, however, should be cognizant of other more historically consistent outcomes that may take place. Financial markets might actually figure out that the real problems for the economy ARE the actions of the central banks and that “water does keep the boat afloat but can also sink it.”

Stay tuned…