“A China Deal”

Each day it seems the stock market futures are higher and the media cites the progress on the China trade deal as the reason for the market optimism.

President Trump states “talks are going well,” but the “sticking points” are still…well, sticking points.

Nick opinion: A trade deal between the US and China is going to happen and the stock market is aware of that fact. Neither side however, is going to get close to their objective demands.

Once the deal is on paper I believe it will be viewed as “net-neutral” for the stock market.

Therefore, the topic of this weekly comment is looking past the successful signing of a US/China trade deal and what investors might expect to become media's new focus of attention.

The first thing investors will refocus on is the global economy.

Let’s look at a few charts showing a variety of profiles of the global economy.

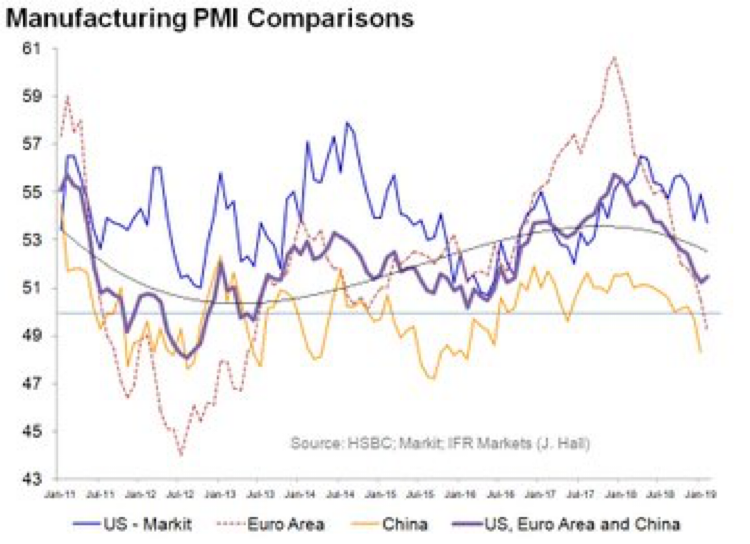

First up, the global purchasing managers indexes (PMI). Please note a reading below 50 signals “recession.”

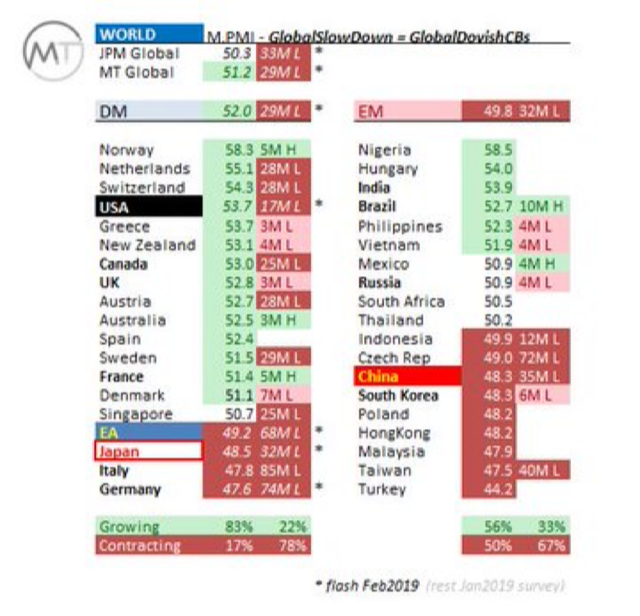

Both China and the Eurozone are reading below 50. The purple line with all of the PMIs blended is still above 50. Below are the specific country readings.

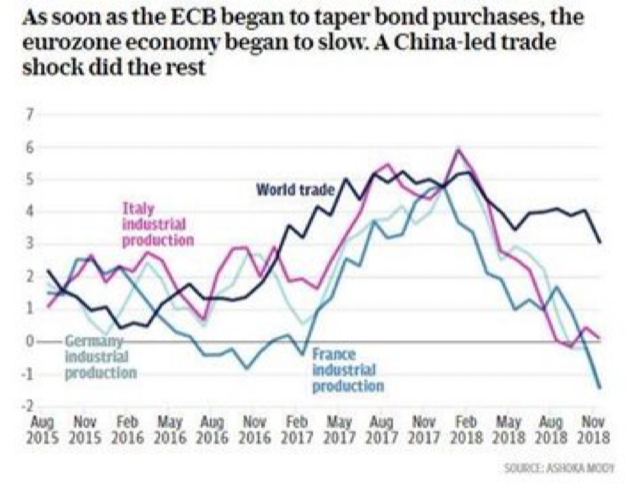

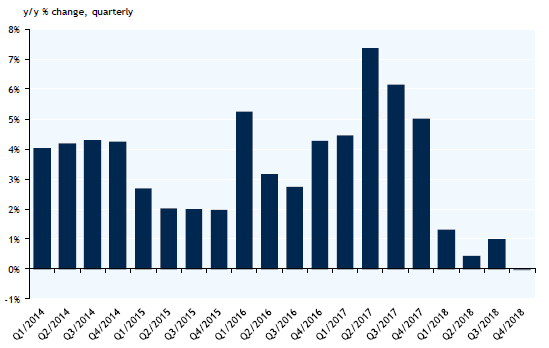

World trade statistics is dependent upon growth rates. Notice how trade (black line) has slowed as global PMIs have weakened.

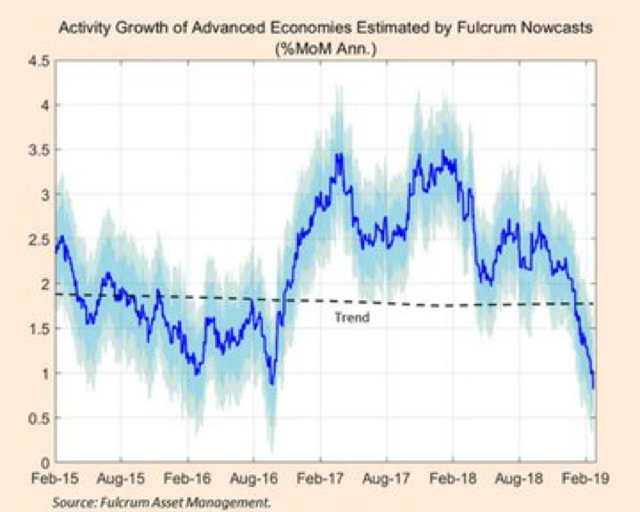

The next chart shows the broadest measure of global growth measured in advance economies.

Economic “surprises” continue to trend lower in the US which is the driver of global growth at present.

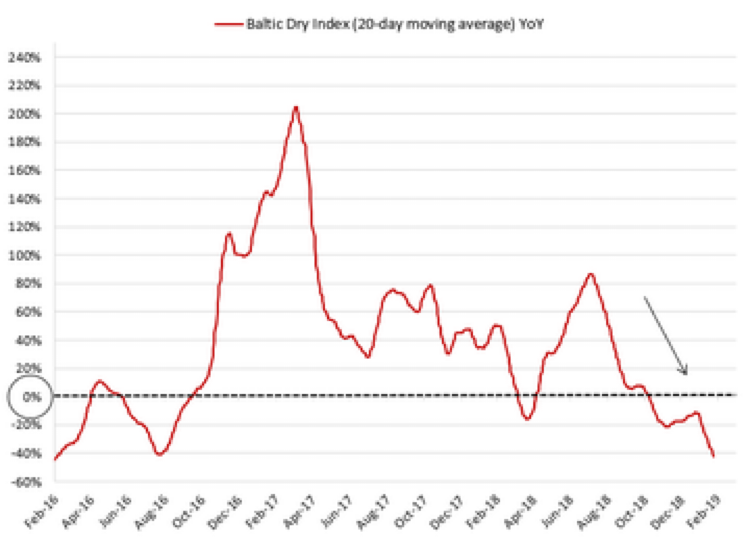

Cost to ship dry goods continues to push lower as well.

And finally, one Canadian chart. The RBC chart below is the graphic representation of how fast retail sales have dropped in our country.

Bottom line: The surging stock market is going to have to reconcile all of the above weak economic data at some point. This is why we need to be careful not to grow complacent in our discipline.

Maybe the global economy stopped weakening in February? Maybe the stock market is anticipating a global economic rebound because of the global central bank intervention?

Would this justify the rapid rise in stock markets?

Maybe…but not necessarily.

Because good economic news will start the new worries about inflation and, at some point, bring the “Fed is going to have to raise interest rates” narrative into play again.

By turning 180 degrees from a tightening bias to an easing bias, global central banks are limited their ability to shift policy again. What if they start talking about raising interest rates again? How much credibility will they have?

We are months away from this story, but it could happen upon us faster than we think.

If the further acceptance of the Modern Monetary Theory (MMT) continues to grow rapidly, then stock investors may start to fear an overheating economy coming quicker than usual.

The greatest pushback by the economists who disagree with MMT is that it could be very inflationary and force central banks to raise interest rates much faster than in the past cycle.

Speaking of MMT, I noticed the following quote on Twitter last week.

“The kids in the DiFi video rightfully don’t give a s#*t about PAYGO or 60-vote thresholds in the Senate. They just want to confront climate change. If you are running for President this year you better see the world through the kids' eyes, not DiFi's.”

– Brian Fallon, ex-lead singer of Gaslight Anthem

That quote perfectly sets up what I believe we are going to see as the battle lines in the 2020 US Presidential election.

We do live in interesting times…

The Buffett Factor

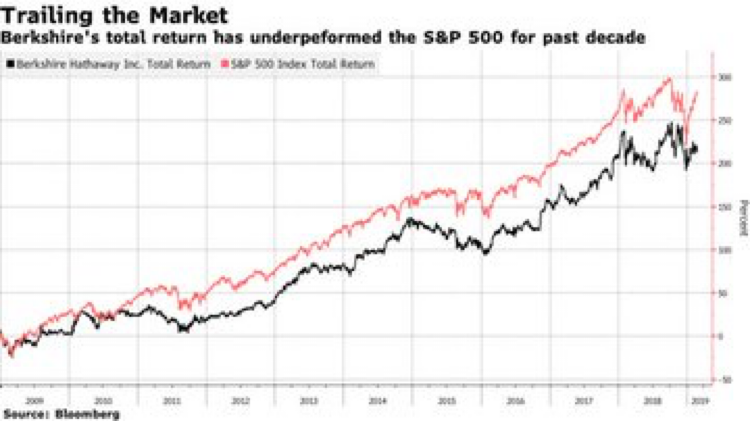

For all those who feel like the stock market indexes in the US have outpaced your personal performance…well, you have good company.

Below is a chart of Warren Buffett’s Berkshire Hathaway 10 year performance vs. the S&P500.

Berkshire has underperformed the S&P500 for almost the entire time that Quantitative Easing and central bank policy have ruled the markets.

Who would have guessed?

OK…one last point of interest.

Let’s look at Gold vs. the S&P500. It is a little blurry, but you will see the trend.

Gold has outperformed the S&P500 since the turn of the Millennium. Gold is up 361% and the S&P500 is up 221%.

Not what you hear in the mainstream news, eh?

Have a great week, and feel free to reach out with any comments or questions you may have. We're always happy to hear your thoughts and feedback.