Is the Cooling Rate for the Global Economy Getting Faster?

Observation 1:

Would you agree that US Federal Reserve President, Jerome Powell, has the best poker face of any Federal Reserve President since Paul Volcker held the position in the late 1970s?

Up until Wednesday evening last week, Chairman Powell has stayed the course and stated the Fed’s intentions to keep raising interest rates at a constant pace; even as American stock and real estate markets began to waiver and the whining started from the usual suspects, Powell never changed his tune.

At a November 14th, speaking engagement, he softened his rhetoric and made the basic point that the Fed has to be careful.

What made him change his tone?

Observation 2:

CNBC’s “Mad Money” host, Jim Cramer, stated last week that in conversations with numerous company CEOs the story has been the same: The US economy has slowed rapidly in the past 60 days. I realize some of this type of rhetoric is to try and influence the US Fed to stop raising interest rates, but I do believe there is some basis to the comments.

Observation 3:

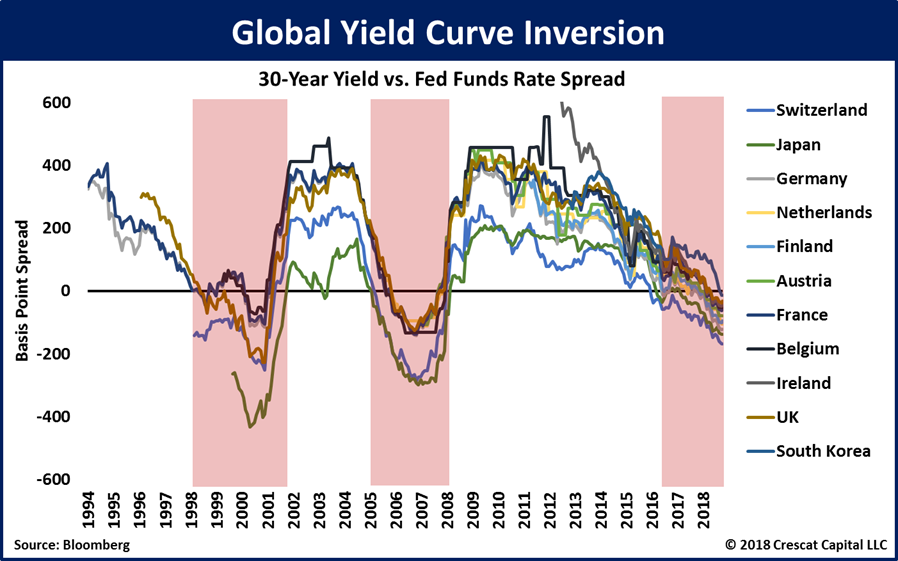

Global bond markets are sending a message too. The chart below shows global bond markets moving towards “inversion.” Meaning that short term interest rates are higher than longer term interest rates, and could indicate an oncoming recession.

Those are very long term trends shown on the chart, however, and we should not read anything “immediate” into the picture…just that a global yield curve flattening is happening.

Let me make some forward looking statements. These are purely ideas I have been thinking about in the context of 30 years experience in the industry. The current unique economic conditions present do create problems for applying the past to the future, but it is the best template we have to go on. The combination of experience and rigorous investment discipline is our best road map to markets.

If inflationary pressures are growing (wages, raw material costs, transportation costs, etc.) and economic activity is cooling, what happens to corporate profit margins in the next six months?

Stagflation.

One would have to imagine a sharp decline in profit margins that bottoms relatively quickly. The real question is what happens if the stock market “narrative” changes to something closer to a “stagflation” outcome including quickly declining profits? The risk of this happening is growing.

What if the US Federal panics and starts Quantitative Easing again?

Ah…back to my theme for the last 18 months.

My original thoughts on this outcome were that stocks go roaring back to new highs as the final leg of this BULL market is played out, but a “rapidly slowing US economy narrative” would temper my enthusiasm for this roaring BULL market outcome.

The initial response would still be BULLISH for stocks, but it might fade faster than I would have thought in my original outlook.

It would also make me VERY positive on precious metals and 8 – 10 year Government of Canada bonds.

Conclusion

Since the October stock market lows, I have taken the position that stock prices would work their way higher until Christmas time. Until the lows are broken, I am sticking with that forecast.

Canada has held up better, but some of my US charts are getting “dirty” to the downside, where dirty refers to moves that do not support the technical profile I am looking for.

The majority of the TEAM models that are in structured note format are already in cash as of October 1st; the others are only 50% in the stock market. I really don’t mind either profile given what I have been discussing above.

The FAST TEAM is invested still 100% invested.

It was in cash since early September and bought the Canadian dividend index with a 5.57% yield at a price of $19.71.

The price of this index has been holding above $20.00.

The FAST TEAM has a stop loss placed at $19.75 to force it to exit the market “flat” if the BULL market falters.