More about US Debt Dispersion

Right off the top, thank you for all the comments and questions about the “Monetary Hotel California” weekly.

The idea of how the government has gone so much deeper into debt as compared to the US citizenry was a surprise to many, as popular opinion was that both were deeper in debt.

The www.usdebtclock.org site has a lot of great data and the ability to go backward and forward in time. It is worth a few minutes of your time to check it out for yourself.

The key theme that came back from readers is the question of how is it possible for the US to continue to run an operating deficit indefinitely into the future?

The simple answer to keep the money printing presses running has two requirements:

- The US asset base must keep inflating in value.

- The US dollar must remain the “reserve currency” of the world.

As the budgets become more unbalanced the process by which the US is allowed to keep creating money becomes more stressed.

Higher inflation rates tend towards higher interest rates. Higher interest rates predicates more interest payments on new and rolling over amounts of debt issuance.

The chart below shows the expected path of annual interest payments on the US Federal debt over the next 10 years.

It is important to remember, this is just the interest on debt, not the total budget deficit. Add the possibility of a recession before 2022 and we quickly see something needs to change in terms of US spending and taxation.

Summary Statement: Interest rates are the key to EVERYTHING financial in the world today. For decades, interest rates have trended ever-lower. Lower interest rates have covered over a multitude of mistakes made by investors and governments.

During the past 10 years, interest rates have been manipulated lower and kept low. It has resulted in a world where we have been rewarded for:

- Investing in ridiculous securities

- Voting for ridiculous candidates

- Borrowing ridiculous sums

To those who decided over the past 40 years that “deficits don’t matter” I would like to amend that statement to “deficits don’t matter until interest rates go up to a level where they do matter.”

Because saying deficits don’t matter is “ridiculous.”

Interest Rates in Canada and the US

Let’s take a look at where interest rates are for both short term and longer term bonds in the Canada and the US.

Canada:

It is expected that the Bank of Canada will raise their bank rate on the 24th of October. They all but said they were going to raise in September except they wanted to wait for NAFTA to be decided.

NAFTA is done and this clears the runway for a 0.25% hike this month.

Below is the yield on the 10 year Government of Canada bond.

The 2.53% interest rate shown is now at a cycle high.

The economic case for raising interest rates further in Canada is not as strong as it is for the US. Going forward from here I would expect Canada to raise interest rates at only half the pace as the US. If the US raises 1% in 2019, I believe Canada will only raise by 0.5%.

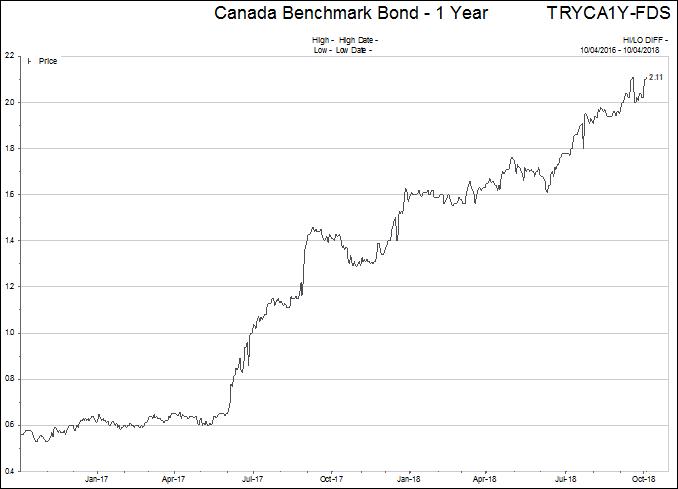

The chart below shows the 1 year Canada bond rate. It is also making new cycle highs as we speak.

These higher rates are already impacting Canada’s consumers. Real estate prices have moderated. Mortgage debt growth is slowing and car sales are off from last year.

Slowly, markets are feeling the impact of higher interest costs in Canada.

US:

The US economy is in a significantly better place than Canada.

Notice the higher yield on the US 10 year Treasury bond.

There are a number of problems that a 3.25%-3.75% US interest rate on the 10 year bond accentuates in America. Again, these interest rate issues are cumulative and do not dissipate with time.

Remember, my thesis remains that the US Federal Reserve will continue to raise interest rates until something breaks in the asset markets. Federal Reserve chairman, Jerome Powell, has been absolutely consistent in his statements as to intention.

Below is a chart of the yield on the 1 year US Treasury bond. It is hard to believe that less than two years ago this yield was under 0.50%. Just for fun, take $20 trillion in debt and calculate the interest owing at 0.50% then at 3.16%. Hmmm…big difference.

The last US interest rate chart I will show is the 30 year US Treasury bond going back 18 years. The red dotted line is the 100 month moving average.

Notice how each “touch” of the red line was “rejected” and 30 year interest rates quickly retreated lower (red arrows)….until now (yellow arrow)!

Interest Rate Summary: There is no real way to know when higher interest rates are going to have a meaningful impact on stock and real estate prices. What we know for sure is that they will make a difference at some point.

But I think the outlook is different for Canada and the US as to HOW this will happen.

For Canada, it most likely starts with consumers. The Canadian consumer is reminiscent of the American consumer of 2008. Our recession will likely be more severe and resemble the US downturn a decade ago.

The American consumer is in better condition this go around.

I think the recession in the US this time will center in the high yield and leveraged bond markets. These asset classes are totally out of control relative to historical levels.

The other area I expect challenges for in the US is the Federal deficit considering what's been outlined above. As shown last week, the deficit will near $2 trillion by 2022 even if interest rates just stay where they are right now!

At some point…interest rates are going to matter.

Gold

I have been getting a few more emails and calls about gold/precious metals lately.

The short opinion on this sector is that Gold prices need to clear $1250 US to really get interesting. Rising interest rates and a rising US dollar are not the ideal conditions for Gold to get itself into gear.

But therein lies the interesting part of where the Gold market resides at present.

Historically, the US dollar tends to rise in an asset BEAR market. Traditionally, this has not been beneficial to gold prices in US dollars.

So IF gold begins to rise in US dollars, while the US dollar is rising against other currencies, often those times have set the stage for large increases in the gold price.

Way too early to go down this road, we will just watch for now.

If you are interested in precious metals, or have questions about what's been discussed above please feel free to shoot me an email or give me a call.