This corporate earnings season and the next are oddities. This is not because of the double-digit retrenchments that we expect in earnings growth—that’s normal during recessions. A key reason we think the Q1 and Q2 reporting seasons will be outliers is because many management teams are having a very difficult time gauging the future amid COVID-19 uncertainties.

Given the abundance of unknowns about the contours of economic recessions and subsequent recoveries in North America, Europe, and globally, there is a meaningful lack of visibility about corporate profits, especially in economically-sensitive industries and those hit hardest by COVID-19 shutdowns.

As a result, we think investors should take 2020 and 2021 earnings forecasts with a grain of salt, and should use a range of estimates when attempting to gauge the future outlook for profits and equity market valuations.

A lack of guidance

Normally during earnings season, analysts and investors have a well-established playbook to work from—profit estimates for the current and next quarters that tend to come reasonably close to reality. Not in this COVID-19 environment. This go-around, many Wall Street industry analysts who cover individual companies will be left in the dark.

Our national research correspondent believes a meaningful share of S&P 500 management teams will withdraw earnings guidance during the Q1 reporting season due to substantial COVID-19-related uncertainties. Companies domiciled in other countries and regions will likely do the same, and we’re already seeing this play out in the early stage of the European reporting season.

There is not much incentive for management teams of economically-sensitive companies to go out on a limb to forecast earnings when operations in so many national and local jurisdictions are in flux and subject to government decisions on when and at what pace businesses can begin getting back to normal.

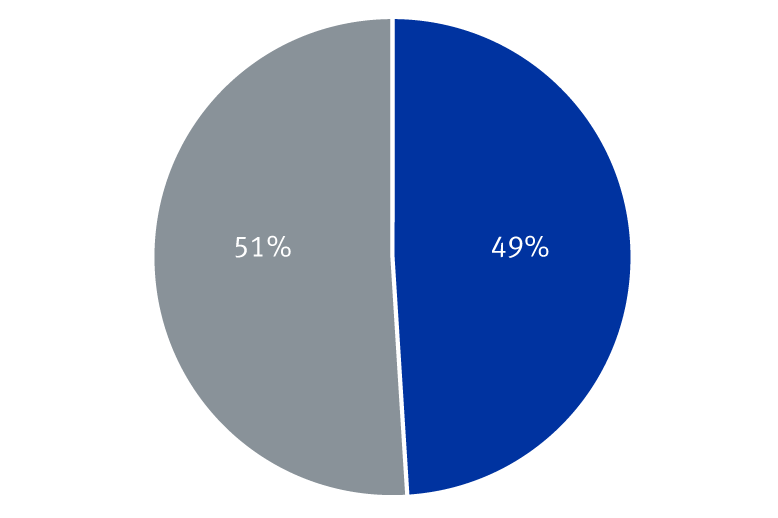

Before COVID-19 caught fire, roughly half of S&P 500 companies had not yet provided full-year guidance (this is not atypical for early in the year), while roughly the other half had provided guidance.

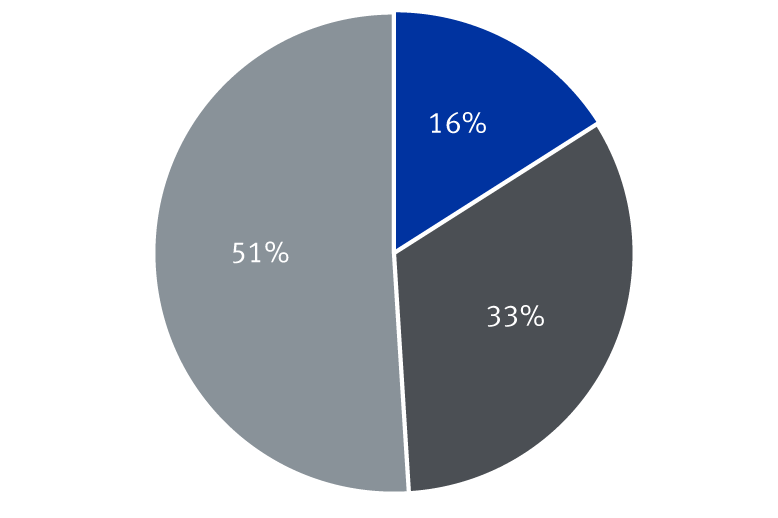

After the Q1 earnings season largely concludes in the latter part of May, our national research correspondent believes the majority of companies that had previously provided full-year earnings guidance will have withdrawn it. It also thinks the original pack of companies that refrained from providing guidance will continue to sit on the sidelines. It anticipates only 16 percent of companies will provide full-year guidance.

About one-third of U.S. large-cap companies are likely to withdraw earnings guidance

Percentage of S&P 500 companies that previously provided 2020 earnings guidance

Did not provide guidance

Provided guidance

Percentage of S&P 500 companies likely to provide 2020 earnings guidance post-Q1 results

Did not previously provide guidance

Likely to provide guidance

Likely to withdraw guidance

Source - National research correspondent, Standard & Poor's, FactSet; data as of 4/20/20

Room for movement

The lack of and withdrawal of earnings guidance would leave profit forecasts for this year and next even more in flux than they normally are.

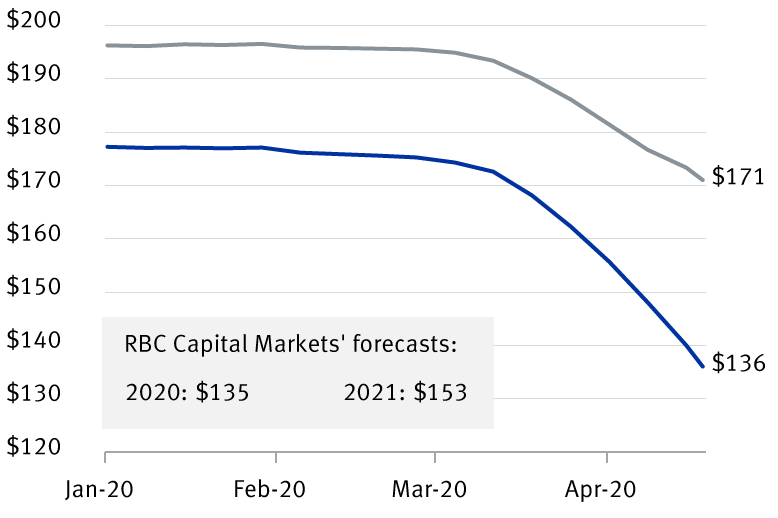

The S&P 500 consensus forecast for 2020 of $136 per share has declined substantially from $173 since mid-March, according to bottom-up estimates of Wall Street analysts aggregated by Refinitiv I/B/E/S, just as it should have amid COVID-19 risks. RBC Capital Markets is currently forecasting $135 per share.

Even though both of these 2020 forecasts are in the “reasonable zone,” in our view, there is still downside risk considering the Q1 reporting trends thus far. With 22 percent of S&P 500 companies having reported, 30 percent of them have missed the consensus forecast, a higher rate than usual. The 2020 consensus estimate could continue to drift down in the weeks ahead, and visibility about the remaining quarters of this year is lacking.

The 2021 consensus estimate of $171 per share still seems far too elevated to us, despite the fact that it has been cut from $197 per share at the beginning of the year due to COVID-19. RBC Capital Markets is at $153 per share for next year.

COVID-19 has pushed profit estimates down substantially, but is it enough?

S&P 500 consensus earnings-per-share forecasts

2020 consensus estimate

2021 consensus estimate

Rely on a range

At this stage, we think investors should take the bottom-up consensus earnings forecasts of Wall Street analysts and the top-down estimates of equity strategists with a grain of salt. We would use a range of estimates to gauge the future path of earnings and market valuations.

We think $125–$135 per share seems like a reasonable range for 2020 until more is known about the depth and duration of the U.S. and global economic recessions. We think $150 per share is a good ballpark estimate for 2021, but we wouldn’t hold onto it too tightly given the abundance of unknowns about the contours of the economic rebound.

Non-U.S. Analyst Disclosure: Jim Allworth, an employee of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc. contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since he is not an associated person of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.