While rising tides lift all boats – the amount risen depends on the boat !

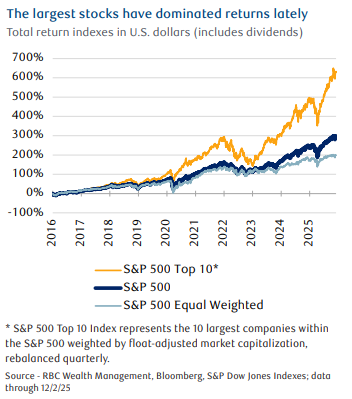

Not only has the U.S. equity rally been uneven in 2025, the segment of the market that has dominated during this bull market cycle has been narrow and concentrated mainly in the largest of large-cap stocks.

Not only has the U.S. equity rally been uneven in 2025, the segment of the market that has dominated during this bull market cycle has been narrow and concentrated mainly in the largest of large-cap stocks.

Following a 38 % surge from the April low through the all-time high in late October, the S&P 500 has been consolidating its gains, and leadership within the index has been rotating.

It’s useful to step back from the market’s recent movements and evaluate the unique contours that have sparked this year’s rally and the longer bull market run that began in October 2022.

- Mega Cap Stocks have outperformed significantly.

- Earnings growth for technology-related stocks has far outpaced the rest of the market.

As the chart above shows, soon after the bull market began, the performance gap widened notably between the 10 largest U.S. stocks and S&P 500 Index, along with its equal-weighted counterpart.

Except for the brief period during the tariff scare last April when the S&P 500 pulled back by almost 19 %, the pattern of a rising tide lifting the largest stocks more than others has defined this bull market cycle.

Since the bull run began on Oct. 12, 2022, on a total-return basis:

- S&P 500 Top 10 has surged 175 %

- S&P 500 has rallied 100 %

- S&P 500 Equal Weighted has risen 58 % It’s about fundamentals, not just AI hype The AI boom has contributed to the big rally in the biggest stocks.

Among the 10 stocks that currently represent the largest S&P 500 stocks by market capitalization—NVIDIA, Apple, Microsoft, Alphabet, Amazon.com, Broadcom, Meta Platforms, Tesla, Berkshire Hathaway, and JPMorgan Chase—the first eight are heavily involved with developing the emerging AI technology, and even the last two have AI exposure.

AI-related stocks have dominated this group in the past two years. During this period, these stocks have grown earnings much faster than the rest of the market and have generated free cash flow at a pace that’s well above the “average” S&P 500 stock.

In other words, their stock moves have not been driven solely by AI hype; there has also been meat on the bones in terms of company fundamentals.

Tech sector profit growth rapidly flipped from deeply negative territory in Q1 2023 to lofty levels, reaching almost 26 % in Q1 2024 and hasn’t really looked back since. In the past two years, the Tech sector’s profits have risen much faster than the broader market quarter after quarter, as the chart shows.

The old investment adage “past performance is not necessarily indicative of future results” applies in this case. Just because the largest 10 stocks within the S&P 500 have outperformed significantly so far during this bull market cycle doesn’t mean this pattern will automatically continue for the duration of the bull run. Much will depend on whether earnings growth of technology-related stocks continues to exceed other areas of the market to a meaningful degree—and whether the prospects for this will extend beyond 2026.

Another factor that could influence the performance of the largest stocks versus the rest could be the AI development cycle itself. Thus far, the phenomenon has been dominated by “AI 1.0,” which has been mostly a capital-spending story to build infrastructure and train and run AI models. The bulk of stocks within the S&P 500 Top 10 Index have benefitted from this over the past two years. The focus of the AI development cycle probably needs to start shifting to “AI 2.0,” where signs of productivity and financial benefits start accruing to companies not just inside, but also outside of the technology industry.

This could ultimately boost financials of certain industries and companies that aren’t necessarily in the center of the AI radar right now.

Given the very strong run that the largest S&P 500 stocks have had, now is an ideal time to check portfolio allocations. It’s prudent to double check their fundamental prospects and valuations, and if warranted, bring them back closer into balance.

If you have any questions or comments, please do not hesitate to let me know