The old line is that the cure for high prices is high prices. Economics are rife with such self-correcting mechanisms.

Today we’ll examine how exactly this is playing out in the relationship between the U.S. budget deficit and longer-term interest rates.

U.S. growth is solid, but perhaps not stable The U.S. economy has shown unexpected resilience during the post-pandemic era, mystifying both U.S. Federal Reserve and private sector forecasters.

One of the key factors has been the expanding federal budget deficit.

The growth in debt-funded government spending contributed to demand, helping push up household wages, corporate profits, and ultimately asset prices. The deficit provided a boost to the economy as it recovered.

Many are increasingly concerned with the magnitude of the government’s shortfall. At 6.5 % of GDP, we are in uncharted territory for the modern U.S. economy. This is the first time the government has run a deficit this large outside of a recession.

This is a risky evolution of fiscal policy.

It should be made clear that this is not a concern with federal debt. U.S. default fears are wildly overblown, and that the U.S. is rich in public and private sector assets and productive capacity.

The deficit is different – and it is troubling on two fronts.

- The potential for unsustainably fast growth putting pressure on inflation. The U.S. economy is firing on all cylinders, with high wages and investment returns fueling household consumption and artificial intelligence opportunities propelling corporate investment.

The additional boost from federal deficit spending adds to the demand.

What’s less simple is identifying slack to meet that demand.

Unemployment is hovering around 4 %, 1 % below its long-term median. The lift from technology sector productivity is unlikely to continue over the coming quarters.

Trade has often filled the domestic supply void, but that may be less available this time around. Potential for tariffs and higher scrutiny at border crossings would add upward pressure on prices.

- Bond Supply. Markets are certainly capable of absorbing U.S. Treasury bond issuance—Treasuries remain the most liquid security class in the world.

But pushing out trillions of dollars in bonds in less than 12 months risks straining investor appetite and balance sheet capacity.

Fast growth and inflation make equities and other growth-sensitive assets attractive compared to fixed coupons. This large supply means that borrowers—including the government—may need to pay higher coupons to attract buyers.

But high rates tend to be self-correcting. The shift can come in two ways.

The first is a slowdown in the private sector that offsets the government’s expansionary policies. To some extent, this is already happening.

Many corporate issuers have pulled billions in bond deals last month because rates were too high. Lower bond sales mean fewer investments and slower expansionary hiring. Historically, it’s been the federal deficit that has reacted to shifts in private sector activity, but there’s nothing to say the dynamic cannot work in reverse and we may be witnessing the early stages of that shift.

Neither the government nor the private sector blink, and growth continues at its current pace. If that proves inflationary, as seems possible, the Fed would be forced to respond, raising short-term interest rates to engineer a growth slowdown.

Neither the government nor the private sector blink, and growth continues at its current pace. If that proves inflationary, as seems possible, the Fed would be forced to respond, raising short-term interest rates to engineer a growth slowdown.

We are likely to see most of the work done by the private sector adjusting to higher rates. A this point, a rate hike is unlikely. This would see investors shift their rate cut expectations to later in the year.

There is another path forward: the federal government could move toward a more balanced budget.

While there are efforts in this direction—most notably by the Elon Musk-led team known as the Department of Government Efficiency, (DOGE) significant political hurdles to rapidly implementing large fiscal cutbacks remain.

Even with the risk of higher rates and the potential for slower economic growth as a result, the answer is not for investors to head for the sidelines.

For starters, we are talking about fundamentally healthy adjustments that the economy always undergoes—and that it needs to undergo. Additionally current yields provide a meaningful cushion against potential yield curve shifts.

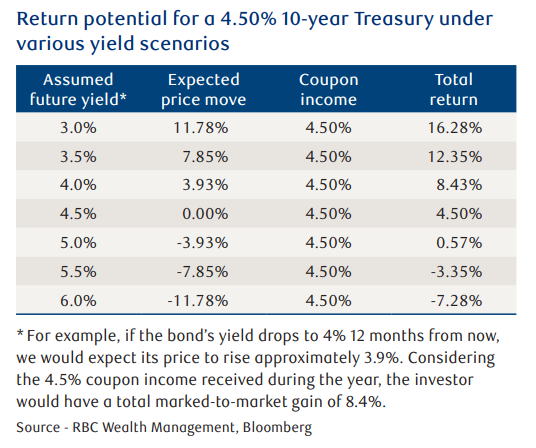

The table above lays out estimated returns for Treasury bond investors over a 12-month time horizon under various scenarios.

While marked-to-market losses are easily conceivable, the cash flow from coupons likely makes them manageable for most investors under a range of assumptions.

While one can map out a reasonable scenario of steady growth and a drift higher in interest rates, even the youngest of investors can remember shocks to the system from COVID to regional bank scares and the global financial crisis.

Holding a diversified portfolio of assets is a time-tested approach to dealing with unexpected event risk or recession or growth slowdowns.

Now is not the time to be scared, rather to extend the current robust growth framework as prudent investors have always done.

Please let me know if you have any questions or comments.