Higher productivity has driven the U.S. economy ahead of others in recent years.

This has forced other natio ns to meaningfully raise the stakes in the global race to harness emergent technologies such as Generative Artificial Intelligence (GenAI).

ns to meaningfully raise the stakes in the global race to harness emergent technologies such as Generative Artificial Intelligence (GenAI).

Productivity is measure of how efficiently resources are harnessed to generate economic value.

One of the more straightforward approaches to measuring productivity is labour - the amount of economic output per hours worked to produce it.

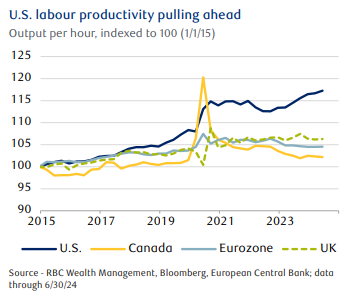

The U.S. has been consistently outpacing major advanced-economy peers for some time. Since 2014, workers in the U.S. have boosted their productivity by 17%.

By contrast, gains in the eurozone and the UK have been limited to 5% and 6%, respectively, while Canada’s productivity has stagnated.

This rise in worker efficiency has been a major factor supporting the U.S. economy’s faster growth trajectory over the past two years. Between Q2 2022 and Q3 2024, U.S. real GDP expanded by 6.7%, compared to 4.5% for Canada, 1.5% for the eurozone, and 1.4% for the UK.

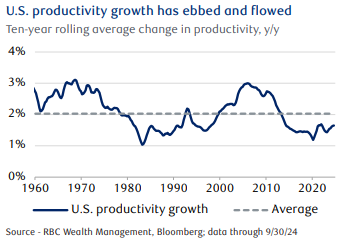

U.S. workforce productivity boasts a reliable record of long-term improvement. Since 1960, U.S. productivity has grown at a 2% compounded annual growth rate. Though seemingly modest, this steady pace has an extremely large cumulative effect: workers in the U.S. are now roughly 250% more productive than their 1960 counterparts. Productivity growth, however, has ebbed and flowed over the decades.

U.S. workforce productivity boasts a reliable record of long-term improvement. Since 1960, U.S. productivity has grown at a 2% compounded annual growth rate. Though seemingly modest, this steady pace has an extremely large cumulative effect: workers in the U.S. are now roughly 250% more productive than their 1960 counterparts. Productivity growth, however, has ebbed and flowed over the decades.

The recent upswing has come during the period of tepid progress in the 2010, when productivity grew at a compounded annual rate of just 1.2%—one of the slowest rates in the past seven-plus decades.

Small variations in productivity growth rates compound over time into vastly divergent economic outcomes.

At 1.2% annual growth, output per worker doubles roughly every 58 years. At 2.5%, it doubles in just 28 years. In real-world terms, that difference determines whether workers double their output once or twice over their careers.

The long-term trajectory of economies and the standard of living for households are closely tied to this, as wage growth tends to track productivity gains over time.

Productivity is the engine of long-term economic progress—and has implications for financial markets.

When productivity rises, economies can produce more goods and services with the same inputs. This not only boosts the value businesses derive per worker but also raises an economy’s “speed limit,” allowing faster expansion without fostering inflationary pressures. More productive workers also tend to act as a tailwind for corporate profitability, creating a virtuous cycle of growth and reinvestment.

When productivity rises, economies can produce more goods and services with the same inputs. This not only boosts the value businesses derive per worker but also raises an economy’s “speed limit,” allowing faster expansion without fostering inflationary pressures. More productive workers also tend to act as a tailwind for corporate profitability, creating a virtuous cycle of growth and reinvestment.

For the U.S., the recent rebound in productivity growth is encouraging, but sustaining it will require a concerted effort. The productivity edge the U.S. has achieved recently can be attributed to several key factors.

For the U.S., the recent rebound in productivity growth is encouraging, but sustaining it will require a concerted effort. The productivity edge the U.S. has achieved recently can be attributed to several key factors.

A deep-rooted culture of innovation and risk-taking has fostered rapid business formation and accelerated the diffusion of technologies through the economy, while flexible labour markets adeptly match workers to jobs aligned with their skills.

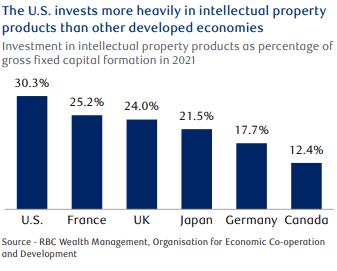

Crucially, high levels of investment in research and development have kept the U.S. at the forefront of technological leadership.

This offers a useful playbook for other major economies seeking to strengthen their productivity trajectory.

The emergence of GenAI presents an opportunity to reset the global productivity landscape, allowing lagging countries to bolster their productivity growth and close the gap with the United States, much like the computer did in the late 1980s.

As always, please let me know if you have any questions or comments.