Central banks’ inflation targets are in sight, but not all price trends have normalized.

Structural price pressures suggest policymakers should remain vigilant. Inflation isn’t the headache it was two years ago, but investors should keep it in mind in their asset allocation decisions.

Mission Accomplished … Sort Of

Central banks have made considerable progress reining in inflation, helped by improved supply chains and lower commodity prices.

Headline inflation is below 2.5 % in the U.S., UK, and eurozone, while the Bank of Canada (BoC) managed to hit its 2 % target in August for the first time in 3.5 years.

Policymakers are now shifting their focus to growth and labour markets, aiming to stick the soft landing.

Are we there yet ? Well, let’s say we are getting closer.

There are still pockets of price pressure—most significantly in housing and other services—that are cause for concern, and upside risks to inflation remain. There are also several structural forces that could keep inflation on the high side of 2 % over the medium term, unlike throughout the 2010s when inflation tended to fall short of central banks’ targets.

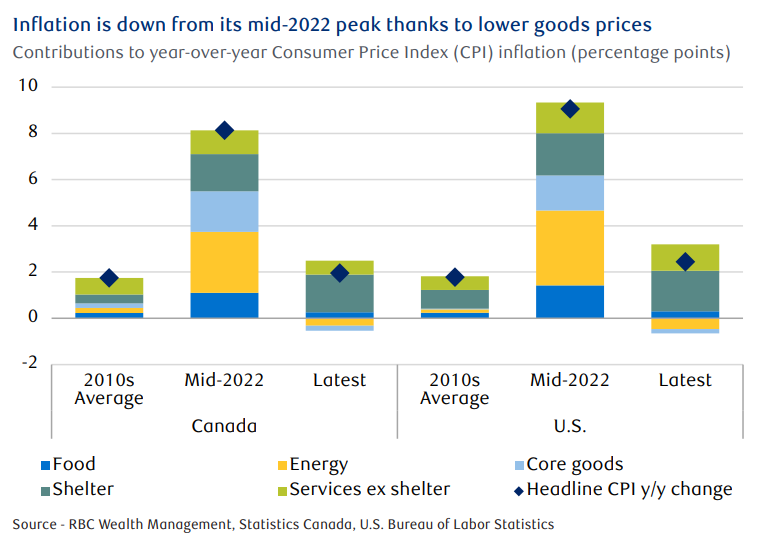

The dramatic inflation slowdown from its mid-2022 cycle high has been concentrated in goods prices.

Energy price growth has normalized after the combination of war in Europe and a post-pandemic travel resurgence have led to upward price pressure in 2022.

The supply chain issues and high demand that drove food and core (non-food and energy) goods prices higher have since eased. Central banks can take some credit for tight monetary policy reducing demand for goods, but factors outside their control were also key to reining in inflation.

Services prices haven’t normalized to the same extent.

Non-shelter services inflation, which is thought to be a good barometer of domestically generated price pressures, has come down from cycle highs but remains elevated relative to pre-pandemic levels, particularly in the United States.

Despite a cooling labour market, U.S. wage growth has accelerated slightly in recent months. However, strong pay gains appear to be justified by the U.S. economy’s robust productivity growth. That’s not the case in Canada, where productivity has been sluggish and growth in unit labour costs remains too high for the BoC’s comfort.

Policymakers are hoping that rising unemployment will reduce labour cost pressures going forward. Recent labour disruptions and large wage settlements on both sides of the border show that workers looking to play catch-up after a period of high inflation can keep wage growth sticky.

Shelter inflation is another source of ongoing price pressure thanks to tight rental and housing markets. In the U.S., rent and owner’s equivalent rent (what a homeowner could charge to rent out their home) lagged rising market rents. In Canada, still-rising rents, and higher mortgage interest costs are keeping upward pressure on shelter inflation.

Slower immigration on both sides of the border might help alleviate some rental market pressure, but historically low vacancy rates could make a return to pre-pandemic shelter inflation levels.

More To Come ?

While central banks deal with these lingering price pressures in services, they must also be cognizant of upside risks in goods prices.

Oil prices are no higher than they were a year ago, prior to the breakout of the Israel-Hamas war, but spiked higher recently amid concerns about broadening conflict in the region. Russia’s invasion of Ukraine was a key contributor to rising energy prices and peak inflation in 2022, and geopolitical tensions remain a key risk to inflation, even if energy is a non-factor in current CPI readings.

Many comparisons have been made between the current cycle and the dual waves of inflation seen during the 1970s. While such comparisons may be overblown, it’s worth remembering that geopolitics and oil prices were key drivers of that second wave of inflation in the 1970s.

Trade policy is another inflation key topic ahead of the U.S. election. Neither political party has been a strong booster of free trade recently. As noted in a recent article, Donald Trump has said he favours doubling down on protectionist policies. His proposal for across-the-board tariffs of 10 % or more on all imports and high tariffs of 50 % or more on Chinese imports could add 0.8 % to domestic inflation, according to an RBC Global Asset Management analysis.

Even if those policies are only partially implemented, higher tariffs could be an unwelcome inflation headache for the Fed.

Beyond these near-term risks, there are a number of structural factors that could exert upward pressure on inflation in the medium to long term:

- Rising U.S. government debt levels is not default but inflation. High levels of government spending put upward pressure on prices, and high debt loads encourage governments to inflate away the value of existing debt.

- Tariff threats are part of a broader deglobalization trend that could put upward pressure on goods prices after two decades of globalization-capped core goods inflation.

- Tight labour markets have put upward pressure on wages, and there could be a structural element as retiring baby boomers limit labour supply growth.

As always, please let me know if you have any questions or comments.