Large-cap tech stocks have dominated U.S. equity performance this year, but recently the rest of the market has been trying to take the baton.

Let’s discuss the main factors needed to make a clean handoff.

The question facing the U.S. equity market is whether S&P 500 performance will finally broaden out beyond the mega-cap artificial intelligence (AI) stocks. There have been fits and starts since this leg of the rally began in late October 2023, but lagging AI-related stocks notably in total and unable to grab the leadership baton.

However, in recent trading sessions performance has flipped.

A group of eight S&P 500 sectors has outperformed the three most  AI-leveraged sectors.

AI-leveraged sectors.

The Dow Jones Industrial Average and small-capitalization indexes have also outpaced the more AI-exposed S&P 500.

This trend accelerated on Wednesday following press reports that the Biden administration is seeking to impose even tougher trade restrictions on companies based in the U.S. and allied countries that sell semiconductors and semiconductor capital equipment to China, many of which are leveraged to the AI theme.

The Q2 earnings season, which began recently, may provide clues about whether the rotation away from AI-related stocks, into other areas of the market, will stick.

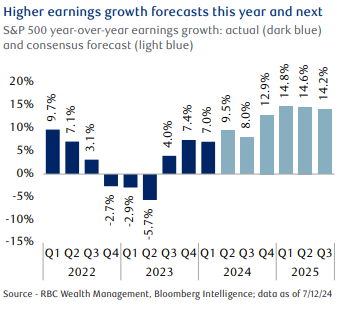

S&P 500 earnings are expected to grow this year and expand further next year according to the consensus forecast. Whether this outcome transpires could largely depend on economic momentum.

If the economy can resume average or above-average growth in coming quarters, potentially helped along by Fed interest rate cuts, then this S&P 500 earnings growth trajectory would be plausible. However, if economic growth remains below average like it was in Q1, slows to “stall speed” (between 0% and 1 %), or finally succumbs to recession, the current consensus earnings growth forecasts would be unachievable.

Cracks in employment and manufacturing raise questions about economic momentum, but recent improvements in retail sales, lower interest rates on mortgages and other loans, and bond market signals that the Fed could start cutting rates in September provide reasons for cautious optimism.

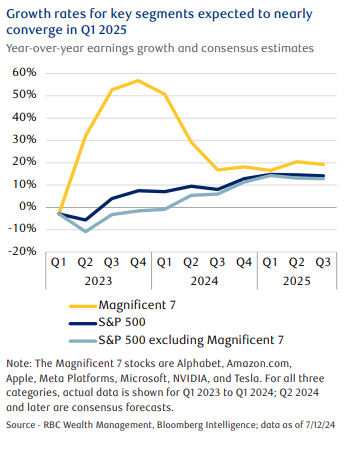

The profit trajectory of two important S&P 500 segments will likely be another major determining factor in whether non-AI parts of the market, particularly economically-sensitive sectors (aka cyclicals), can assert leadership over a sustained period.

The profit trajectory of two important S&P 500 segments will likely be another major determining factor in whether non-AI parts of the market, particularly economically-sensitive sectors (aka cyclicals), can assert leadership over a sustained period.

The year-over-year earnings growth rates for AI-leveraged Magnificent 7 stocks and the rest of the market are set to nearly converge around 15 % in Q1 2025. The consensus forecast projects Mag 7 earnings growth to slow meaningfully by Q3 of this year and then level off, whereas growth for the rest of the market is expected to steadily improve by Q1 of next year, before flattening out.

If institutional investors become increasingly confident this earnings convergence story could play out sectors and industries outside of the Magnificent 7 and AI-focused areas of the market in the coming weeks and months could continue to outperform.. This could result in a broader group of sectors taking the performance baton.

Management teams’ earnings guidance and commentary during the Q2 reporting season should provide hints about whether the consensus forecasts for both segments are feasible or need adjusting. It’s notable that the convergence story has already been pushed out; three months ago, it was expected to transpire in Q4 2024.

U.S. equity market volatility could increase during the second half of this year as economic and earnings growth uncertainties get resolved. Volatility typically perks up at some point during election years.

The S&P 500’s 12-month forward price-to-earnings ratio of 18.6x excluding Magnificent 7 stocks is above average, but not extreme from our vantage point—so long as consensus earnings estimates and GDP growth hold up.

We recommend tilting U.S. equity holdings toward quality dividend-paying stocks and areas of the market that have lagged this year given that the baton could finally shift to such sectors for longer than just a brief stint.

Specifically, we favor Financials, Health Care, and Utilities.

If you have any questions, please feel free to let me know.