Good Morning,

While AI and the Magnificent 7 have obvious contributors to this bull market, today we will spotlight two other trends with a clear impact on portfolio performance.

The S&P 500 continues to surge in 2024 despite numerous concerns, and narrow leadership.

The result is a bull market that many investors find unlikable, as the surge to record highs may appear unjustified from an economic perspective.

2 telling trends have emerged: dividend yields and earnings revisions.

Low Yield Stocks Have Outperformed

Low dividend yields continue to be highly correlated with outperformance, meaning that higher-yielding equities are underperforming lower-yielding ones.

Some of the mega-cap tech stocks have now moved to paying small yields (1 % or less including Meta Platforms and Alphabet). The no-yield category is one of the worst-performing segments, rising only 3.4 % year to date.

The no-yield segment of the market has underperformed all other segments, on average, except for stocks with yields greater than 3 %. However, the average data doesn’t tell the full story.

Many of the no-yielding stocks have actually performed quite well.

Many of the no-yielding stocks have actually performed quite well.

When accounting for the upside/downside ratio of no-yield stocks, the return profile improves dramatically.

High dividend yield continues to be a critical factor in 2024 underperformance.

Conversely, many no-yield stocks and the low-yield group as a whole are correlated with outperformance.

For example, stocks with yields of less than 1 % have rallied 18.0 % year to date, on average, exceeding the S&P 500’s strong 17.8 % return.

Analyzing Earnings Revisions

Another more consistent driver of outperformance over time is higher earnings estimate revisions.

This year, companies that have seen their 2024 consensus earnings estimate rise have outperformed those that have seen earnings per share (EPS) estimates fall.

Considering change in EPS estimates into six categories from worst to best, we can see that with each improvement in the EPS change category, average share price performance has climbed.

For example, stocks with earnings estimates that declined more than 10 % (the worst segment) fell 5.1 % year to date, on average – while stocks with earnings estimates that rose more than 10 % (the best segment) rose 26.6 % on average.

Positive estimate revisions are one of the more traditional indicators of equity outperformance, which holds true in 2024 despite all the competing crosswinds present in the market.

It becomes quite clear that high-performing stocks in the S&P 500 typically show below-average dividend yields and above-average earnings estimate revisions.

The top 10 performing stocks in the S&P 500 in 2024 have returned 94.7 % on average, significantly outperforming the S&P 500’s 17.8 % gain. The average dividend yield of this outperforming group is 0.7 %, roughly half that of the market. The average 2024 estimate increase for this group is 17.0 %, more than 7x higher than that of the market.

To identify future investment opportunities, we think it helps to understand recent market movements because they can provide context for forward-looking decisions.

To identify future investment opportunities, we think it helps to understand recent market movements because they can provide context for forward-looking decisions.

Currently, we are in a market characterized by narrow leadership, low-dividend outperformance, and a scenario where inflation is slowing and unemployment is still manageable. When these factors change, the high-quality equities that have been underperforming will likely benefit.

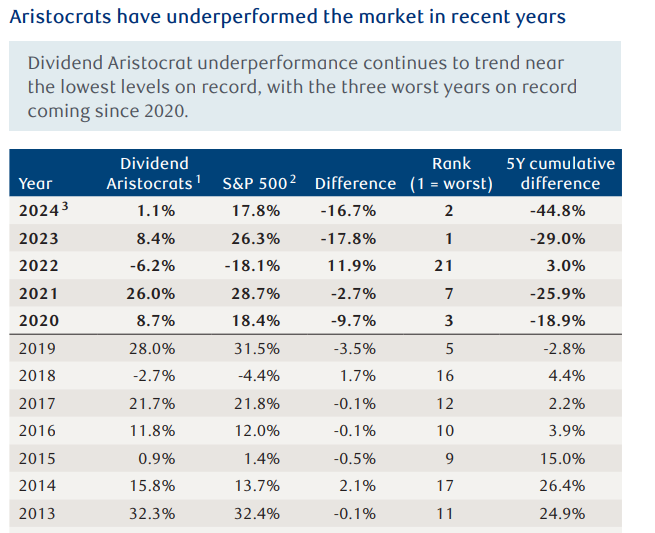

Using the Dividend Aristocrats basket (S&P 500 companies that have increased their dividends in each of the past 25 consecutive years) as a proxy for underperforming, high-quality stocks, this basket of companies is mired in its worst multiyear performance stretch on record.

Over the past 20 years, 2023 was the worst year of underperformance for the Dividend Aristocrats compared to the S&P 500, as the table above shows.

2024 is on pace to be the second-worst year. Four of the five worst years of underperformance have occurred since 2019. The result of these outcomes is a stretch of never-before-seen underperformance of the Dividend Aristocrats compared to the S&P 500.

Considering all of this, the probability that high-quality stocks will outperform when the investment landscape changes is much better today than on average. The Dividend Aristocrats have historically delivered their strongest performance during and following economic slowdowns.

The fundamental thesis for these high-quality equities is supported by attractive valuations compared to the broader market and business models that have historically weathered economic volatility better than the market at large.

We are in a frustratingly narrow market ! It is important for investors to stay disciplined and consistent by executing on their investment plan and identifying future opportunities. High-quality dividend-paying stocks are in a favorable position for when the investment landscape changes again, as it is sure to do.

As always, please let me know if you have any questions or comments.