Problems with supply chains have become a greater source of concern and are underpinning inflation pressures.

There is no quick way to relieve the bottlenecks.

We examine the root causes, and discuss the impact on the equity market.

As major equity indexes came off the boil in September, key reasons for the market’s retreat were supply chain constraints and their knock-on effect on inflation.

The problems have been present and well known for many months, but they have become exacerbated recently. In reality, they are unlikely to fade away anytime soon.

While COVID-19 prompted much of the supply chain bottlenecks, there are other factors also at play:

- A sharp increase in demand for goods: As the global economy re-opened after being nearly shut down in 2020, demand surged.

- Supply chains aren’t built for this. The pandemic has sparked lifestyle changes as household spending has shifted more toward goods and away from services. This has resulted in shipping volumes from Asia to North America are up 27 % compared to pre-pandemic levels, according to RBC Global Asset Management (RBC GAM).

- Labor shortages in a variety of industries: This has occurred for multiple reasons, including ongoing concerns about COVID-19 risks, a mismatch between job openings and qualified applicants, and perhaps changes in career goals and priorities helped along by the pandemic. In August, the proportion of the American workforce that voluntarily quit their jobs surged to the highest level on record going back to 2001.

- Low supply of container ships: The shipping industry was running low on ships even before the pandemic. Over many years, the number of shipyards worldwide has dropped 63 % since the previous peak level in 2008, according to RBC GAM. More ship capacity will likely go offline as new regulations come into force in 2023 that will require ships to be retrofitted for environmental purposes.

- High shipping costs: The most widely followed measure of container shipping costs, published by research firm Drewry, indicates that while container prices have retreated a bit so far in October, they are still up 283 % from a year ago.

- Abnormally long processing times at ports: Shortages of longshore workers and increased demand for goods have backed up container and ship positioning. When ships sit idle off the coast it reduces the number of trips they can take, and the backlog mounts.

- Truck driver shortages: Land-based transportation systems are having difficulty processing the large volume of containers stacked up at ports because of the COVID-19-related shortages of truck drivers, particularly in North America.

- Lean inventories: Global supply chain problems quickly become consequential and multiply when inventories are tight. Moreover, because the problems are well known, orders for raw materials, component parts, and finished goods are now being placed earlier than normal, which is lengthening the queue, creating a vicious cycle, RBC GAM points out.

- Energy price spikes: This problem has surfaced more recently, and could persist through the winter, at least. Recently Chinese manufacturing has been constricted by power shortages and rationing due to high coal prices and the government’s power consumption limits. The surge in natural gas spot prices in Europe has hampered the fertilizer industry, which impacts agriculture production and prices. Power bills for businesses and households are on the rise in Europe and Asia.

- The UK’s own unique problems: Brexit labor rules that place restrictions on EU workers have hobbled distribution channels. Separately, trade frictions between the UK and EU are at risk of heating up in the coming months over the Northern Ireland protocol, which could cause another set of supply chain challenges.

The bottlenecks are unlikely to disappear overnight.

Our recent RBC Elements Digital Intelligence Study had indicated that 77 % of the major ports it monitors were experiencing abnormally long turnaround times, and that the overall global problem was trending “unequivocally worse.”

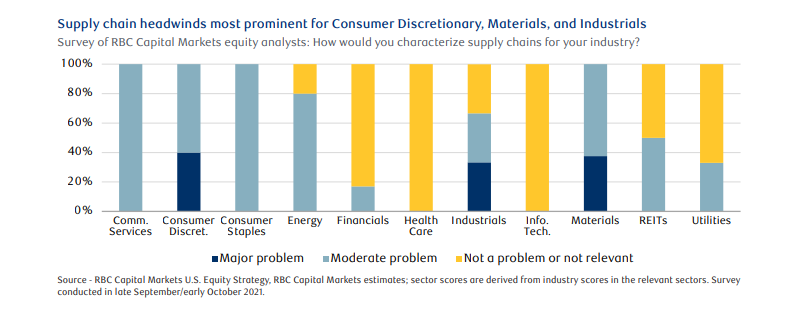

There is an important distinction to be made between the impact on the global shipping industry and the impact on U.S. stock market sectors. Some sectors are experiencing major-to-moderate supply chain problems (Consumer Discretionary, Materials, and Industrials), while other sectors are not experiencing problems (Health Care and Information Technology).

The remaining six sectors seem to be coping, and fall somewhere in between, as the chart illustrates. Lori Calvasina, RBC Capital Markets, LLC’s head of U.S. equity strategy, believes the survey results indicate that supply chain problems facing the broader domestic equity market “may not be as dire as September headlines suggested.”

Management teams’ comments during the Q3 earnings reporting season should provide further insights on implications for profit margins, and on the magnitude and potential duration of the problem. RBC GAM’s Chief Economist Eric Lascelles anticipates that the holiday shopping season will keep shipping costs “extremely high” over the next couple months, and thinks supply chain problems could persist another six months to a year. It will take time to resolve the labor supply/demand mismatch.

Some firms have already warned that bottlenecks could last into 2023. The path of the pandemic could play an important role, after all, it is the source of much of the stress. Calvasina notes that the trend in global COVID-19 infection rates has been a loose leading indicator for freight costs. So if infections peaked in September 2021, there could be relief over time.

Ongoing supply chain pressures will likely be a headwind for economic growth and have knock-on effects on inflation over the near term and possibly midterm. However, once supply chain pressures ease—with the increase in shipping costs and product input shortages eventually abating—this should end up being a deflationary and pro-growth force for the U.S. and global economies.

As long as supply chain problems don’t worsen meaningfully or drag on for an extended period, we think the overall impact on corporate profits and the equity market will be contained. But this issue is one of the reasons we believe inflation will remain elevated in North America and will rise in Europe and Asia, and that equity market volatility could persist and returns could be more muted in the next 12 months.

As always, please let me know if you have any questions or comments.