A growing chorus on Wall Street is warning a bubble may be forming in the U.S. stock market.

But before thinking this AI-led rally could be too much of a good thing, investors should note some key differences vs. the Tech Bubble peak 24 years ago, along with other healthy signs we see today.

While a near-term pullback can’t be ruled out, this is likely not Tech Bubble 2.0.

The S&P 500’s rally since late October 2023 ranks up there with some of the biggest moves within a short time frame in market history, and the index continues to rack up new all-time highs.

The dominance of the so-called Magnificent 7 technology-oriented stocks (Apple, Microsoft, Alphabet, Amazon.com, NVIDIA, Tesla, and Meta Platforms) that are leveraged to artificial intelligence (AI)—especially in the past year— can’t help but harken back to the Tech Bubble about a quarter century ago.

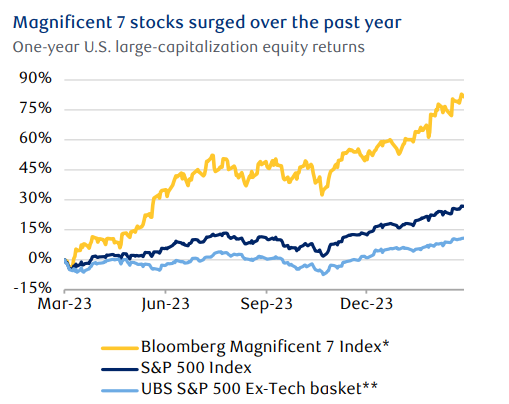

The Magnificent 7 stocks as a group have surged over 80 % in the past year, whereas the S&P 500 has climbed around 27 % through Mar. 4, 2024. When the Magnificent 7 and other technology-oriented stocks are excluded from the S&P 500, the gain is a much more modest 10.8 %.

The Magnificent 7 stocks as a group have surged over 80 % in the past year, whereas the S&P 500 has climbed around 27 % through Mar. 4, 2024. When the Magnificent 7 and other technology-oriented stocks are excluded from the S&P 500, the gain is a much more modest 10.8 %.

With such stark differences between tech and non-tech, it’s no wonder we’re starting to get questions about whether tech stocks are getting bubbly again.

It’s important to distinguish between market trends of the past year and the rally that began following the low in late October.

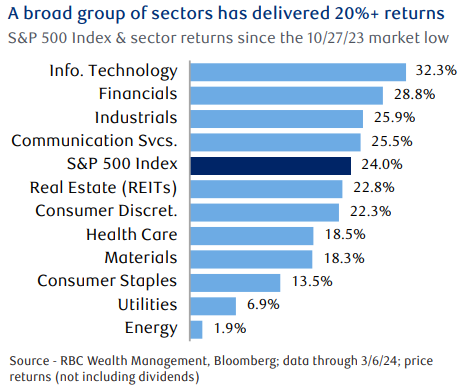

The Magnificent 7 stocks and technology-oriented stocks in general have dominated both periods. But market performance has broadened out since late October.

Financials, Industrials, and Real Estate—diverse economically sensitive sectors—have risen over 20 %. Their gains are up there with the three sectors boosted by Magnificent 7 stocks: Information Technology, Communication Services, and Consumer Discretionary.

Market performance has gone beyond just the Magnificent 7. This as a healthy sign.

Since late October, in addition to AI enthusiasm, the market has been driven by solid Q4 earnings results combined with optimism about 2024 profit growth. It also has been supported by sturdy economic data and declining inflation, along with investor anticipation that the U.S. Federal Reserve will start cutting interest rates at some point this year.

That was then, this is now

That was then, this is now

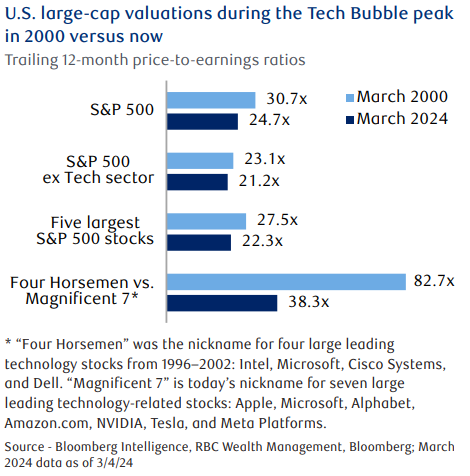

Second, it’s important to consider the key differences between the Tech Bubble peak in March 2000 and conditions today. The combined price-to-earnings (P/E) ratio of the Magnificent 7 is much lower than that of the so-called “Four Horsemen” stocks (Intel, Microsoft, Cisco Systems, and Dell), the group that powered the Tech sector higher back in the bubble days. Today, the Magnificent 7 trailing 12-month P/E is 38.3x, whereas 24 years ago the

P/E was an extremely pricey 82.7x, according to Bloomberg.

Beyond the Four Horsemen, part of the rally during the Tech Bubble era was fueled by companies with no earnings and some that barely had operational track records. These were dot-com firms that went public practically overnight—and collapsed almost as rapidly.

That’s not the case this go-around.

The AI move and rally in other Tech stocks has been fueled by established firms with years of profits in the books, long operational track records, and experienced management teams. Furthermore, there are valuation disparities between then and now. The S&P 500 as a whole, the S&P 500 excluding the Tech sector, and the five largest stocks by market capitalization are all less expensive today than they were 24 years ago.

The AI move and rally in other Tech stocks has been fueled by established firms with years of profits in the books, long operational track records, and experienced management teams. Furthermore, there are valuation disparities between then and now. The S&P 500 as a whole, the S&P 500 excluding the Tech sector, and the five largest stocks by market capitalization are all less expensive today than they were 24 years ago.

At this stage, Tech Bubble 2.0 is unlikely to occur. But this is no reason to throw caution to the wind.

The S&P 500’s surge since late October ranks with some of the biggest moves within a short time frame in market history. The market is bound to take a breather at some point and a pullback can’t be ruled out – however -forerunners of bear markets—lofty investor sentiment and declining market breadth—are not yet in sight.

Even though valuations are below where they were during the Tech Bubble peak in March 2000, the market is not inexpensive today. Valuations are above average and stretched, in our assessment, and typically don’t stay at such levels for long periods of time.

RBC Global Asset Management Inc. Chief Economist Eric Lascelles estimates that the risk of a U.S. recession is about 40 %. While this is down from about 70 % last year, the risk is elevated compared to periods of economic calm. Some leading indicators are still signaling that an economic contraction can’t be ruled out, especially if employment deteriorates and/or inflation becomes sticky or increases.

These factors should be reflected by maintaining Market Weight positioning in U.S. equities with a watchful eye on market trends.

As always, please let me know if you have any questions or comments.