Elmer Fed? Current media headlines might seem to jump-up-and-down more than usual, which would be an accomplishment. This week the Globe and Mail sent advisors in Canada a morning missive about the ”Hawkish Fed,” a term implying tough-love rate hikes from the daddy of central banks. This comes as the bank looks and sounds more chicken hawk than hovering condor.

Heading in to Father’s Day, we could be excused for thinking of the Fed as that non-meat-eating dad who’s never spanked his kid. Lest Johnny’s fragile psyche be nicked, discipline looks something like: “I love you, John-John, but… uh, I mean -- and… please remove the fork from your sister’s eye… J-J-dudykins, my smart-smart boy, please don’t bite the iPad. I’m going to count soon. And then… no avocado for you tonight!”

This week, analysts moved beyond measuring every word that comes forth from the mouth of the Seer of Bond Yields – graduating to full-on textual analytics. Sort of. A chart (below) helps us visualize… wait for it… what we think they’re thinking at the Fed, and… you guessed it… what we think they’ll be thinking after – they already thought what we thought they’d think – and all of this is projected out 2 ½ years in advance.

So that’s super handy.

And in truth, super necessary. When rates are this low, modest changes matter a whole lot. In effect, there’s a very active marketplace of expectations, and the medium of exchange is Deep Space Financial Klingon. Every message is worth translating, even loosely. Watch closely Mr. Spock.

The baby feds more or less dangle alongside or just behind US Fed policy, trying not to spit up on their trousers. Scanning the related headlines this week:

- Germany announced measures to keep interest rates negative next year;

- The Swiss announced a target of -.75% for its policy rate;

- The UK forecast reducing purchases of their own bonds soon;

- China obfuscated (always insert this line);

- The ECB announced a 3-day retreat to discuss a policy to strike a committee by the end of summer to tackle climate change, while bickering over ECB inflation/ rate policies – and… um, hey look! There goes Justin Trudeau riding on the back of a mosquito! “Marvelous hair Justin! Hey… Psst! Who invited him? Somebody call security!” (I made up part of that, but which part?)

- Yesterday the US Fed announced that sometime between now and the end of 2023 they might raise target short term interest rates from 0% to .50%. That might sound about as scary as Dr. Tongue’s 3D House of Pancakes (look it up), but they’re both something we should watch.

This week’s Global Insights piece is here: Global Insight Weekly

TLDR (Too Long Didn’t Read)?

Highlights here:

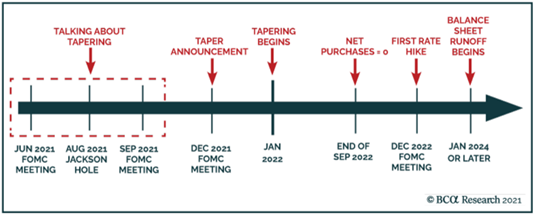

- A first step on the long journey to rate hikes? – As noted in the preamble, the Federal Reserve opened the door to discussing asset purchase tapering and future interest rate increases. But with a long road still ahead, and inflation top-of-mind for many, we look at the economic factors that could shape future Fed policy. (page 1)

- Notable sector trends in the U.S. equity market – Stocks are on track to break their three-week streak of moving higher after the Fed’s recent release. And we look at what the recent divergence in sector performance means for long-term portfolio positioning. (page 3)

- Regional highlights: Resale activity in the Canadian housing market declines again; STOXX Europe 600 Index posts ninth successive record high; China economic activity normalizing (pages 3-4)

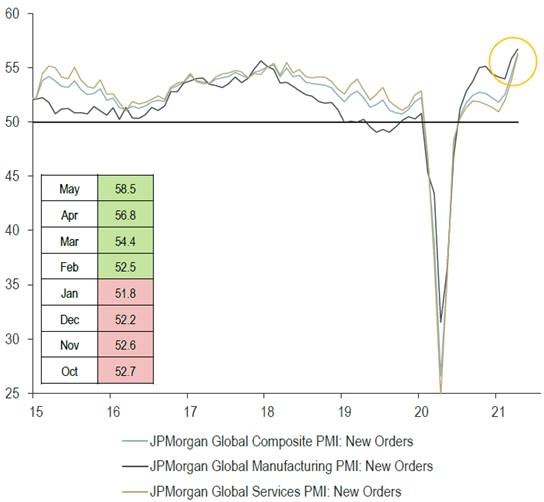

Inflation, and Pie-sky PMI: This chart measures aggregate purchase ordering flow, which says something about inflation expectations. It’s probably not evident to non-geeky people at a glance, but this is good news. Purchase ordering is really quite brisk right now. In a back-to-work environment, that probably means some of the supply pressures will alleviate in coming weeks/months.

Have a great weekend !

Mark