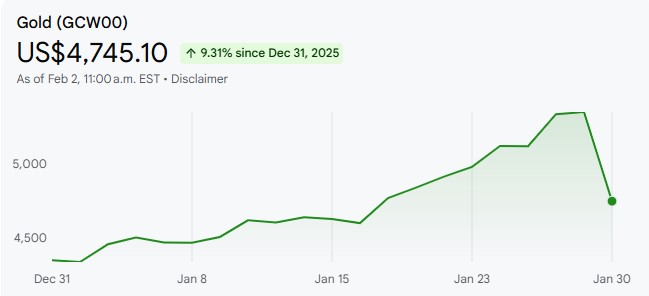

Nominee announcement of Kevin Warsh triggers big risk-off liquidation Friday. Gold, Silver, Copper, all the metals were down big. The markets view of Warsh is hawkish, leading the US dollar to surge in value. Gold was down more than -12%. Even more remarkable, Gold was still up nearly 10% on the month.

- Gold plunges in most brutal selloff in 40 years | Financial Post

- Silver, gold sell off as precious metals markets nosedive

Is the rally in metals ending or oversold? My thought - this is likely a correction back to a long term uptrend. There was froth and excitement, and markets got a reality check - nothing more, nothing less.

A weakening US dollar remains one of the trends to be aware of for 2026. This is a tailwind for the metals. We continue to favour them in portfolios, but will stick to our process and trim profits regularly. The biggest mistakes are made when you ignore your principles because of moves in market prices.

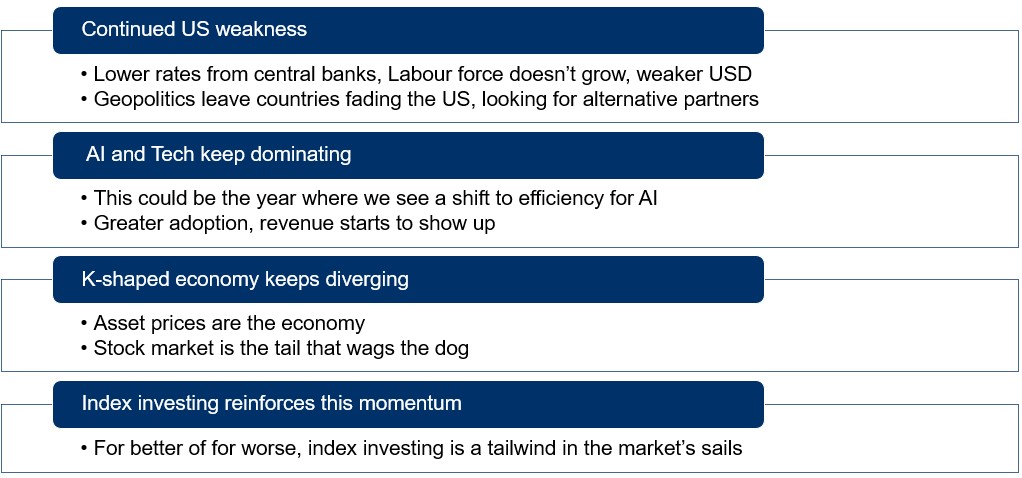

Trends we need to be aware of for 2026. After attending numerous 2026 outlook presentations and our very own annual Portfolio Manager’s conference – here’s my quick summary of what to expect.

- 2026 will look a lot like 2025.

- The AI and Tech music keeps playing. The list of tail risks keeps growing.

- We expect fits and starts, with bouts of volatility and big risk off events.

- Remember - Markets take the escalator up, and the elevator down.

- Come year end, we end 2026 with positive returns.

Yes – Inevitably the uptrend will end… likely in a very dramatic fashion.

No – the alarm bells aren’t ringing for an imminent end.

We think it’s a better bet to befriend market enthusiasm. Stay balanced, participate in the upside, harvest your profits, and when volatility strikes - take what the market gives you.

If you’d like to learn about the why, here are the structural trends that will shape 2026. We’ll be revisiting these themes throughout the year as they continue to evolve and shape world around us.

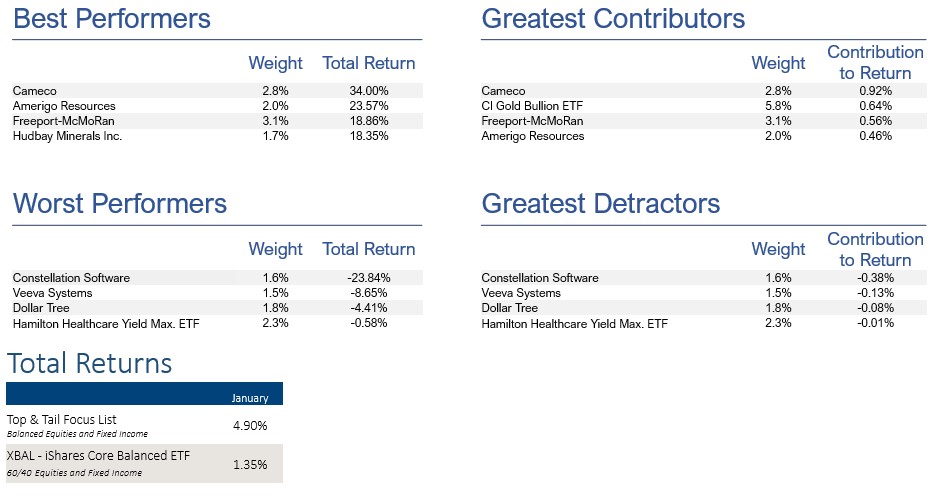

Top & Tail Focus List – February 2026

Overweight to commodities lifts focus list up +4.9% in January, outperforming our benchmark by 3.55%.

Money is emotional. When markets are up, you can be tempted to let your positions ride.

Worse – when they’re down, you can be tempted to sell (The Cardinal Sin).

This time last month, I made the decision to leave the Focus list unchanged as we transitioned from the Paper Portfolio format. We were overweight the metals, but I chose to deviate from my rebalancing rule in favour of a simplified transition. This overweight ended up in the focus list outperforming the benchmark by a wide margin.

Transparency is very important to me.

Full disclosure - 99% of client portfolios do not have a 21% exposure to commodities and materials.

As these assets have rallied significantly over the past few months, and the Focus List is only updated monthly, we had a fortuitous, but in all honesty, unrealistic drift upwards.

I can’t praise the performance, as it would be emphasizing one of my investing sins.

One common denominator for every investment mistake – deviating from your principles and tolerances.

As markets continue to push for all-time highs, we remain defensive and focus on outperforming to the downside.

We'll be harvesting profits in our materials positions, rebalancing and reducing our weights in the focus list. This profit taking will result in a handful of new positions.

February Changes to the Focus List

Consolidating and reducing our materials exposure

- Adding 6% position in Dynamic Active Mining Opportunities ETF (DXMO)

- Removing our positions in ARG, HBM, DXAU

- The thesis metals would rally worked. When the tide lifts all boats, picking individual names is easy.

- Now, I have less conviction in specific names that can continue to outperform. I’m inclined to let the specialists take the wheel.

- Compared to DXAU, DXMO is diversified across a number of metals including Gold, Copper, and Uranium.

- Realizing profits and reducing target weightings in Cameco (1.5%), Freeport McMoRan (2.5%), and Gold Bullion (5%).

- This will reduce our exposure to gold bullion and materials from ~23% to 15%

- Still a modest overweight compared to most benchmarks.

Adding notable names from our RBC DS Portfolio Managers Conference

- We’re allocating the 8% in metals profit taking to the following

- Loblaws (1.5%) and Amazon (1%)

- Food Inflation is insane, and margins aren’t going down. This trickles down to the bottom line for both companies.

- Loblaws is slowly looking more and more like Amazon. They’ve added logistics to their business, leasing out trucks for transport instead of driving back from deliveries empty. They’re also optimizing warehouses and leasing out space.

- Fairfax Financial (1%) and TMX Group (1%)

- Loan growth for the Canadian banks was minimal last year. They profited handsomely from non-recurring line items. This leaves us looking for financial exposure elsewhere.

- With elevated Inflation the past few years, insurance premiums have moved up in lock-step. Fairfax Financial has an excellent management team and is a bargain at these prices.

- As Interest rates have trended down, we expect M&A and IPO transactions to pick up, especially in a materials heavy Canadian market. TMX operates the Toronto Stock Exchange and they stand to benefit from this increase in transactions.

- The Rails: CP (1%) and CNR (1%)

- The last three years, railroads have experienced a freight recession. As policy and governments shift their focus to the importance of natural resources, both rails stand to benefit from an increase in demand.

- This theme is still a page 16 story, underappreciated compared to frontpage headlines about AI. Given current price levels, the risk reward is in our favour All this trade needs is time.

- Keyera (1.5%)

- It feels unnatural to say, but Energy has the cleanest balance sheets. Since the Covid crash where Oil prices traded negative, energy companies of transitioned from accumulating debt for capex and exploration, to eliminating the majority of their debt and becoming cash cows. We don’t see a catalyst for oil prices to rise near term, and thus favour mid-streamers

- With Keyera’s recent acquisitions and completion of KAPS project, this should be a synergy for the company to be rerated higher.

Small caps have long underperformed – they stand to benefit from lower short term interest rates

- Kevin Warsh is perceived as a hawk for his preference to reduce FED asset buying and growing their balance sheet. He’s supportive of lowering interest rates. Trump would not be nominating him if it wasn’t crystal clear he’s be lowering rates.

- Theoretically, the result should be a steepening yield curve. Short term rates down, long term rates up.

- This is a tail wind for small caps as they’ve lagged the MAG7 for years. These business are much more sensitive to debt servicing ratios, and lean more heavily to lines of credits rather than 30 year loans.

- Adding 2.5% Fidelity Global Small Caps Opportunity ETF (FCGS)

- Just like favoring Mackenzie EM fund over VEE, or DXMO over stock picking, I’m not a specialist in small caps. There’s 2000 companies on the Russell alone. I’d prefer to pay the managers that have outperformed.

- Alternatively IWM would be the low cost option

- Just like favoring Mackenzie EM fund over VEE, or DXMO over stock picking, I’m not a specialist in small caps. There’s 2000 companies on the Russell alone. I’d prefer to pay the managers that have outperformed.

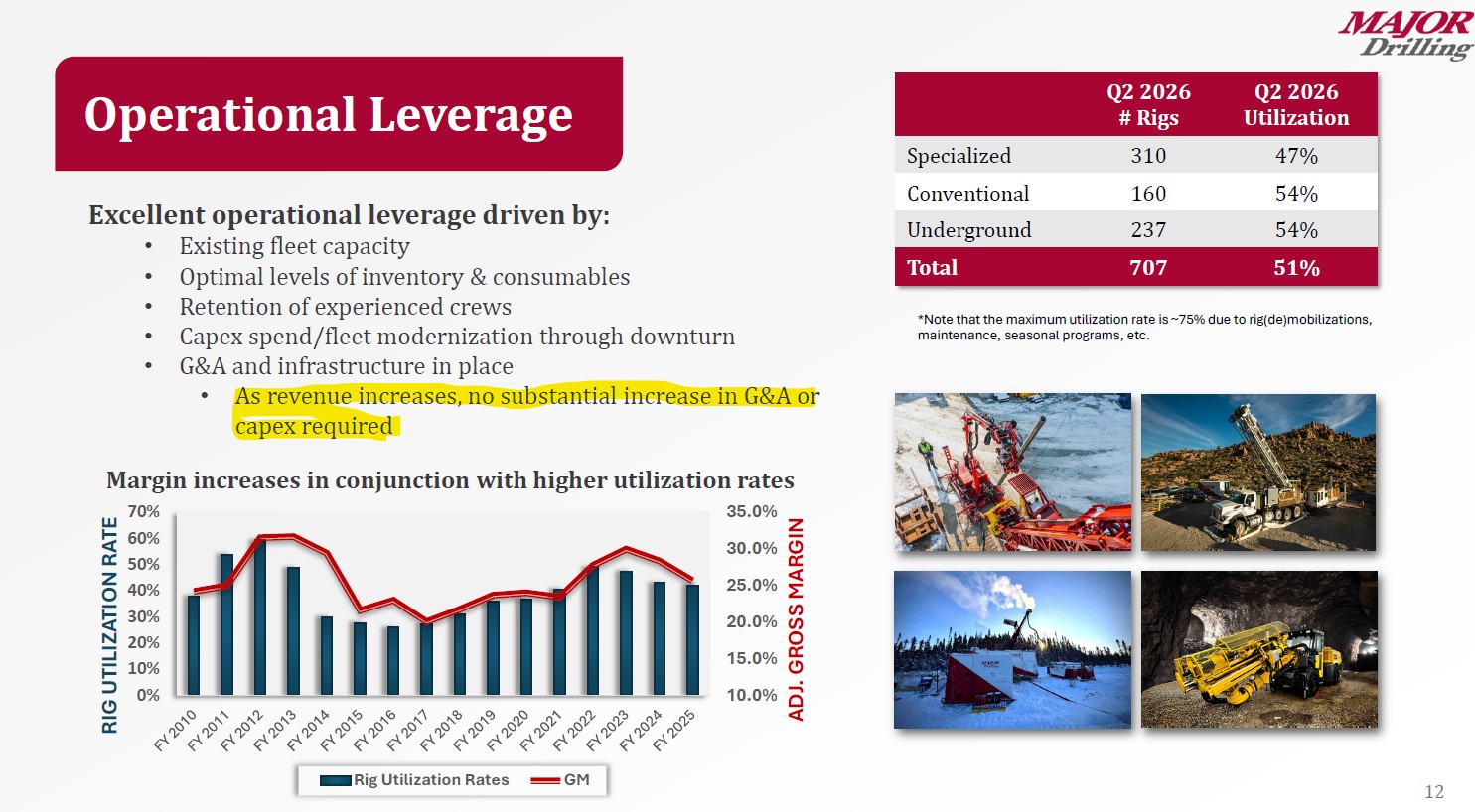

- 1% Major Drilling (MDI)

- Canadian company – largest mineral drilling company in the world

- This is a play on the commodities super cycle, technically MDI is an Industrial company that provides the equipment and services for mineral exploration.

- With the rally in mineral and metals prices, this will encourage more exploration and drilling.

- Attached is their investor presentation – here’s one thing that stuck out to me:

- 1% Volatus Aerospace (FLT)

- They’re a Canadian company that builds drones for defense and commercial purposes. This is a bit different from what I’ve previously held on the focus list. This is a small, small-cap company - very high risk, very high reward.

- After researching this company the past few months, I like them for the following tail winds

- Mark Carney has committed to increase defense spending, focusing on self-sufficiency and partnering with Canadian companies.

- Geopolitics will keep intensifying, with focus on the arctic.

- They are currently working with the Canadian armed forces, training them to operate drones.

- FLT is now starting to show up more and more in my investment research. Attached is a recent RBC conference, you can read a bit of a blurb on them on p.7. They’re currently not covered by RBC.

- I think a small portion of ones total portfolio can be allocated to these type of high risk companies. Revenues are growing, the tailwinds are present, and it’s a great story for the market.

As always, If you have any questions or comments – let me know!

Much love to you and yours,

Lucas