We have long held that the stock market doesn’t march to the president’s drum—or Washington, D.C.’s for that matter. Quite often other factors supersede developments inside the Beltway. And let’s face it, many campaign proposals don’t see the light of day because of the checks and balances built into the system. Yet it’s still useful to consider candidates’ economic proposals given that some presidential decisions can impact the market overall or select industries, even if just for a short time.

Tax plan takeaways

The large tax cuts on individuals, investments, and estates that were implemented in 2018 during Trump’s presidency, known as the Tax Cuts and Jobs Act (TCJA), will expire at the end of 2025. If nothing is done, they will automatically revert to higher levels previously in place.

Trump proposes to extend all of the low tax provisions in the TCJA beyond the year-end 2025 sunset date, regardless of household income, and he wants to cut taxes on Social Security retirement benefits.

Harris seeks to extend the low tax rates for most taxpayers but is in favor of raising taxes on households with incomes above $400,000 per year, and increasing the long-term capital gains tax for those earning $1 million or more. She would boost the TCJA child and small business tax credits and would introduce a new tax credit for certain first-time homebuyers.

The corporate tax rate, which the TCJA cut to 21 percent from 35 percent, does not sunset at the end of 2025—it will stay in place until it is proactively raised or lowered.

Harris advocates raising the corporate tax rate to 28 percent from 21 percent. While Trump had previously called for lowering the corporate rate to at least 20 percent, more recently he proposed reducing it to 15 percent for companies that manufacture goods in the U.S., with some restrictions.

Decoding the impact of tax code changes

Regardless of who is elected president in 2024, the congressional election results will play an important role in determining tax and other fiscal policies.

We don’t think major tax code changes on individuals or corporations are factored into stock market sentiment as of this writing.

We also don’t think a corporate tax rate change is factored into S&P 500 consensus profit margin forecasts, which are currently near the upper end of the range since 1990.

Even so, it’s notable that a Bloomberg study found, “Over the long run there has been essentially zero correlation between the effective corporate tax rate and the performance of the S&P 500 …”

But investors should keep in mind that before we get to the “long run,” the policy debate between the next president and Congress (and lobbyists) about tax rates and other fiscal issues could have a short-term impact on U.S. stock market volatility following the election, including at times during 2025.

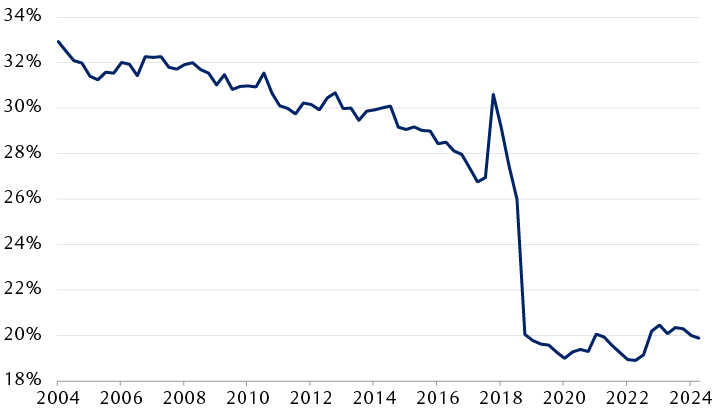

The tax cuts worked

The median tax rate of S&P 500 firms significantly declined after TCJA

The line chart shows the median corporate tax rate of S&P 500 firms from January 2004 through April 2024. Before the Tax Cuts and Jobs Act (TCJA) was passed in late 2017, the median tax rate averaged 30.5%. After the TCJA tax cut was fully implemented by late 2018, the median tax rate averaged 19.7%.

Source - Bloomberg News, “What the data says about actual corporate tax rates: Macro Man” 8/20/24; data represents the median 12-month effective tax rate through 4/30/24

Price plans and populism

Despite the significant decline in the year-over-year consumer inflation rate, the presidential candidates and most voters are still focused on the fact that overall prices remain very elevated.

Harris proposes to tackle high prices by targeting “price gouging.”

We believe any new, comprehensive price gouging legislation would go nowhere in the next session of the Senate and would also struggle to gain support in the House of Representatives, no matter which party wins control of these two congressional chambers.

Nevertheless, we would expect a Harris administration to more aggressively investigate and prosecute federal antitrust and consumer protection cases compared to the Biden administration and previous Trump administration.

Trump’s strategy to bring prices down focuses on incentivizing more domestic oil and natural gas production and energy exports, with the aim of substantially lowering energy and power prices overall, which are key cost inputs of many goods and some services.

Even if this were to dampen global oil and goods prices, we believe some of Trump’s other policies, namely tariff increases, could partly or fully wipe out the benefits that lower energy and power prices would bring.

Talking tariffs

Many of Trump’s tariff policies are more sweeping than those he implemented during his previous term, and they differ greatly from those of Harris.

Trump supports across-the-board tariffs on all imports of 10 percent or more, and high tariffs on Chinese imports of 50 percent or more. He would levy tariffs on goods of U.S.-based companies that are produced overseas and imported into the country, and would use tariffs against domestic companies that outsource American jobs. He has also threatened to use tariffs against countries that trade outside of the U.S. dollar system.

Harris does not support across-the-board tariff increases and views such tariffs as “in effect a national sales tax.” She also does not support significantly raising tariffs on Chinese imports but would likely keep in place the China tariffs and sanctions that Trump and President Joe Biden implemented.

RBC Global Asset Management Inc. Chief Economist Eric Lascelles contends that tariffs “undeniably hurt the country that has tariffs levied against it …” However, he cautions, “Less intuitively, tariffs usually also hurt the country levying them.”

Regulations and red tape

The widespread perception among market participants that Trump is likely to have a more business-friendly regulatory regime than Harris rings true to us, except there are nuances.

While the Biden-Harris administration added 11 percent more “economically significant regulations” in almost 3.5 years than Trump did in his full four-year term, Trump’s administration ended up implementing more regulations than President Barack Obama did in his first term.

We think a Harris administration would implement more proactive and stringent environmental regulations. She would look for opportunities to advance the ball on climate-related issues, whereas Trump stated he would roll back existing climate regulations and targets.

Despite multiple presidential candidates’ pledges to “cut the red tape” in campaign after campaign, a heavy regulatory load on businesses has been the norm for decades. Only a concerted, laser-focused effort on reducing regulations would change this, in our view. For deregulation to work for both the business sector and society, we think a scalpel would be needed rather than a sledgehammer.

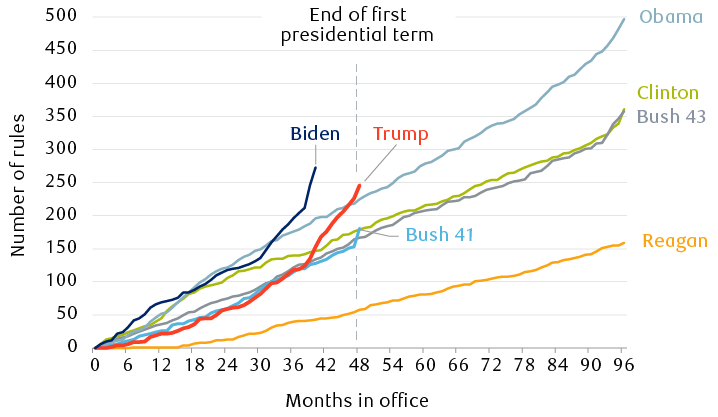

Regulation has increased under every president since Reagan, and accelerated during the last three administrations

Cumulative number of economically significant final rules by administration

The line chart shows the monthly cumulative number of economically significant regulations for each presidential administration since Ronald Reagan. For the two-term presidents, the number of regulations is lowest for Reagan and highest for Barack Obama. George W. Bush and Bill Clinton were roughly in the middle and close together. For one-term presidents, George H.W. Bush was similar to the numbers for Bill Clinton and George W. Bush in their first terms. Under Trump, the number of regulations exceeded Obama’s first term, which to that point had exceeded all of the other presidents. The Biden administration, through slightly over three-and-a-half years, has exceeded the number of regulations created under Trump’s four-year term and all other presidents in their first terms.

Note: “Economically significant final rules,” as defined by the 1996 Congressional Review Act, are rules that result in an annual effect on the economy of $100 million or more, or a major increase in costs and prices, or a significant adverse effect on competition and various economic indicators.

Source - Regulatory Studies Center at The George Washington University; data through 8/5/24

Influence on industries

The candidates have different approaches when it comes to certain industries, but more similar approaches for other industries than is commonly understood.

Banks and financial services: Trump’s regulatory policy proposals and his administration’s approach to mergers and acquisitions within the industry and in general would likely be more favorable than those of Harris. Among other regulations, Harris seeks to limit customer fees.

Oil, natural gas, coal, power, and rare earth minerals: Trump is willing to declare a national emergency to significantly increase domestic energy supplies and exports, and to build out power infrastructure, including to support the growing power needs of artificial intelligence (AI). While Harris no longer supports a fracking ban, we think she would likely impose more stringent regulations on oil, gas, coal, power producers, and mining than Trump.

Clean energy and cleantech: Harris seeks to keep in place and build on the Inflation Reduction Act’s (IRA) unprecedented industry subsidies and incentives. Trump seeks to “rescind all unspent” IRA funds through legislation.

Pharmaceuticals and health care insurers: Harris proposes to add more pharmaceuticals to the Medicare price cap list, building on Biden’s policies. She also wants to extend the price cap list to all Americans, not just retirees in Medicare, and she seeks to permanently cap out-of-pocket drug spending at $2,000 per year for everyone. Trump has previously supported granting Medicare the ability to negotiate prescription drug prices and to level-out prices between the U.S. and other countries. More pharmaceutical pricing restrictions could benefit some health care insurers.

Technology: We believe each candidate would be supportive of the technology industry overall, including AI development, as they understand tech firms are key drivers of innovation and GDP growth. However, both candidates will likely maintain and add more restrictions on tech exports to China, citing national security concerns, which could negatively impact select U.S.-based companies.

Military weapons contractors: Both candidates support significant weapons spending and exporting U.S. weapons to allies and friendly countries. Historically, Republicans have advocated for higher spending levels, but over the years weapons spending has become more of a bipartisan issue as both parties are now dominated by foreign policy hawks.

While candidates’ industry leanings are useful to consider, individual investors should be careful not to jump to conclusions on how stocks of particular industries or sectors might fare depending on who wins the presidential election.

Presidents don’t govern the stock market

Whether Harris or Trump wins in November, we remain convinced that the formal and informal checks and balances built into the government’s structure will constrain the next president from fulfilling her or his full slate of policy goals. Furthermore, other factors will likely play greater roles in shaping the market’s direction such as the natural ebb and flow of the business cycle, the Fed’s monetary policies, and industry innovation.

For individual investors, we think the best investment strategy vis-à-vis elections is to give deference to the long-term investment strategy that is already in place, and to avoid the temptation of making drastic asset class or sector changes based on various election outcome scenarios.

For more on this topic, see the complete report, “Harris and Trump on the issues.”