For most Canadians, their Registered Retirement Savings Plan (RRSP) represents a key source of future retirement income. Understanding how to make the most of your RRSP—and maximize its important tax advantages—is essential to achieving your retirement goals.

What is an RRSP?

An RRSP is a tax-sheltered investment vehicle that provides you with an effective means of saving for retirement. Contributions to an RRSP result in a tax deduction, and the income earned in the plan compounds on a tax-deferred basis. Individuals with RRSP contribution room in Canada may contribute to an RRSP up to the end of the year in which the plan holder reaches age 71.

RRSP-eligible investment options include fixed-income securities, equities, mutual funds, private company shares and more. Additionally, with the elimination of foreign content limits for registered savings plans in 2005, you're now free to invest anywhere in the world.

What are the benefits of RRSP investing?

While most individuals recognize the benefits of investing in an RRSP, many do not exploit its unique advantages to their fullest potential. There are three primary benefits to investing in an RRSP: tax savings, tax-deferred compounding and income splitting.

1. Tax savings

Contributions to an RRSP are deductible for tax purposes within certain prescribed limits. In the year a contribution is made to an RRSP, you can choose to deduct the contribution from your taxable income. This deduction reduces the amount of taxable income and, therefore, the tax payable. The actual tax savings will depend on your marginal tax rate.

The table below outlines both the amount of tax saved and the after-tax cost of a $1,000 RRSP contribution, based on various marginal tax rates.

| Marginal tax rate | Tax saved | After-tax cost |

|---|---|---|

| 25% | $250 | $750 |

| 40% | $400 | $600 |

| 45% | $450 | $650 |

2. Tax-deferred compounding

The most significant opportunity offered by an RRSP is the tax-deferred compounding of income earned within the plan. The term "tax-deferred" refers to the fact that all income earned within the RRSP accumulates tax free until withdrawn.

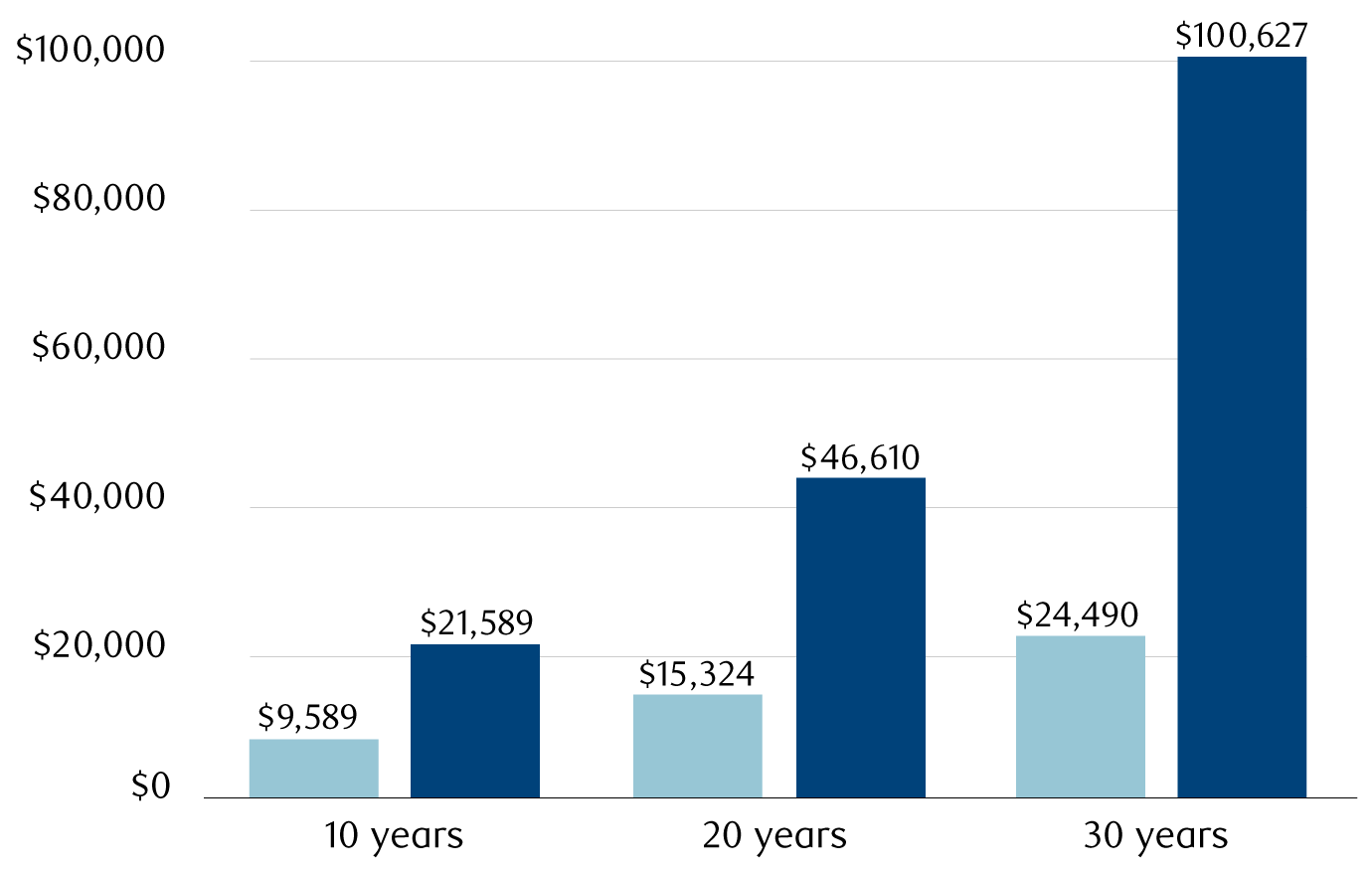

If you have $10,000 to invest and have the choice of making an RRSP contribution or not making an RRSP contribution, consider the chart below, which shows the difference between investing the money inside and outside of an RRSP (i.e., tax-deferred versus taxed). Remember, if you invest the money in an RRSP, you'll save $4,000 in tax (assuming a 40 percent tax rate). Therefore, a $10,000 contribution to the RRSP is comparable to a $6,000 investment outside the RRSP, assuming the tax savings are reinvested.

Tax-deferred compounding (eight percent)

The bar chart shows the differences between investing $10,000 inside an RRSP and $10,000 outside an RRSP, both with a compounding rate of 8%, at 10, 20 and 30 years. At 10 years, the investment is worth $9,589 outside the RRSP and $21,589 inside the RRSP. At 20 years, the investment outside the RRSP is worth $15,324 and inside the RRSP is worth $46,410. And at 30 years, the investment outside the RRSP is worth $24,490 and inside the RRSP is worth $100,627.

Outside RRSP

Inside RRSP

As is evident from the chart, you'd be better off contributing to the RRSP. The question is, how much better?

To determine the RRSP advantage, we have to convert the RRSP value to an after-tax value. To provide this comparison, let's assume you'll withdraw the $21,589 accumulated by the 10th year and pay tax at 40 percent on this income. In the unlikely event the RRSP is actually collapsed in the 10th year, you'd still have earned $3,364 by investing in the RRSP. Allowing the money to remain in the RRSP after the 10th year will further enhance the benefit to you.

3. Income splitting

Utilizing strategies for income-splitting between spouses can provide significant tax savings. One of the most simplistic yet effective methods of income splitting between partners is achieved by contributing to a spousal RRSP. The objective is to provide both parties with similar retirement incomes and therefore similar income tax rates in retirement.

Utilizing the first-time home buyers' RRSP credit

The federal government's Home Buyers' Plan lets you use up to $35,000 of your RRSP savings ($70,000 for a couple) to help finance your down payment on your first home. To qualify, the RRSP funds you're using must be on deposit for at least 90 days. You must also provide a signed agreement to buy or build a qualifying home. The withdrawal is not taxable as long as you repay it within a 15-year period.

For the 2022 and subsequent taxation years, the Federal Budget proposes to increase the amount used to calculate the Home Buyers' Tax Credit ( HBTC) from $5,000 to $10,000. This would provide a tax credit of up to $1,500 to eligible home buyers.

Know your options

An RRSP is one great way to save for the future and provides meaningful tax deductions and tax deferral until you start to withdraw from it. Before contributing to retirement savings accounts, make sure you understand your options.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.