This reality, combined with the still numerous uncertainties about the disease’s toll and duration, has inflicted further damage on the equity market, and disrupted segments of the fixed income and commodity markets. The S&P 500 has fallen nearly 30 percent from its mid-February peak, with other developed equity markets sharply lower as well.

Meanwhile, governments are not only implementing unprecedented restrictions to stem the spread of the disease but also are putting forth aggressive stimulus initiatives—along with major central banks—in an attempt to blunt the economic damage. Following is an assessment of where things stand in this fast-moving crisis from RBC economists and strategists, and the Global Portfolio Advisory Committee.

Stimulating potential?

Markets have yet to respond positively to announced or planned stimulus efforts by major central banks or G7 governments. Are these institutions on the wrong track?

- RBC Capital Markets, LLC Chief U.S. Economist Tom Porcelli argues that the Fed is “not done” stimulating, and the U.S. government is just beginning. He wrote, “Moreover, we maintain, there is a lack of appreciation for some of the fiscal policies that were already floated. This point should not be lost in the noise. Help to the small business community is critical. Overall, we maintain our view that most of the authorities are basically doing the right thing, and once we get beyond the ugly ding to [economic] growth that is coming, policies in place should allow for growth to start the process of healing in the second half [of the year].”

- Porcelli also points out the need for balanced consideration of on-the-ground economic activity. He wrote, “We think while there is a heavy impetus to write off those areas of the economy that are heavily impacted by social separation, there is little credence given to the potential offsets via increased spending n ‘stay-at-home’ goods and services. The situation naturally leads to one of growing pessimism and ‘worst-case-scenarios’ as becoming the base case. But perhaps we are underestimating the ability of companies to adapt.”

Recession realities

Despite being encouraged that authorities seem willing to throw the kitchen sink at this crisis, we’re not Pollyannaish about the economic risks. Because of the sudden, exogenous shock, it is increasingly looking like the coronavirus pandemic could be the first health crisis to cause a recession in developed economies in the modern era.

- Given the significant number of lingering uncertainties associated with the spread of the virus, RBC Global Asset Management Inc. Chief Economist Eric Lascelles believes it’s prudent to evaluate the risks according to three different scenarios: positive, medium, and negative. At this stage, his base-case forecast is that things play out according to the “medium” scenario, which is somewhat more pessimistic than he estimated previously. This scenario assumes a subtraction of one percent to two percent of GDP growth in developed economies for the year. This would result in a recession in Europe (even before the crisis, growth there was weak), slightly positive growth in the U.S., and roughly flat growth in Canada in 2020.

- While it is “still too early to observe significant economic damage in the developed world,” there is downside risk to this “medium” scenario. Lascelles wrote, “… let the record show that even the U.S. and Canada are now more likely than not to suffer technical recessions as their economies decline for two consecutive quarters.”

- Gauging recession risks is more challenging due to the exogenous and swift nature of the coronavirus shock. Normally, our favorite leading economic indicators can pick up weaknesses in the U.S. economy and provide a good sense of when a recession could appear, often six to 12 months ahead of time. However, in this case, traditional data is less useful because developments are unfolding so rapidly, and even the best leading indicators signal with a lag.

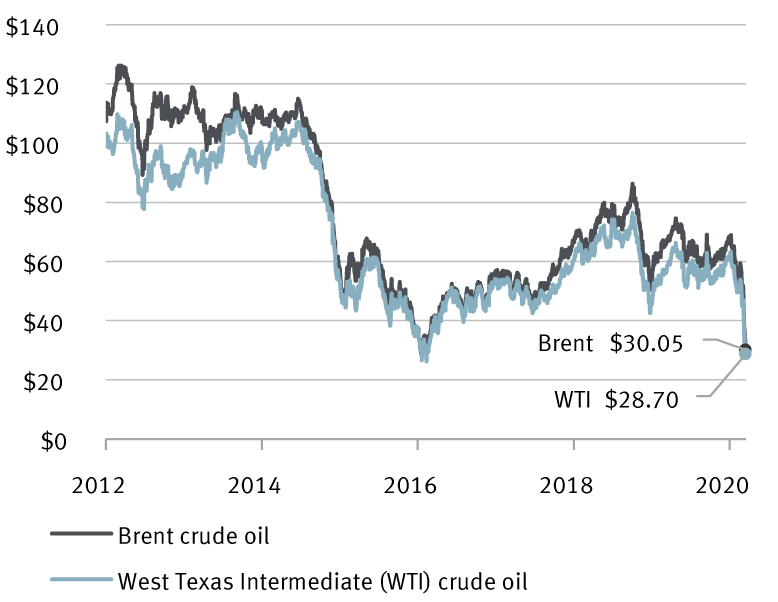

Crude conditions

The crude oil collapse poses additional risks for energy-centric economies and energy sectors of all major oil-producing countries.

Crude oil has plunged and is testing the 2016 lows

Crude oil prices (per barrel)

Source - RBC Wealth Management, Bloomberg; data through 3/16/20

- Regarding the price war between Saudi Arabia and Russia, RBC Capital Markets, LLC Commodity Strategist Michael Tran asks the all-important question, who will blink first? Neither, it will be the U.S. shale industry, he believes.

- President Donald Trump’s plan to fill the strategic petroleum reserve “to the very top” is a constructive development for the oil market as it is equivalent to mopping up 20 days of the excess global supplies, according to Tran. However, he cautioned, “While helpful on the margin, such policy pales in comparison to a coronavirus-plagued [oil] market that is measured in months or a price war that is expected to last several quarters or longer.”

- One of the biggest near-term challenges for the crude oil market that differs from previous shocks is the potential for a severe and sudden decline in gasoline demand, especially in the U.S. It is the world’s largest gas guzzler by far. To put this in context, Tran noted that “the entirety of China could cease driving and that would amount to a demand hit that is softer than if U.S. gasoline demand were curbed by 30 percent.”

Riptides through bond markets

The bond market has not been spared from the volatile market conditions.

- Price discovery has been very challenging for market makers thanks to swings in government bond yields that have been both large and frequent. A notable example of this can be found in the trading activity of the most actively traded U.S. Treasury bonds, as dealers reported bid-offer spreads that were about 10 times wider than normal.

- Trading conditions were even more challenging in the corporate bond market, as corporate bonds have been a popular source of funds. As a result, many corporations have not benefited from the recent move lower in government bond yields, and they have actually seen their cost of debt rise back to mid-2019 levels.

- These unwelcoming conditions have shut down the new issue market, and this has incentivized borrowers to shore up liquidity where they can. To this end, a number of companies reported drawn down bank lines.

Canadian equities and the dollar

- After underperforming global peers amid the recent plunge in oil prices, the S&P/TSX Composite Index is trading at a forward price-to-earnings multiple of 11.4x, compared to 15.1x at the start of the year and its long-term average of 14.5x. Despite a seemingly attractive valuation, we believe investors should maintain a defensive bias as economic risks and the earnings outlook are notably tilted to the downside.

- The uneven representation of sectors in the Canadian market (i.e., Energy and Financials account for roughly 45 percent of the benchmark) brings with it particular challenges. With limited visibility on how the COVID-19 outbreak and the global oil price war might play out, we are mindful of the risk that business activity disruptions could last longer and inflict more durable damage to the Canadian economy than what markets currently anticipate. Furthermore, we fear that the Canadian household sector is ill-prepared to weather an economic downturn in light of elevated debt burdens and a tepid savings rate.

- Balance sheet stability is likely to become the top priority among energy companies and investors alike. Energy companies are already cutting production plans and capital expenditures, with dividend payouts also in the crosshairs.

- The banks remain the most important sector in Canada. It will be in focus as investors gauge the impact of low interest rates, lower overall economic activity, weak energy prices, and the ultimate magnitude of credit losses lurking in bank loan books. Direct oil & gas exposure is less than it was five years ago, but banks may have to contend with more broad-based credit weakness should the economic outlook darken. We remain comfortable that the Canadian banking sector has strong capital positions with which to absorb any future losses. Furthermore, the dividend yields that range from over five percent to over seven percent offer some level of support and should be sustainable under economic scenarios more dire than what we contemplate as our base case. Nevertheless, we believe investors in the sector will need to be patient and able to stomach the kind of volatility that we expect to see through this period of meaningful uncertainty.

- The Canadian dollar has sold off sharply along with the equity market and in particular with the recent fall in energy prices. It may remain under some pressure until more clarity emerges on the outlook for the Canadian economy and the energy industry more specifically.

Profits pressures

Corporate earnings estimates are being reassessed across the board, in all major equity markets. Uncertainty about the spread and duration of the pandemic is making the process more difficult. Here again, employing scenario analysis is useful.

- RBC Capital Markets, LLC Head of U.S. Equity Strategy Lori Calvasina recently lowered her S&P 500 earnings estimate from $174 to $165 per share. This assumes one negative quarter of U.S. GDP growth in Q2, and economic stabilization beginning in Q3. In this scenario, a recession would be avoided, as those contractions typically feature at least two consecutive quarters of negative growth.

- But with economic risks on the rise in the U.S., we think it’s prudent to consider a recession scenario. If this were to occur, Calvasina estimates there would be an additional, meaningful hit to corporate profits. S&P 500 earnings could retrench to $149 per share in 2020, much lower than her $165 non-recession estimate. This harsher scenario would represent an 8.6 percent year-over-year decline in earnings growth compared to the $163 achieved in 2019.

- Markets usually don’t wait around to see whether a recession will materialize before they factor that into stock prices. We think the U.S. and other equity markets have already begun to “price in” (factor in) a recession. This is one of the reasons the declines have been so swift and vicious, in our view. The S&P 500 is already in the “recession zone.” In the 12 U.S. recession periods since the late 1930s, the average and median declines of the S&P 500 during or adjacent to those episodes were 32 percent and 24 percent, respectively. However, there was wide variation among those 12 episodes, with the most moderate decline being only 14 percent and the most severe at 57 percent, the latter of which occurred surrounding the global financial crisis in 2008–2009. During the coronavirus crisis, the S&P 500 has fallen almost 30 percent from its all-time high, which means “the stock market is now baking in a recession,” Calvasina points out.

Darkest before dawn

RBC’s economists and strategists continue to believe this troublesome period for many countries, and markets, is a transitory shock.

- There is no doubt in our minds that some companies are going to face serious hardships through this period and even afterwards—signs of distress among the hardest-hit industries and requests for government assistance are starting to accumulate. But we believe many industries will begin to heal and get back to work after the worst of the virus passes, and some industries will help lead the way out.

- As Lascelles so aptly put it on a recent conference call, equity investors are buying a share of future earnings of companies—not just for the next few months or even the next year. Long-term investors are buying into a multiyear stream of earnings. He does not believe this pandemic will cause a permanent hit to the profits of most companies. Not even the Spanish flu of 1918—a much more deadly pandemic—caused a permanent hit to corporate earnings.

- Calvasina will continue to re-evaluate her U.S. earnings targets as developments surrounding the virus and its economic impact begin to crystallize. She wrote, “For now, we continue to believe that the bulk of the pain in stocks will occur early in the year, with the bulk of the economic impact coming in 2Q/mid-year, and a recovery trade taking hold once the news flow around the coronavirus improves and/or the valuation appeal of stocks becomes more apparent.”

- We believe the massive stimulus efforts by governments and central banks, not to mention the prudent steps that millions around the world are taking to stem the spread of the disease, can go a long way toward mitigating the damage to the economy.

Disclaimer

Non-U.S. Analyst Disclosure: Patrick McAllister and Mikhial Pasic, employees of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc., contributed to the preparation of this publication. These individuals are not registered with or qualified as research analysts with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since they are not associated persons of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

Non-U.S. Analyst Disclosure: Jim Allworth, an employee of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc. contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since he is not an associated person of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.