Key Takeaways:

- When deciding what to during this market reaction, one must look at their portfolio strategy

- Current baseline scenario assumptions are that the previous trend in growth will resume at some point

- Given no certainty on when this outbreak will be contained, it's likely to remain volatile for awhile

A few weeks ago, when the coronavirus started emerging, the belief was that this outbreak will be contained with no large-scale impact on the global economy and that media (and all of us) will be on high-alert. Since that post at the end of January, while the long-term risks haven't increased, there are certain sectors and companies that have become impaired and/or will take longer to recover.

Certainly in our household, that family trip to Europe in the summer: we aren't booking in the next few days (but I am sure we will still go). There is no doubt that the fears have changed behaviour and this effects markets.

So when looking at the situation for my client's portfolios, I wanted to share how I think about these implications:

Four key points:

- What was the economic-earnings trend before the shock for the various companies in the portfolio?

- What stage of the business cycle are these companies in? Is there a real U.S. recession risk?

- How do those assessments translate in terms of asset allocation and portfolio implications?

- Do any of my clients have immediate cash needs?

For now, I am operating under the following assumptions:

- COVID-19 outbreak tapers off by the end of March

- Full factory re-opening in China by the end of March

- Coordinated stimulus led by China and the U.S. in terms of more reductions in interest rates: global coordination like we have seen a few times now in the recent past

- The previous trend in economic growth and earnings to resume post the shock

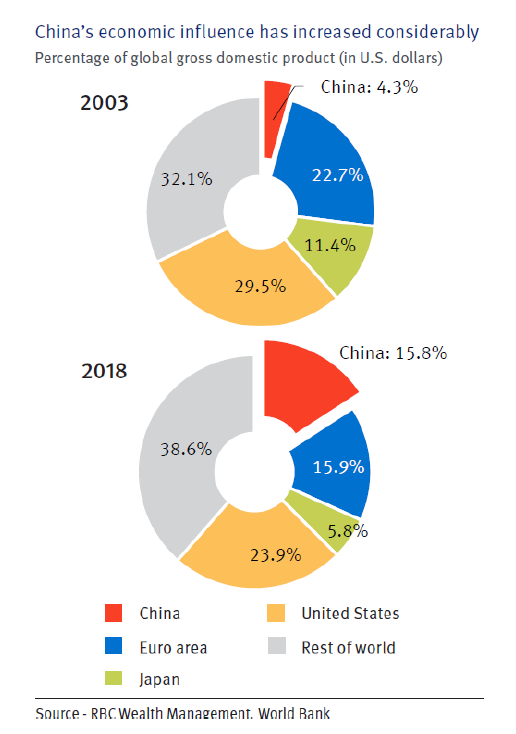

China's importance to the global economy has grown considerably in the last 15 years, so how quickly China recovers will positively influence greatly when the markets stabilize:

Some sectors will recover quicker than others and are better positioned. A downturn is uncomfortable. While no one knows the full extent of the duration or intensity of the virus's impact on the economy, I believe that as with prior major pandemics of SARS (2002/03) and H1N1 (2009), this too will be a manageable and transitory event. While the client's long-term objectives shouldn't change, this does present opportunities to make some tactical changes to asset-class allocation and individual securities.

Perhaps we can blame this volatility on this year being a leap year. An old Scottish expression: "leap year was ne'er a good sheep year." The superstition is that Leap Days are particularly unlucky to have been held through history and across cultures. Rome burned in 64, and the Titanic sank in 1912 (both leap years). This leap year, on Saturday the 29th, our friends in the U.S. are holding the Democratic 2020 South Carolina Primary. I predict that Biden will win, a temporary respite from the Bernie Saunders momentum. Some indeed believe a Saunders Democrat president would be analogous to a Titanic sinking for the markets. Stay tuned for commentary on the Democrats nomination process, as it unfolds in the next few weeks, and how the markets might judge different outcomes.