While management buyouts are often more successful than passing the business to family members or third parties, this may not be the case for all industries and businesses. Owners of businesses employing family members often place significant importance on keeping the business in the family compared to owners of businesses not employing family members. This is particularly so for agriculturally based businesses. Many small and medium sized enterprise owners employ at least one family member, and statistically, family businesses often play a bigger role in local communities, place greater emphasis on customer loyalty and foster a culture of shared values. This may allow for a successful and smoother transition.

There are a number of challenges unique to running a family business and planning its future. Consider the interaction of family, business and ownership values and interests. There are long-standing relationships between family members that will still be there long after the transition, so don’t overlook family dynamics. Is there a suitable successor within the family, and if so, can they work with others in the family who may also be involved in the business?

The high failure rate of intergenerational business transfers can be attributed to a combination of factors. These include the lack of a formal succession plan, a tendency to leave succession planning too late and the absence of clear communication. When you involve family members and discuss their concerns, such open communication helps clarify expectations of everyone’s roles and commitment to make the transition a success. Don’t assume that you understand the needs and perspectives of your relatives and employees. Address potential issues, perhaps by means of a family council, rather than avoiding them.

Owners of family businesses often assume they are “on the same page” as their chosen successors. This may be one reason why they are less likely to have a formal succession plan than those selling the business outside the family. It’s a risk to assume that one of your children or another family member wants to take over the business. They may have other plans. When you have identified a successor, involve them in your succession plan and share your long-term goals with them, your family and key employees. Their input can minimize potential conflict and help maintain stability in the business and the family.

Don’t underestimate the value of starting the process early. If you start to design your succession plan many years ahead of your expected exit date, you can build the interest of potential successors within the family by involving them in meetings and asking for their input. This can help them make an informed decision about whether they want to participate and to what extent.

If you don’t have one family successor in mind yet, consider splitting the business and its responsibilities between family members. Who has been actively involved in the business and shown an aptitude and desire for leadership? Given the differing levels of commitment that your children may have shown, should you divide the business equity equally between them? The business may be your largest asset. Can you recognize their contributions in other ways and is it appropriate for children who are not actively involved in the business to be shareholders?

Obtain professional advice from your legal advisor, tax specialist and possibly a family business facilitator. A facilitator can help you discuss issues with family members, provide objectivity, find constructive ways to resolve conflicts, review plans, establish priorities and involve stakeholders in the succession process.

Will you have an ongoing role after the transition, perhaps in an advisory capacity? This is common among entrepreneurs. The longer they have been in control, the more personally attached they are and the more likely they will want to stay involved. This can gradually reduce the business’s dependence on you and may make it easier to separate your identity from the business role you’ve held for so long. It can also help you gradually transition into retirement.

Incorporate personal planning considerations into your succession plan. Have you prepared a Will and a Power of Attorney/Mandate? Who will run the business if you become incapable of doing so or pass away before the transition? Should you have a buy/sell agreement in place? Your tax planning may also include discussion of family trusts, estate freezes and structuring your business succession to maximize the capital gains exemption.

Business owners who implement a succession plan well in advance report significant benefits. The business enjoys improved financial stability as it moves through a well-planned and managed transition, and relationships with employees and family members also benefit. A large percentage of business owners feel that a succession plan has helped them provide for their family’s future, and many report that they have been able to minimize their future tax liability and improve their business’s financial stability. Those who acquired their business through succession agreed that succession planning yielded significant benefits and helped prepare them for their future as a business owner.

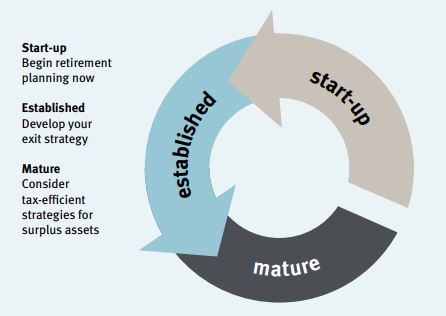

What will you do once you’ve retired?

If you should ever think of retiring from your business, like many successful business owners, you may need help with retirement and tax planning matters. If your work has consumed much of your daily activities, the transition from this busy and demanding working life into retirement can be a challenge.

Give some thought as to how you and your spouse will spend your time in retirement and develop a plan to ensure that your new life will be fulfilling. This doesn't necessarily mean leisure and recreation. You could have an ongoing role in the business, become involved in a new one or work with a charity, non-profit organization or in the community.

Retirement planning requires you to consider a whole new lifestyle with new priorities and perspectives. A common misconception about retirement planning is the idea that money is the most important element and that you should focus your planning on creating after-tax cash flow. There are many other essential factors to consider.

Build an estate plan

If your business interests represent a significant part of your estate, have you thought about how the transfer of this wealth will affect you, your family, your relationships and your personal legacy? Family members may have played different roles in the business. Consider these differences when planning your estate and deciding how you will treat active and non-active family members; for example, equal versus fair treatment. In considering what income you will need, remember to provide for possible unplanned events. Try to be proactive in planning for an unforeseen event, such as a health crisis, and do your planning well in advance of your potential retirement date. Ensure you review your Will and Power of Attorney/Mandate on a regular basis so they continue to meet your estate planning objectives.

What are your plans after you exit your business?

As a business owner, the demands of running a successful business keep you very busy and engaged. Have you thought about how you want to spend your time after you retire? You may have a succession plan for your business, but do you have a plan to help ease the personal transition as well? It is a good idea to develop fulfilling new hobbies and interests while you’re still working. You have left your mark on a successful business. Now you have an opportunity to leave your mark on your community and other areas of interest that are important to you.

Discuss your personal goals with your family and friends if possible. Working together to plan for the next phase of your life can be beneficial for everyone. If you have a spouse who has not been involved in the business, their transition may be different from yours. Remember to include them and develop a post-retirement plan together. This should include fine-tuning your personal finances for the last few years before you retire to ensure you’re in good financial shape to proceed with your plans after you exit the business. Establishing clear personal goals will make this process simpler.

Financial considerations

There are a number of financial factors to consider as you plan your retirement. Tax and estate planning should be ongoing considerations throughout your working life to ensure that your plan continues to reflect your changing circumstances and is still on track to help you achieve your retirement goals. As a business owner, however, in addition to assessing your sources of retirement income, you will need to review your succession plan periodically to ensure that the projected proceeds from the sale or transfer of your business will last as long as your retirement does. It can be difficult to replace an income stream in later years. Remember to factor in the effect of inflation and consider strategies that can increase the value of the funds you will receive from the sale, well before your planned retirement date.

What are your sources of retirement income and when will they be available?

It’s important to understand your sources of retirement income and how much recurring income will be produced by these and by existing income sources. These could include the CPP/QPP, OAS, RRSPs, proceeds from the sale of the business, income from an ongoing interest in the business, income from a new business, an IPP or an RCA.

Consider how to manage these sources of retirement income to maximize their efficiency. Where will you obtain funds if you have a cash flow shortfall? A common strategy is to withdraw funds from non-registered investments before redeeming funds held in tax-sheltered plans. This ensures you continue to defer paying tax on registered investments and preserves the power of tax-free compounding as long as possible.

We can help you decide how to draw on your various sources of retirement income in the most efficient manner to minimize tax, maximize flexibility and make the most of the available tax credits. We can also help you identify the issues that are relevant for your situation and keep your long-term financial plan on track.

Plan your retirement early

Will you need all the proceeds from the sale of the business to fund your retirement? Ensure your succession plan has taken this factor into account. How will you convert the funds received from the sale into an income stream so it’s available for you in retirement?

If you are transferring the business to family members, perhaps for little or no cost, your planning should incorporate this and the need to ensure that there will either be sufficient income from the business to meet everyone’s needs or that other sources of income will be available.

At the Opheim Wealth Management Group we can help you design your financial plan, maximize your after-tax income streams and help you estimate how much wealth you will need for retirement. This will also help you determine whether you will have any surplus and, if so, how much. If there is a significant surplus, we can help you plan the transfer of this wealth to your intended beneficiaries in the most appropriate and tax-efficient manner.

Special tax rules for farmers and fishermen

Tax-deferred transfers to family members

If you own certain qualified farm or fishing property located in Canada that you use directly for your farming or fishing business, you may be able to transfer the property to your children on a tax-deferred basis during your lifetime, or when your estate is settled. This also applies when a family corporation or an interest in a family partnership is transferred from a parent to their child.

If your business qualifies for a tax deferred transfer at the time of death or if you choose to transfer it during your lifetime, you may be able to postpone the payment of tax on any taxable capital gain until the child sells the property. You can also transfer such business property to your spouse or common-law partner during your lifetime and potentially postpone payment of tax on capital gains until your spouse decides to sell.

The capital gains exemption

A capital gains exemption may be available on the sale of your qualifying farm or fishing property, subject to some conditions. If your business meets the “ownership and usage” criteria, you may be eligible for the exemption. If you have previously claimed the exemption on a disposition of qualified property, the amount you claimed will reduce the amount of exemption available on the sale or transfer of your farm or fishing property.

If you transfer the property to a qualifying family member at its fair market value or at less than fair market value, there may be an opportunity to multiply the use of the capital gains exemption. Talk to your professional legal and tax advisors to determine whether these opportunities could work for you and your business.

Who will inherit/purchase the family business?

When deciding who will inherit your family farming or fishing business, there are many factors to consider. The choices you make can determine how the business will prosper in the years ahead, so take some time for discussions with family members. A large percentage of agricultural businesses consider it important to keep the business in the family, but relatively few family businesses survive to the second generation.

Do you intend to retire from the business and pass it on to the next generation during your lifetime, or on your death? If one of your children/ grandchildren is to take over the business, ask yourself whether they have the business acumen, experience or desire to do so successfully. If there are several children in the family, are any other children likely to be involved in the ongoing ownership and management of the business, and, if not, are you making other arrangements for these children?

Have other family members made a commitment to the business, financial or otherwise, or a contribution that you should recognize?

Determining what is fair

Treating your children fairly does not necessarily require that you provide each of them with an identical inheritance. If only one of your children will inherit the business, and there are insufficient funds to provide an equivalent-sized inheritance to your other children, try to structure a division of property that is fair to everyone.

If there are children who are not involved in the farming/fishing business, have you already provided gifts to these children? For example, have you funded their university education? Can they inherit nonbusiness assets? If any of them already hold an interest in the business, have you provided for this in the transfer arrangements? In some cases you may be able to structure more equivalent sized inheritances for each of your children through the use of life insurance policies.

Depending on the circumstances, you may wish to transfer to the farming or fishing child only those assets that are essential for the economic viability of the business. To ensure the transfer is fair to all your children, consider the resale value of the assets transferred, the profit your business successor is likely to make and the contribution that person may have already made to the business.

Is the business profitable enough to support more than one household?

When you transfer the business during your lifetime, remember to take into account the financial position of all the households involved. If you are to receive a lump-sum capital payment, when will it be paid and will it involve indebtedness for the transferee household? What level of debt repayment can they tolerate and what rate of debt repayment can you accept that will provide you with adequate retirement income? Consider your household’s lifestyle needs and retirement goals and factor in any financial commitments you have made to any children in the family, other than those you have transferred the business to.

Think about the transition period

Will you retain control of the business for a period of time? Consider the structure of the new business, for example, a partnership or a corporation. Will you continue to be involved, perhaps as a manager, and, if so, for how long? Give some thought as to how responsibilities will be divided in the new business. There may be matrimonial circumstances affecting the children who are taking over the business. Are there safeguards in place to prevent the family business from being adversely affected by a matrimonial dispute or marriage breakdown?

We can help you collect the information you will need in the decision-making process and review the critical issues of the business transfer to ensure your retirement goals remain on track. We can also work with you to invest the proceeds of sale in a manner that’s consistent with your needs and goals and, if necessary, act as an objective third party to help you identify issues that may need to be addressed.

Ask us how this kind of succession planning could work for your business.

Incorporating your professional practice

There are significant differences between a professional corporation and other corporations.

If you are a professional such as a doctor, dentist, lawyer or accountant, you might consider the advantages of incorporating your practice if you haven’t already done so. Incorporation is permitted by certain professional regulatory bodies, and may provide potential tax savings and tax-deferral benefits. It may also enable you to take advantage of enhanced retirement plans such as IPPs or RCAs.

Characteristics of professional corporations

There are significant differences between a professional corporation and other corporations. A professional corporation is generally subject to the rules and guidelines of the regulatory body governing its profession. These include restrictions on the name of the professional corporation and who may be named as a voting shareholder. For example, in some provinces and territories, only members of the same profession can be voting shareholders of a professional corporation. Generally, the officers and directors of the corporation must also be voting shareholders. Before deciding to incorporate your practice, make sure you understand the regulatory guidelines applying to your profession in your province/territory.

Advantages of professional incorporation

There are a number of potential benefits to incorporating your professional practice. You may be able to:

-

Enjoy potential tax savings due to the reduced federal and provincial/ territorial corporate tax rate that applies to active business income

-

Benefit from the tax-deferral opportunities of the corporate taxation structure and use the additional funds in the corporation to pay off debt, purchase capital assets, acquire investments or fund an insurance policy

-

Take advantage of the capital gains exemption available on the sale of shares of a professional corporation, provided certain conditions are met

-

Achieve potential tax savings through a number of income splitting strategies, depending on your province/territory of residence

-

Limit your commercial liability to trade creditors

-

Choose from flexible remuneration options depending on your province/territory of residence

Planning for retirement

Professional incorporation provides retirement benefits not available to sole proprietors or partnerships, including the ability to establish IPPs and RCAs. These retirement savings vehicles can greatly enhance your retirement benefits and potentially provide creditor protection.

Considerations

In addition to the many advantages offered by professional incorporation, there are some considerations to bear in mind. The costs of establishing and maintaining a professional corporation can be higher than those of a sole proprietorship. There are greater tax filing and compliance obligations. You can’t use business losses to offset your income from other sources. And you may also have to pay a health tax levy when your corporate payroll exceeds a certain level (depending on the province/territory).

Creditor protection

If you decide to incorporate, you should also keep in mind that a professional corporation can only protect you against business creditors and not personal liability for professional negligence. Consider investing in malpractice insurance and other creditor protection strategies such as setting up an IPP inside the corporation.

We can help you implement several strategies made possible by professional incorporation, including IPPs and RCAs. Please contact us for more information. Business planning quick tip

There are several strategies incorporated professionals can consider to reduce taxes. However, there is at least one tax strategy available to unincorporated professionals – “cash damming”. With cash damming, you convert the interest on your personal debts to a tax-deductible business expense by using the revenue from your business to pay off your personal debts. You then use a separate line of credit or other loan facility exclusively to pay your business expenses. If you would like to learn more about how this strategy works, please ask us for more information.