It is hard to believe that 2024 is here! With the start of a new year comes new room to contribute to your Tax-Free Savings Account (TFSA). A TFSA is an extremely powerful account as it allows your savings to be invested, grow, and be withdrawn – all tax free.

The government of Canada first introduced the TFSA in 2009, with the initial contribution allowance of only $5,000. If you were of age to contribute to a TFSA in 2009, the cumulative contribution amount now totals $95,000, with the annual contribution limit being $7,000 for 2024. Over the years, TFSAs have grown substantially due to the combination of consistent annual savings and the power of compounding.

| TFSA Contribution Room | ||

| Years | Annual Limit | Cumulative Total |

| 2009-2012 | $5,000 | $20,000 |

| 2013-2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016-2018 | $5,500 | $57,500 |

| 2019-2022 | $6,000 | $81,500 |

| 2023 | $6,500 | $88,000 |

| 2024 | $7,000 | $95,000 |

We cannot stress enough the importance of utilizing a TFSA. Here are five key benefits:

-

Tax-free income and growth: Any income (including capital gains) earned in a TFSA is exempt from tax. This feature allows your savings to grow and compound at a faster rate.

-

Tax-free withdrawals: You can make tax-free withdrawals from your TFSA, and the withdrawal amount is added to your contribution room in the following year. Since the withdrawal does not go into income, it has no impact on federal income-tested benefits or credits (such as the Guaranteed Income Supplement, Child Tax Benefit, Old Age Security, etc.).

-

Designating a successor holder or beneficiary: When naming your spouse as the successor holder of your TFSA, your spouse automatically becomes the holder of your account at your time of death, and the TFSA continues to exist and grow tax free without affecting their contribution limit. When designating a beneficiary, the beneficiary will receive the funds completely tax free. Not only will your beneficiary(ies) benefit, by making a designation on the plan documentation, it will simplify the administration of your estate for your executor and reduce probate taxes.

-

No upper age restriction on contributions: You can contribute to a TFSA as long as you are age of majority and a resident of Canada. You are entitled to make the annual maximum contribution amount up until your date of death.

-

Unused contribution room can be carried forward: If you contribute less than your annual contribution limit, you can carry forward any unused contribution room indefinitely.

It is important to use your TFSA effectively to reap these benefits. Although it is called a Tax-Free “Savings” Account, you can have your savings work for you and grow by investing within your TFSA. The qualifying investments you’re permitted to hold in your TFSA include (but are not limited to): cash, mutual funds, securities listed on a designated stock exchange, Guaranteed Investment Certificates (GICs), bonds, etc.

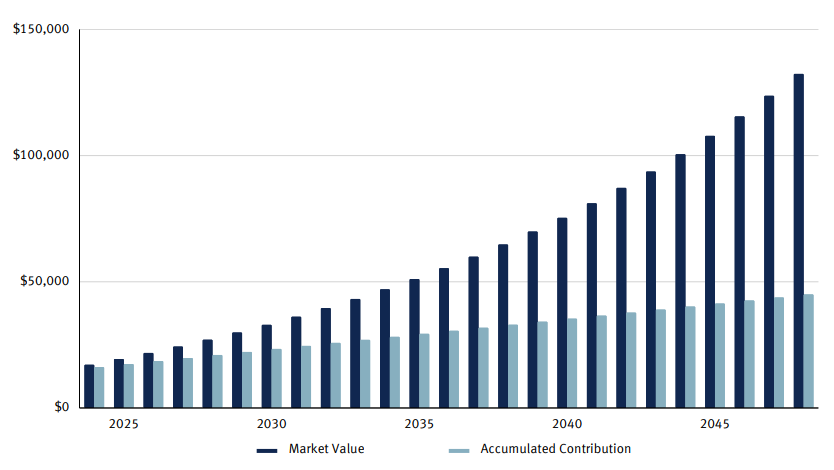

The power of compounding is quite staggering. If you made a onetime contribution of $7,000 to your TFSA in 2024, and made a $100 contribution every month thereafter for 25 years, you would have contributed a total amount of $45,000. If you had invested your consistent savings and it was growing at a rate of return of 6.00%, at the end of those 25 years, your TFSA would be worth $132,355. Now think about how much money you would have if you contributed and invested the maximum contribution amount to your TFSA every year.

It is important to be aware of how you are investing your hard-earned savings and the rate of return you are receiving. If your investments are not growing, then you won't fully benefit from what the TFSA has to offer. By owning great quality, dividend-paying stocks, you can create a growing income within your TFSA. No matter if the price of the dividend paying stock is up or down, the growing dividends provide you with an income. With this growing income, you may never need to touch your capital which can be passed to your beneficiary(ies) tax-free upon your passing.

If you could benefit from our services and would like to discuss TFSAs, please do not hesitate to give us a call. We would love to help in any way we can!

"How will you replace your current income in retirement?"™ - Jim Seyers