Interest rates have been trending downward for the last 40 years, and with the most recent two emergency rate cuts, the Fed Funds Rate now hovers around zero. This month, a debate has begun as to whether negative interest rates will be seen in North America. Although Fed Chairman Jerome Powell has recently shot down any such rumours by claiming that the policy was “not something [they’re] looking at,” President Trump has been pushing for negative rates for quite some time and has said that he “feel[s] strongly we should have negative rates.”

What are negative interest rates?

Negative interest rates are exactly how they sound: an interest rate below zero. This is typically a consequence of unconventional monetary policy, as central banks attempt to prop up a stagnating economy. If the Federal Funds Rate were to drop below zero, borrowers can essentially take out loans for free, or even get paid to do so. The purpose of this is to encourage borrowing and investing, in lieu of saving. Although, the Fed prefers to provide aid and stimulus through a 'quantitative easing' program, some like Zach Pandl, Head of Strategy at Goldman Sachs, believes a second wave of COVID could prompt the Fed to reconsider cutting rates into negative territory.

This concept may seem foreign to North Americans, however, the Eurozone has been running at negative interest rates since 2014. Tom Porcelli, Chief Economist of RBC CM, does not believe the negative interest rate policy has worked to restart their economy. In his view, lower interest rates had little impact on a region that faces the fundamental problems of a declining working population and stagnant productivity growth. These growth constraints lead to a lack of viable investments whose demand is not impacted from a decrease in the cost of credit.

Bond Markets Signaling

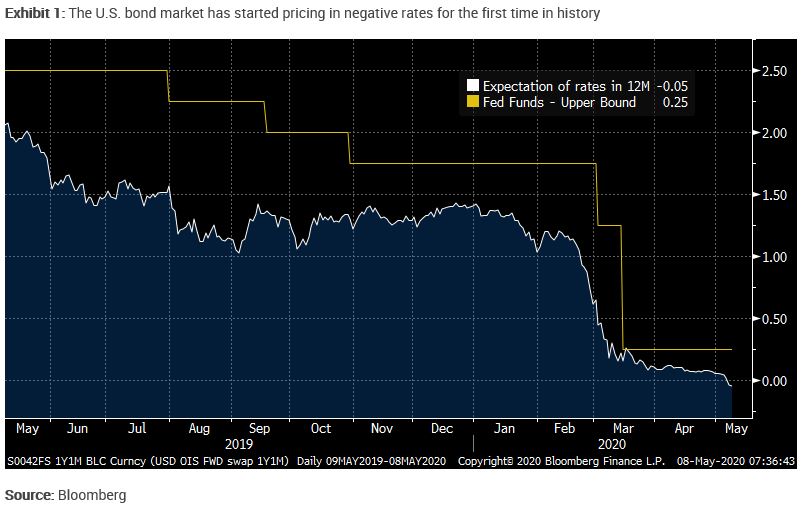

The bond markets have begun to price in negative interest rates for the first time in history. This can be seen in the overnight index swaps market, commonly known as “OIS”. This market is showing a negative reading for interest rates in twelve months. The white line in Exhibit 1 tracks these expectations, while the yellow line measures the current Fed Funds rate.

However, if you zoom out (Exhibit 2) you can see that the bond market has not always been correct in predicting rates over the past cycle. The bond market was wrong coming out of the last recession, predicting that rates would rise when they actually stayed at the zero lower bound (0-0.25%) for ~7 years. The market was also incorrect in 2018 when it priced in the expectation that the Fed would keep hiking rates. This is all to say that negative interest rates are not guaranteed.

What should investors do if there are negative rates?

A yield curve that moves into negative territory is the only way that government bonds make meaningful capital gains from here. At the time of this writing, the 10-year U.S. treasury yields 0.63%. If its yield declined to 0% the bond price would rise by approximately ~5.70% (0.63% x ~9yrs duration). The reverse would happen if rates rose, however, we do not see this as an immediate risk. This should reinforce the idea that gains may be limited in government bonds as it requires a heavy fall in rates that is currently unwanted by the Fed. These bonds, however, should continue to provide ballast to a portfolio during volatile times.

If rates are negative, it can be challenging to hold bonds through passive indexing ETFs. These indexes will inevitably hold the negative yielding bonds which may detract from yield and income distribution. Rather, using actively managed fixed income products may be preferred for volatility management and total return by rebalancing between high yield and investment grade credit. For those who prefer a risk-averse passive strategy, a diversified GIC ladder can be considered, as investors can currently earn a return that is higher than a government bond.

Finally, negative yielding fixed income securities could also encourage investors to flock to riskier equity investments in search of greater dividends and return. Dividend-paying blue-chip stocks with healthy balance sheets and free cash flow could become benefactors of investment flows. However, a lower or negative interest rate environment will also increase the stock market’s price multiple and valuations of stocks, which need to be cautiously monitored.

North America has never faced negative interest rates so investors cannot rely on history books for guidance. How the sentiment of investors, businesses and consumers can change in response to the reality of negative rates is also hard to predict. This is all to say, another potential layer of uncertainty is brewing for investors and although negative rates are not present today, the bond market is telling us something and we should tune our ears to it.