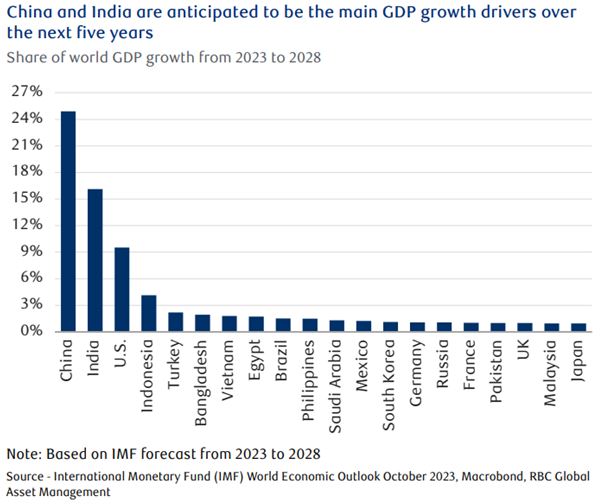

The Global Election Wave 2024 will mark the biggest Global election cycle in history. More than half of the world’s population will vote. The implications for this are profound, as the emerging economies affected are anticipated to drive over 60 percent of Global GDP growth over the next few years. For more details, please see the full article:

Mobile-friendly link

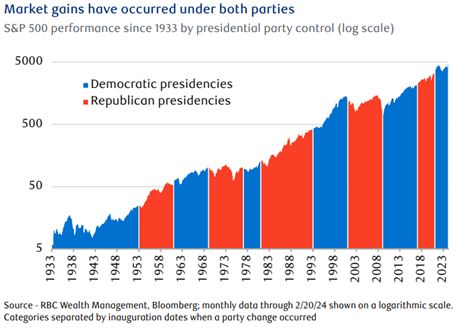

The Economy over Politics On our view of historical trends, Federal reserve policy, economic dynamics, innovation, and earnings growth have a substantially more significant impact on investment performance when viewed against the influence of political developments. For more details on the markets during election years, please see the full article:

Mobile-friendly link

A Soft Landing? Much has been written of where we are in our economic cycle, and similarly in the stock market. We acknowledge that deep market downturns are often accompanied by several factors we do not see today. Notably, overly optimistic investor sentiment and market breadth – whether most stocks are moving up together as opposed to only a few leaders. RBC’s Chief Economist Eric Lascelles has commensurately adjusted the probably of a U.S. economic soft landing to 60%.

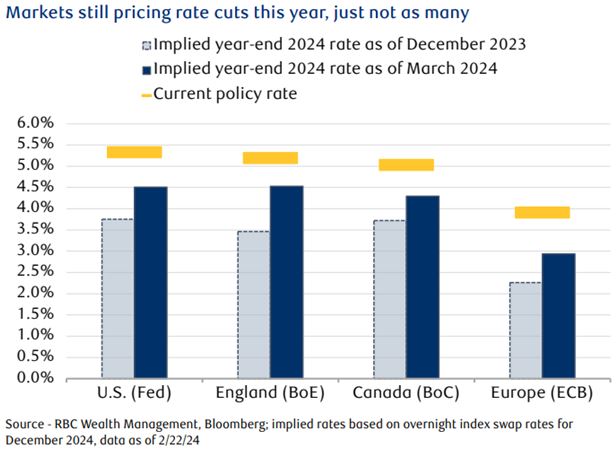

Rate Cut Projections Despite the volatility of rate expectations, we maintain our outlook for a gradual easing of inflationary pressures. The Federal Reserve’s cautious approach aligns with our view that the first rate cuts will begin by this summer.

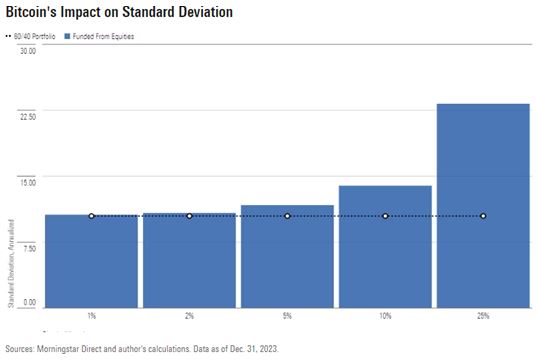

How much Bitcoin is too much? As per Morningstar, (see chart below from Morningstar): “The sources of risk for a 60/40 portfolio can be deceiving. It’s easy to assume that 60% of the portfolio’s risk comes from equities and 40% from bonds. However, it is more like 85% of the portfolio’s risk comes from equities because they are more volatile than bonds. In light of this, adding bitcoin, which is much more volatile, can dramatically shift a portfolio’s risk profile. A small dose of 1% or 2% bitcoin doesn’t have a big impact on a 60/40 (balanced) portfolio. At these levels, bitcoin contributes roughly 3% and 7% of total risk, respectively, and results in a minimal change to overall volatility. While a little bitcoin can go a long way, it is at greater exposures where investors will see the largest shifts in the total risk toward bitcoin. At 5%, the bitcoin allocation contributes over 20% of the portfolio’s total risk and produces a volatility that’s roughly 16% over the 60/40 portfolio. A 10% allocation increases volatility by 41%. With a 25% allocation, the contribution to risk leaps to 83% when sourced from equities. The overall volatility is more than double that of the 60/40 portfolio. This should serve as a warning to investors that even a small amount could disproportionately increase the volatility of the portfolio, therefore changing the risk composition.”

You can enjoy the complete RBC Wealth Management report in PDF format here: Global Insight

Please feel free to contact us with questions and to discuss your investments.

We appreciate the opportunity to support your financial journey, and look forward to helping you accomplish your long-term goals.