“You get recessions, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready. You won’t do well in the markets.” – Peter Lynch, Fidelity investing legend

It is that time of year when Bay Street and Wall Street roll out the predictions. The truth is, it’s hard to predict things a year out. Just look at the past three years. So let’s have a discussion in more broad terms about where we are at, and where we may be going.

The new year always feels like it is supposed to be a time for fresh starts, a time of enthusiasm for the forthcoming year, resolutions to be / get better, a chance to try something different. But if we will be starting something anew, logically, it suggests we are finished with something old.

Despite the fact the calendar may have flipped, however, we are nowhere near done with what we started with in 2022. The fact that inflation remains “sticky” keeps the central banks in a “hawkish” tone. Markets have been locked in a tight trading range for the better part of the past year, and investors remain searching for clues that either confirm or deny that a recession is looming. One way or another, many of the items causing investor anxiety should get answered in 2023.

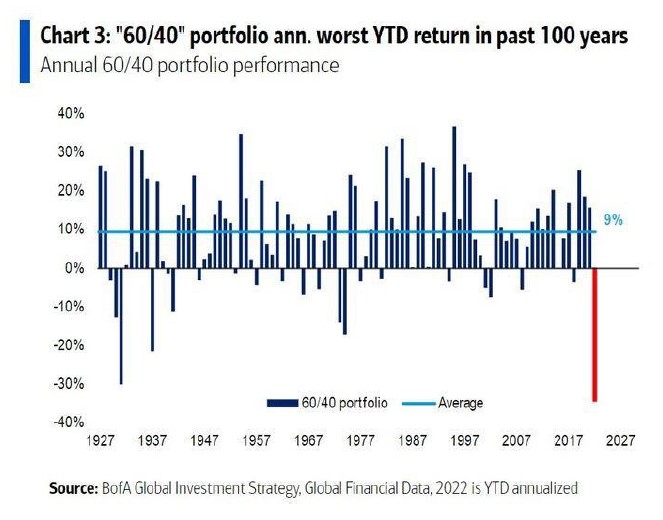

First a quick look back. Last year resulted in only the fifth year since 1928 when both stocks and bonds were negative. That is only five times out of 94 occurrences. Yep, it’s rare.

For many years, the 60/40 portfolio represented the optimal well-balanced portfolio. It’s not that this asset mix in a portfolio performed the best, but rather that it performed the best relative to its volatility over time. According to exchange-traded fund (ETF) giant Vanguard, the 60/40 portfolio has gained an average of 8.8% per year for nearly 100 years. Owning that portfolio meant you could sleep at night for most of market history.

Until 2022, that is.

In normal times, stocks and bonds move in opposite directions, which has meant the 60/40 portfolio had the right combination of the two. Thanks to inflation and higher interest rates, both stocks and bonds moved lower for the bulk of the past year. The fact that a 60/40 balanced portfolio had its worst performance in history in 2022, adds to the anxiety. The negative view is that nothing worked in 2022 except cash and energy. Diversification failed, people’s net worth fell, and markets seemed broken. On the other side of the coin, one could argue the bulk of the interest rate increases are behind us, excess speculation and froth has been shaken out, cash pays decent yields to wait, bonds are more attractively priced than they’ve been in decades, and markets are better priced than they have been in a while. Statistically, having two tough back-to-back years is slim. We will lean toward our inclination that we are rapidly approaching a longer term inflection point in the markets.

The past year was one of trying to call peaks: Peak inflation, peak yields, peak Fed, peak oil, peak bearishness, and yes, peak uncertainty. I would guess most of those are now in the rear-view mirror.

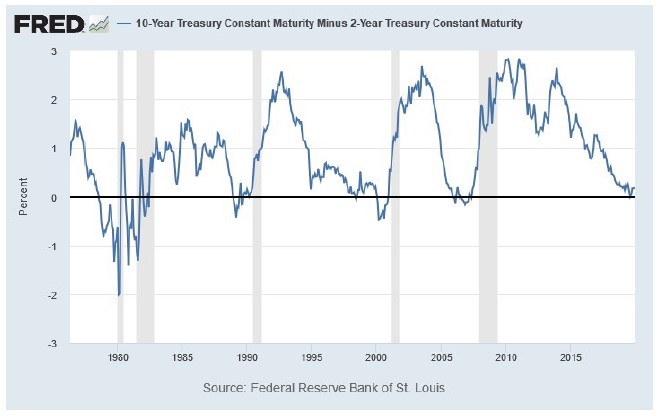

When looking at the business cycles over time, they do repeat. Right now, we are ticking a lot of the boxes that say we are getting into the “late-cycle” phase. That peak expansion we experienced in 2022 after the printing presses of COVID-19, followed by rising inflation, followed by monetary tightening to control that inflation, a flat and /or inverted yield curve, and the decline in cyclical indicators (like housing, now the labour market)…one by one…they are showing up….

The main (and best in our opinion) indicator in the past has been the bond markets, and they are screaming late cycle with curve inversions all over the place.

(Source: FRED Charts https://research.stlouisfed.org/publications/yield-curve/ )

We think the bond markets have it right, and most economic indicators seem to reinforce the message: We are late cycle, and to get back to a new early cycle, we are probably going into some form of recession. Bottom line is we can’t have it both ways: we can’t expect inflation to come down by way of crushing demand without seeing collateral damage to consumer spending. To that, we cannot expect demand and pricing power to come down significantly without seeing collateral damage to corporate profits. And those force downward revisions to earnings, which creates collateral damage to the economy. Economics 101. Period.

Every recession in the U.S. has been preceded by either an oil shock, Fed tightening, or an inverted yield curve. In 2022? We have experienced all three.

This U.S. Federal Reserve (the Fed) seems determined not to make the same mistakes as the Volcker Fed, which we could say had a “stop / start” approach to rate hikes, and in the end caused an even worse recession and crushed consumer confidence. Fed Chair Powell has committed to steadily increasing rates, purposely overtightening in order to defeat inflation.

Signs of lower U.S. inflation are starting to show up:

- Gas prices are down almost 40% from their peak in June

- Used car prices are down 20% from peak

- Global freight rates are down 80%+ from their 2021 peak

- Fertilizer prices are down 45% since last March

- Rents have inched down in September, October, and November

- Home prices are down 20% to 25% from peaks

The year 2023 is starting by offering investors myriad investment opportunities both in the short and longer terms. Short term investors can now get 4% to 5% on cash equivalent products like high interest savings accounts or Guaranteed Investment Certificates (GICs). Fixed income investors can buy short- and medium-term Canadian corporate bonds that are now yielding 5%. Those looking for yield from equities can find many with yields above 4% to 6% from companies with solid long tern track records of raising dividends each year. Growth names like Amazon, Microsoft, Brookfield, etc. have been marked down dramatically, yet the longer-term outlook for many of these companies remains very bright. Stocks overall will very soon trade closer to reasonable values.

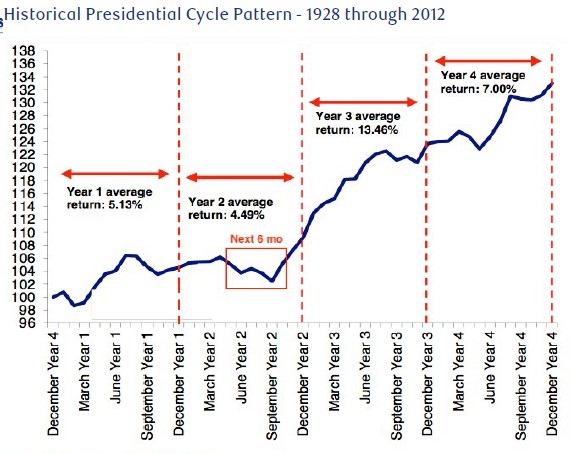

From a cycle perspective, we are entering the third year of a President’s term, the “Pre-election” year. History has shown them to be decent periods in which to be invested:

(Source: Investing.com https://www.investing.com/analysis/trading-the-worst-6-months-and-the-presidential-cycle-200312125 )

We think 2023 will be a decent year. Not great, but decent. We are coming off a huge negative sentiment bottom, the bond markets right now are pricing in 200 Fed basis point cuts later in the year, and inflation should continue to ease. Volatility has started off somewhat sedate, and credit spreads should tighten at some point. Those are all positives.

We urge investors to stick with their long-term investment process and not let short term uncertainty knock them off their longer-term path. At some point, the economy (and markets) will start to recover even as news may seem to be getting worse. The economic data does not have to improve for the markets to rally, it just has to be “less bad” than what’s already priced in. It happens every cycle since the beginning of time. The more people fear the current uncertainty, the more opportunities appear.

There is no substitute to owning a high quality, balanced portfolio. In the end, things always sort themselves out and these frustrating times will pass.

I mentioned earlier we are approaching that inflection point in the markets. Maybe we are close, maybe we need another 5% to 15% lower? Maybe, I don’t know. But what I do know is that whenever that final bottom is put in, whatever that number is on the major indices, wherever that low is made, it will be the last time we will ever see that number and those lows again in our lifetimes.

Stay tuned,