Macroeconomics Outlook - September 2021

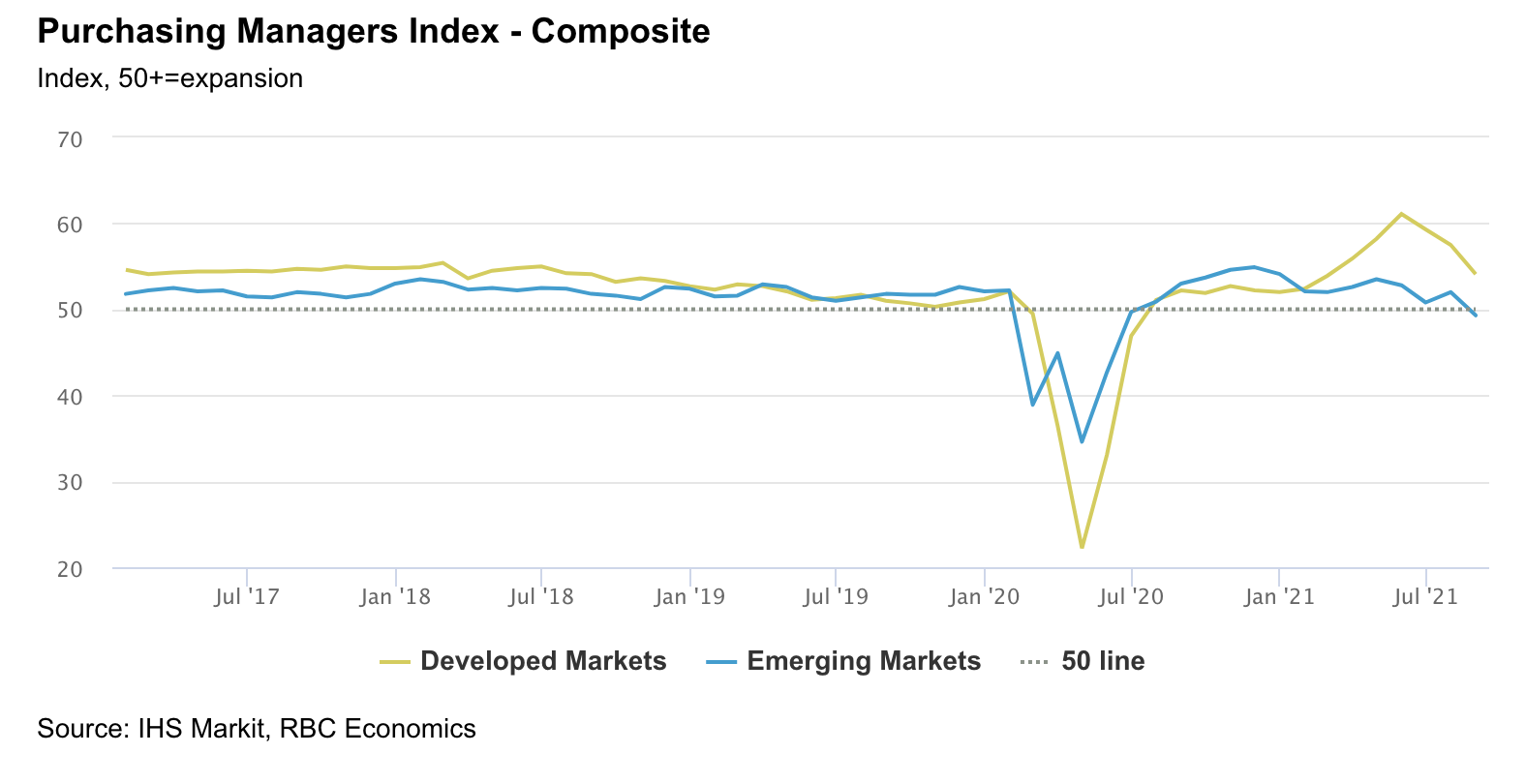

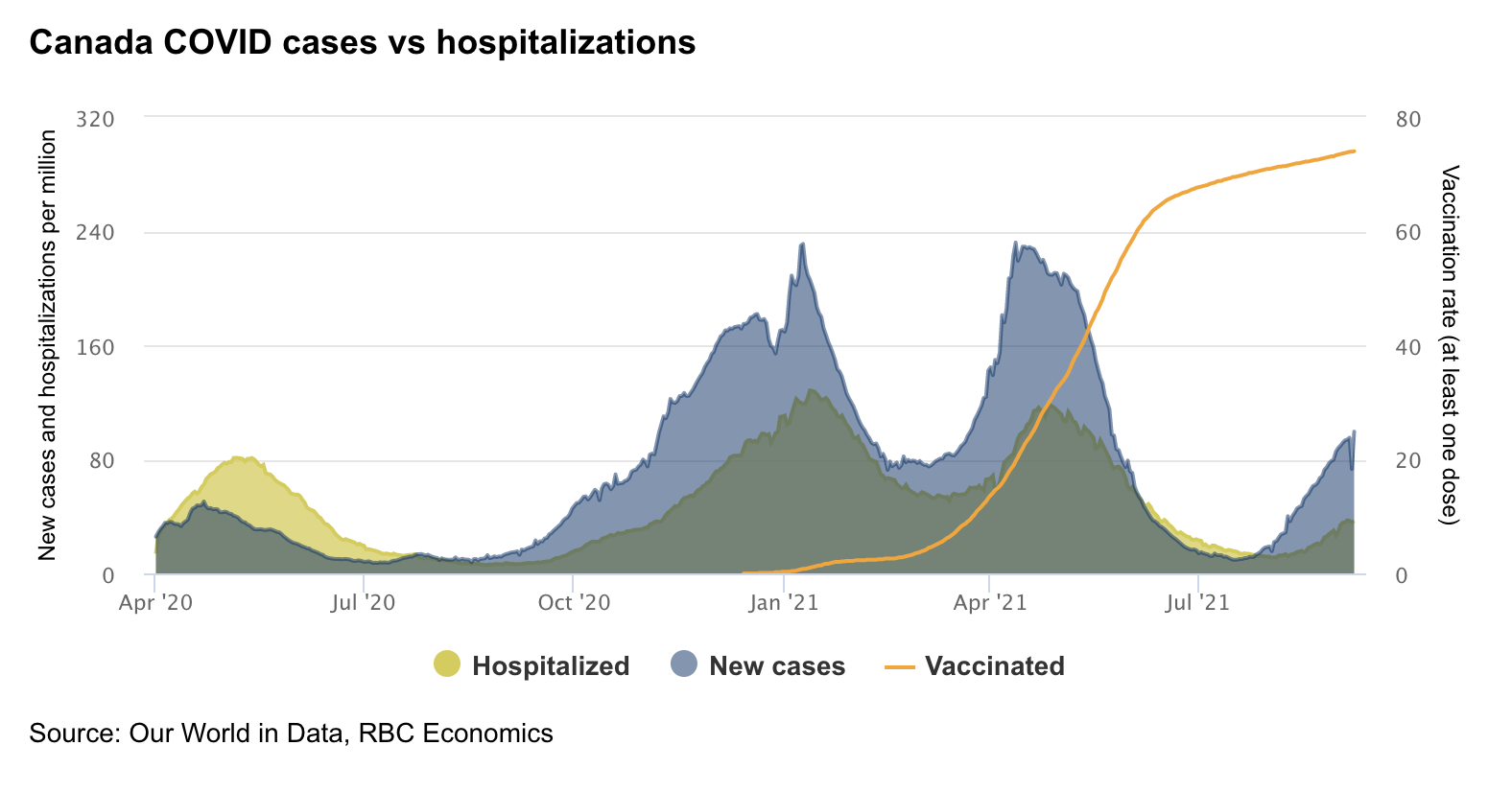

The spread of the Delta variant of COVID-19 and slow vaccination rates in many emerging market economies created another detour in the road to recovery for the global economy. Supply chain disruptions and labour shortages continue to weigh on manufacturers ability to deliver product. Services providers are also struggling to find workers while virus spread threatens to limit the recovery in the hospitality sector. While these constraints may act as a speed bump to global growth, the combination of government stimulus, low interest rates and high vaccination rates in advanced economies will keep their recovery on course for the remainder of 2021.

The IMF updated its forecast for the global economy in July though the subsequent rise in infections has created some downside risk to the upgraded outlook for the advanced economies. World GDP was forecasted to post a 6% rise in 2021 followed by a 4.9% increase in 2022.

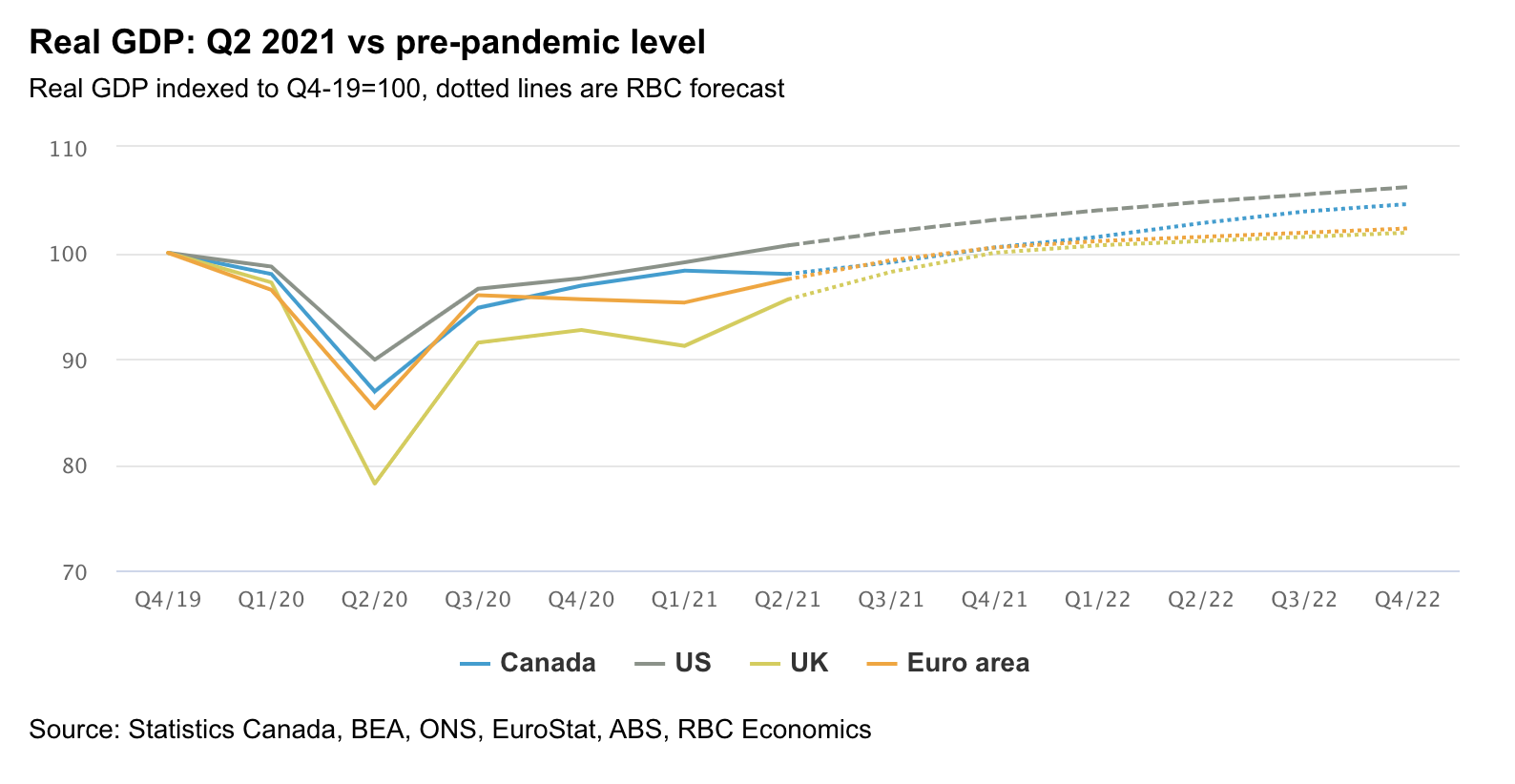

The US, UK and Euro-area posted impressive gains in the second quarter of 2021 with the US returning to its pre-pandemic level of GDP while the UK and Euro area trimmed the shortfall. The outlier was Canada where longer and more extensive lockdowns resulted in GDP falling in the second quarter pushing the economy further away from where it was before the crisis. The spread of the Delta variant of COVID-19 is generating some downside risk to the near term outlook, however given the high level of vaccinations in Canada, the US, UK and Euro-area we expect fewer restrictions to be implemented making the impact on the economy much less severe than in previous waves.

Staying the course

Sizeable government spending and extraordinarily low interest rates will continue to support the recovery. Some government measures are expiring, including a winding down of supports for unemployed workers, but on balance fiscal policy remains supportive. Monetary policy also remains highly accommodative. The Bank of Canada was first to taper asset purchases and will likely stop adding to its balance sheet holdings by year end. We expect the US Fed to start a similar process later this year. Neither central bank however is expected to raise the policy rate until late 2022 which will limit how high rates go from recent lows.

Reliance on policy support is expected to wane as economies are able to reopen. The surge in consumption of goods that fueled the initial stage of the recovery will be replaced by consumption of services, increased business investment as companies rebuild capacity and exports as global trade flows resume. In the near term, supply chain bottlenecks and labour shortages could weigh on the expansion and generate upward pressure on prices. We expect that as businesses increase capacity and workers return to the labour market, these impediments to growth will recede. Price pressures similarly are expected to ease from current elevated levels as the temporary effects associated with the pandemic and reopening fade. That said, inflation rates are likely to remain above pre-pandemic levels for the remainder of this year and into 2022.

Canada’s economy hits speed bump

The economy contracted at a 1% annualized rate in the second quarter as strict lockdown measures early in the quarter hurt spending on services and resulted in job cuts. Consumer spending on goods slumped in the quarter as supply shortages clipped product availability and retailers were forced to close to in-store traffic in parts of the country. Cooling housing market activity also played a role with residential investment falling for the first time in a year. The biggest weight on the quarter however was the sharp decline in exports which mainly reflected a drop in autos and parts. Business spending conversely rose in the quarter as companies worked to boost capacity by investing in machinery and equipment. On net, the Q2 dip left GDP 2% below its pre-shock level.

Q3 off to a soft start

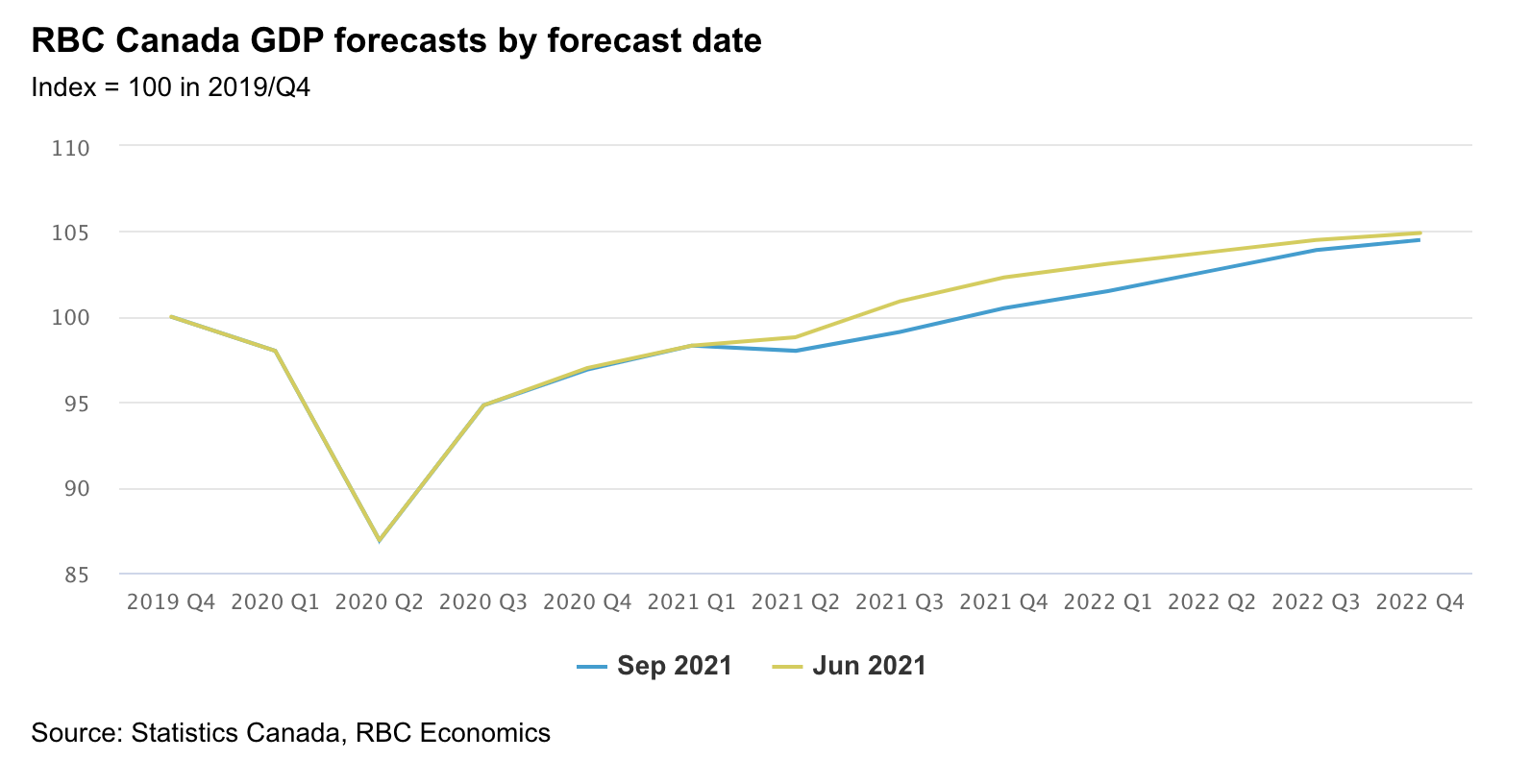

The early read on output in July showed the economy slipped again though our tracking of the data suggests that this weakness will prove short-lived. Our data showed consumer spending activity increased in early in the third quarter with the hospitality sector enjoying a surge as virus containment measures eased. And even though activity in the goods sector was restrained by severe supply chain disruptions and labour shortages, exports of manufactured products increased. The quarter may have started on a soft note, but we expect strong increases in August and September as restrictions eased further and schools reopened. Another solid gain in the fourth quarter will result in Canada’s economy expanding by 5.1% in 2021, slower than our previous forecast. We’ve upgraded our forecast for 2022 to 4.3%.

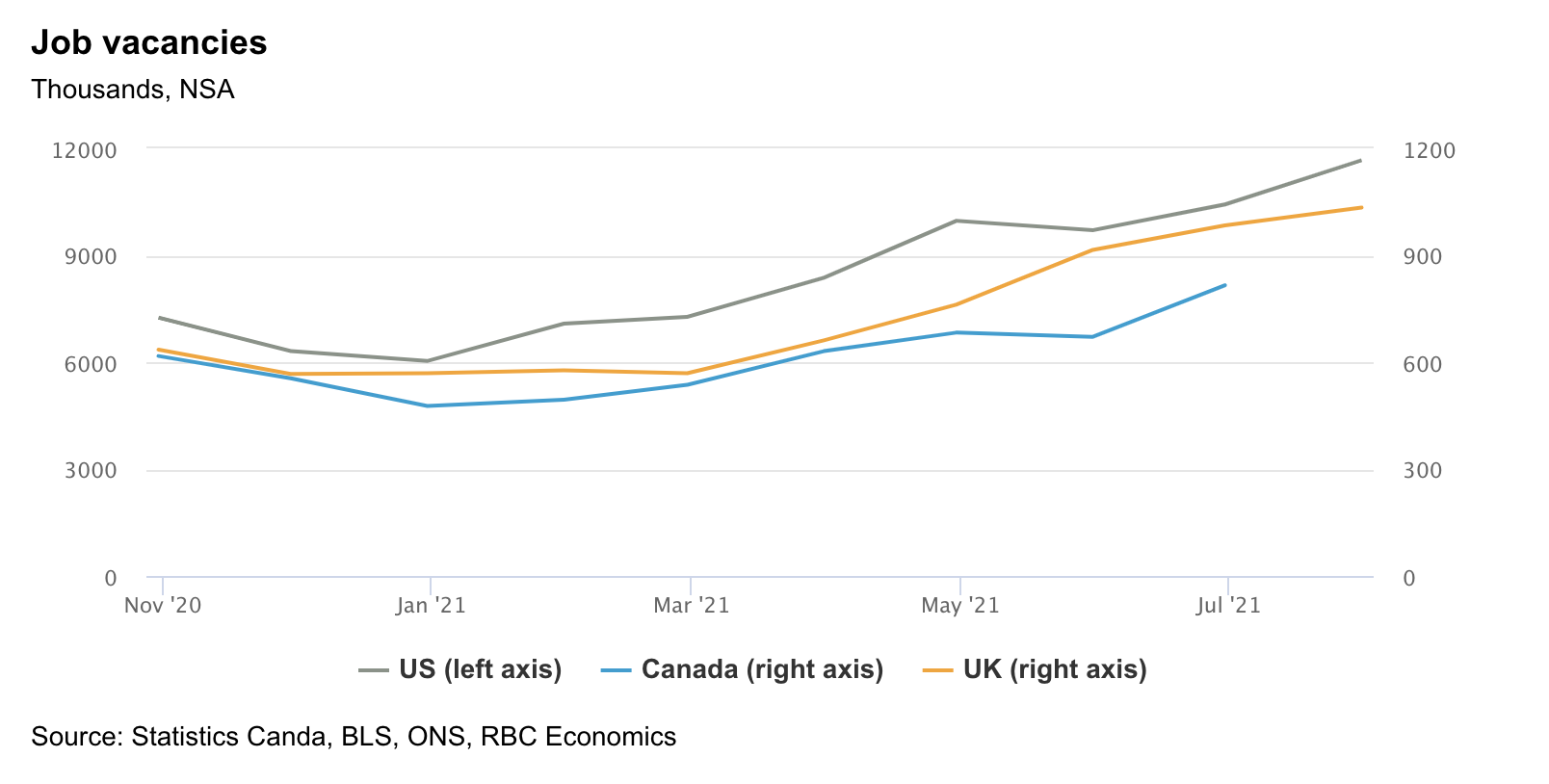

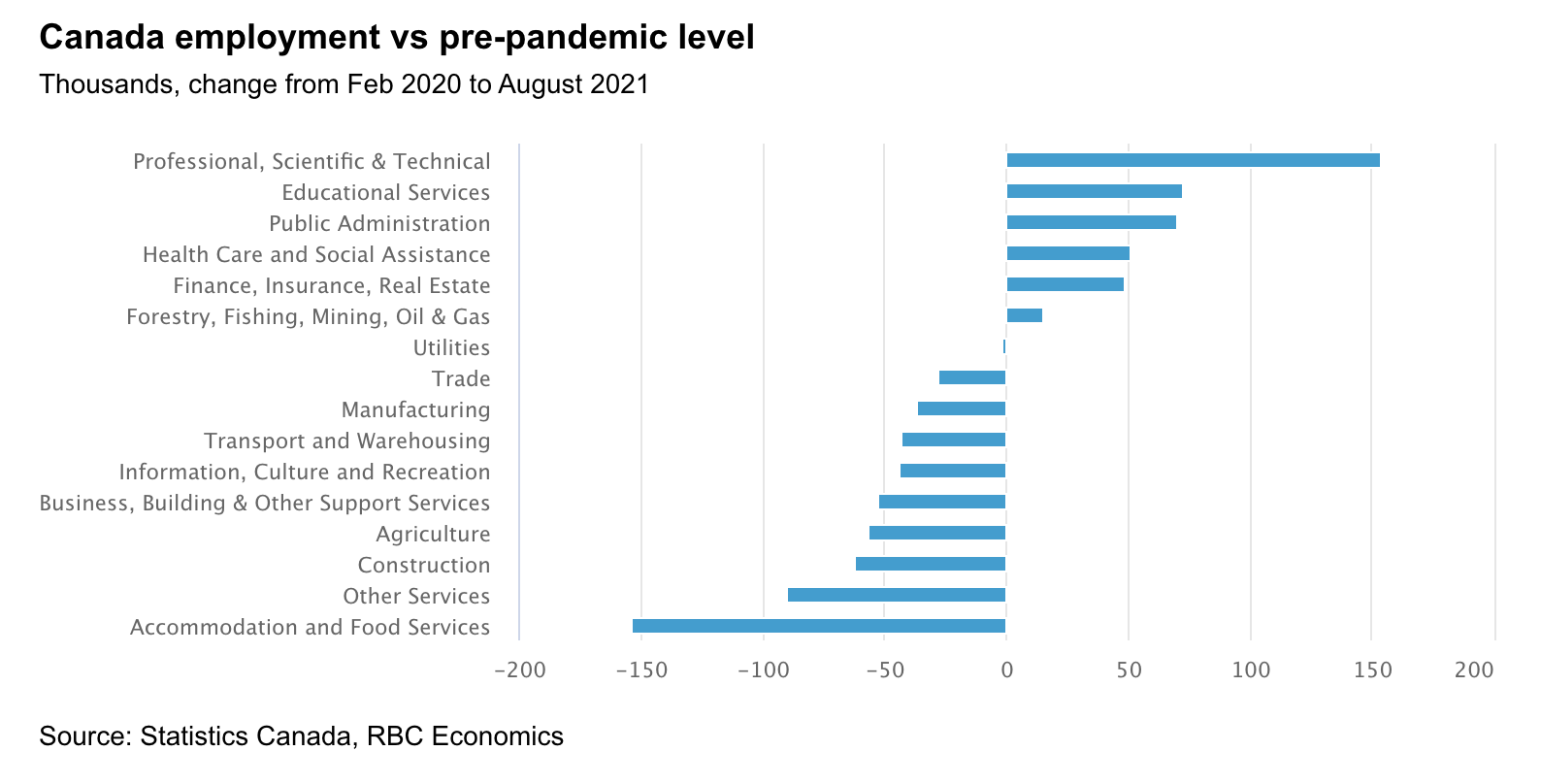

Labour market healing underway, shortages surge

Jobs lost during the spring wave of infections and restrictions were fully recovered in June and July. Another solid rise in August left the pandemic-related deficit at 156,000 meaning 95% of losses have been recovered. Employers faced a growing challenge to find workers with a record 800,000 positions left vacant at the end of June. With the services sectors more fully reopening and vaccination rate rising, more workers are expect to secure positions. However skills mismatches and hesitancy to rejoin the workforce given the spread in the Delta variant means this process will take time and in the near term may force businesses to operate at reduced capacity.

Virus spread keeps consumers sitting on savings stockpile

The massive savings stockpile means households have enormous purchasing power to fuel the recovery but as seen in the second quarter’s weak showing concerns about another round of virus spread and fear of going out can slow that down. Our base case view is that higher vaccination rates will limit the impact of future virus waves on the economy allowing for household spending on services to rise more quickly over the second half of 2021 and in 2022.

Housing market in transition

Home resales continue to transition toward more normal levels after reaching extreme—and clearly unsustainable— highs earlier this year. A number of factors including opportunities for households to spend on other goods and services as the economy reopened underpinned the easing in sales activity in recent months. The deterioration in affordability and tightening in mortgage stress test also played into the market softening though the main factor was and will continue to be the lack of supply. New listings dropped more than 20% from the March high creating exceptionally tight demand-supply conditions and strong upward pressure on prices.

While we expect demand to continue to cool, more supply will be needed to rebalance the market and stabilize prices. On the supply front, more sellers are likely to emerge as the pandemic disruptions ease further and some of the record number of units under construction are completed. While we project sales to decline by 20% next year, the pace will still be above the 10-year average and prices which increased at a double-digit pace this year are expected to post a more modest gain in 2022.

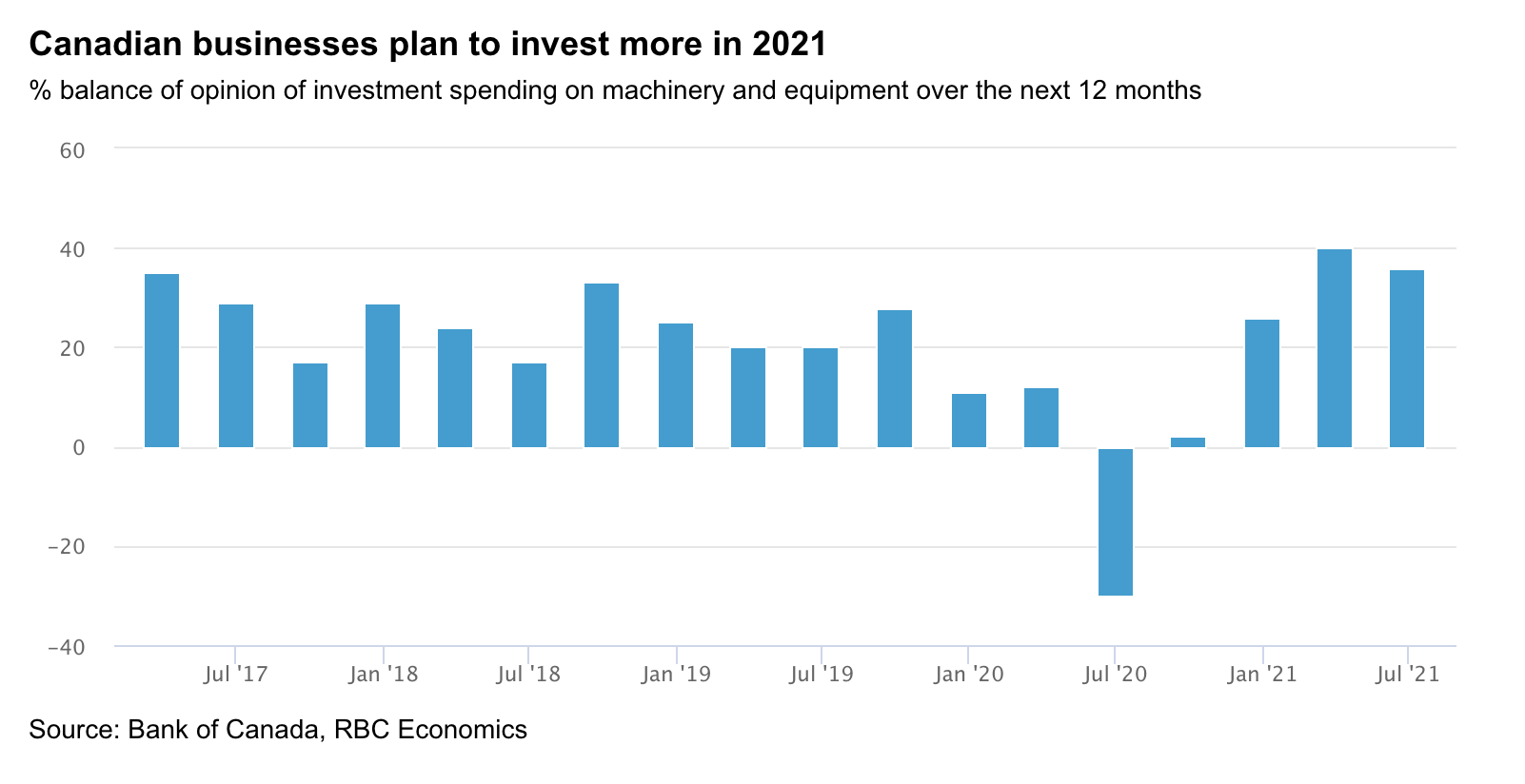

Business optimism fuels rise in investment

As vaccination rates rose and the economy reopened, businesses became more confident with the Bank of Canada’s sentiment index hitting an all-time high in the second quarter. Rather than worries about demand, companies increasingly reported concerns about supply of both inputs and labour. Supply chain disruptions, rising input costs and a scarcity of workers are leaving companies uncertain about whether they could meet demand. In the second quarter, companies invested in machinery and equipment and rebuilt inventories which had been drawn down over the previous four quarters. Firms are expected to continue to invest with some spending more on technology as they shift toward increasing their online presence or manageing their workforce.

Firming demand to put floor under inflation correction

Distortions associated with the pandemic contributed to the sharp increase in Canada’s inflation rate in recent months. As these transitory factors fade, so too will the inflation rate. However the degree to which inflation pressures ease will be challenged by the strengthening in demand. In July, the core inflation rate, which excludes food and energy prices, posted the strongest gain in almost two decades and 65% of goods and services in the CPI basket saw their prices rise faster than the Bank of Canada’s 2% target on a year-over-year basis. With household demand, particularly for services, expected to firm again in the second half of the year and supply chain constraints remaining, the inflation rate is likely to remain elevated. We expect that as capacity increases and supply chains normalize, price pressures will ease however this will take time with both the headline and core measures forecast to converge to 2.5% by the end of 2022.

About the Authors

As RBC Chief Economist, Craig leads a team of economists providing economic, fixed income and foreign exchange research to RBC clients. Craig is a regular contributor to a number of RBC publications and is a key player in delivering economic analysis to clients and the media through the Economics Department’s regular economic briefings.

As RBC Deputy Chief Economist, Dawn Desjardins contributes to the macroeconomic and interest rate forecasts for Canada and the U.S. Before joining RBC, Dawn worked as a reporter for Bloomberg Financial News in Toronto covering the Canadian bond and currency markets. She also spent ten years as the Canadian bond market strategist for a major U.S. bank.

Nathan Janzen is a member of the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.