FinTech is a term coined to describe a rapidly growing industry segment that is aiming to deliver financial services more broadly, efficiently, and innovatively using powerful online technologies, enabled by “Big Data” and cloud computing. Initially arriving on the scene in the form of online-based payment services (PayPal, Alipay, Apple Pay), FinTech enterprises have begun offering access to credit, insurance, and investments. FinTech potentially represents a major disruptive force that will necessitate a response from banks and other financial services providers, as well as from regulators.

What is driving the growth of FinTech?

- Dramatic growth of e-commerce has brought with it the need for easy-to-use, online, secure payment services.

- Huge, underserved populations exist around the world with little-to-no access to banking services or credit. This acts as a powerful constraint to global economic growth and social improvement. FinTech may be uniquely suited to fill these gaps.

- Massive amounts of data available from e-commerce transactions, social media, and internet searches allow FinTech companies to determine what financial services to offer to which person, as well as how to price that product. Data has become more important than collateral for these providers.

- Regulators do not appear to have been able to keep pace with FinTech evolution. This is allowing FinTech businesses to innovate aggressively, and perhaps take risks that their customers are not fully aware of, while restraining incumbent financial services companies, which are regulated, from competing head-on with these new entrants.

What can FinTech offer?

For underserved populations, FinTech’s most dramatic impact is opening up access to credit and offering digital cash transfer platforms. Beyond these, FinTech offers services that have altered and continue to transform the financial services industry.

Low-fee digital cash transfer platforms

Digital cash transfer platforms are now widely used worldwide. These can be particularly beneficial to migrant workers, whose families—often unbanked—rely on receiving money from abroad.

According to the World Bank, funds sent back to the home country are an important source of income for several developing countries, representing a non-negligible four percent of GDP in Mexico, for example, and up to an eye-watering 27 percent of GDP in Nepal. Global remittances in 2019 exceeded $700 billion, with over $500 billion flowing to developing nations. The International Monetary Fund estimates that remittances sent through traditional channels are subject to fees that average 10 percent but can be as high as 20 percent for small remittances of under $200, which are typical for poorer migrants.

M-Pesa, the text message-based payment system initially launched in Kenya in 2007, exploited the opportunity, allowing users to send and withdraw funds via basic mobile phones. The service is now used by 48 million customers across eight countries. According to the World Bank, M-Pesa has advanced the financial empowerment of women, helping them gain control over their income, fostered startup businesses, and advanced financial inclusion, which means that individuals and businesses have access to affordable banking services.

Another example is the UK FinTech company Wise (formerly TransferWise), which provides a low-fee digital payment solution to transfer money, making financial services more affordable across society. It initially differentiated itself from the competition by being transparent about fees and focusing on small transactions. When the company entered the Malaysian market in 2019, its fourth Asian market, the authorities welcomed it, commenting that it would improve financial inclusion and support the country’s balanced economic growth.

Access to credit

FinTech can help improve access to credit for small and medium-sized enterprises (SMEs) and provide services in remote areas through alternatives to traditional lending methods.

A prime example of this is Ant Group, a Chinese FinTech company, which had a profound impact on consumers’ and entrepreneurs’ access to loans. At its peak, Ant counted more than 1.2 billion users and handled 110 trillion yuan in payments ($16 trillion), or over 25 times more than the U.S.’s PayPal.

Starting out as a payment service on Alibaba’s e-commerce platform, the company became the leading app for mobile and online payments, providing credit facilities to smaller enterprises on Alibaba.com and enabling consumers and merchants to borrow money sourced from banks on their smartphones.

Ant is able to gather a large amount of consumer finance data from its parent’s e-commerce platform. This enables it to assess borrowers’ creditworthiness even if they lack the repayment track record required by traditional banks, and to tailor the financial terms of a loan to suit each borrower based on the particular risk profile. As such, Ant can help SMEs access trade finance, supporting their development and expansion.

Other services

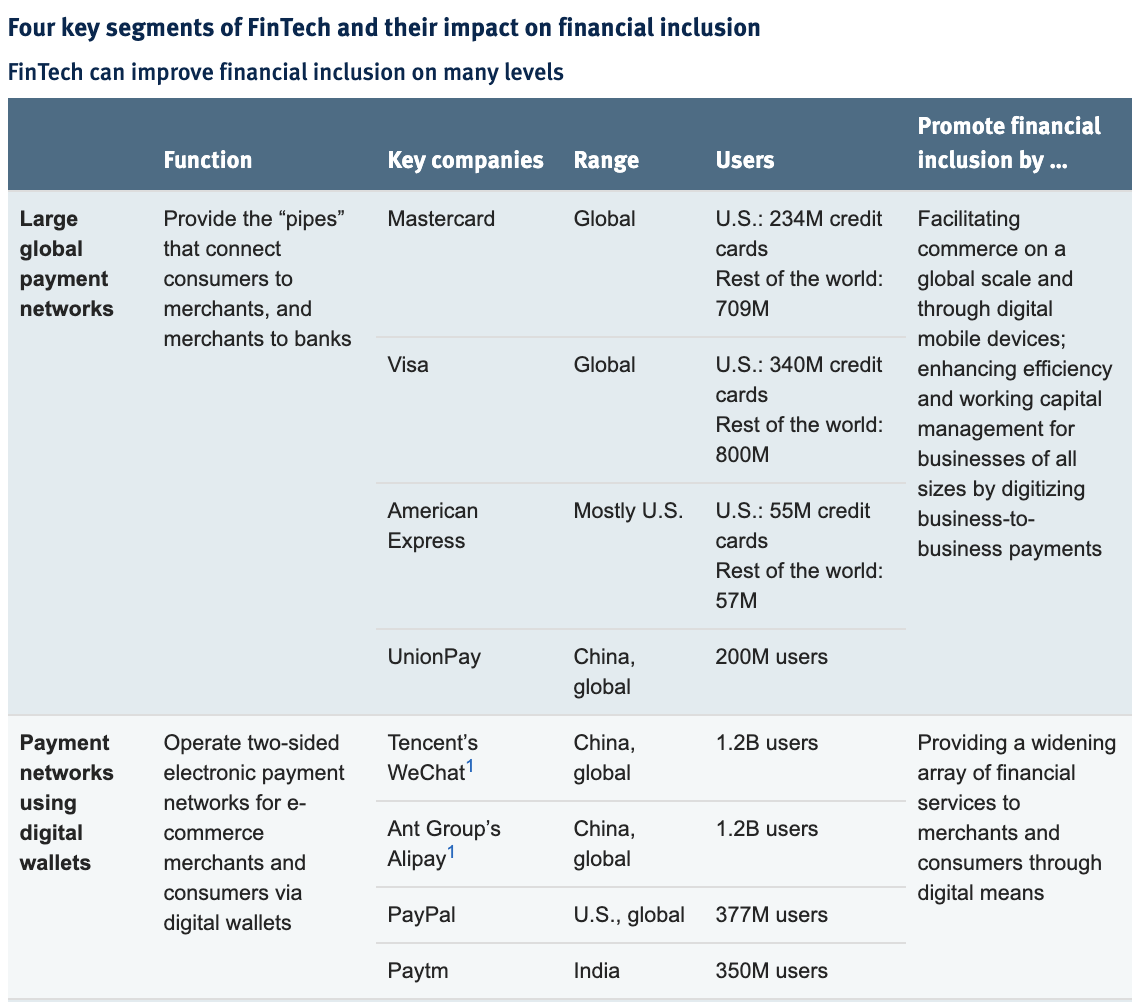

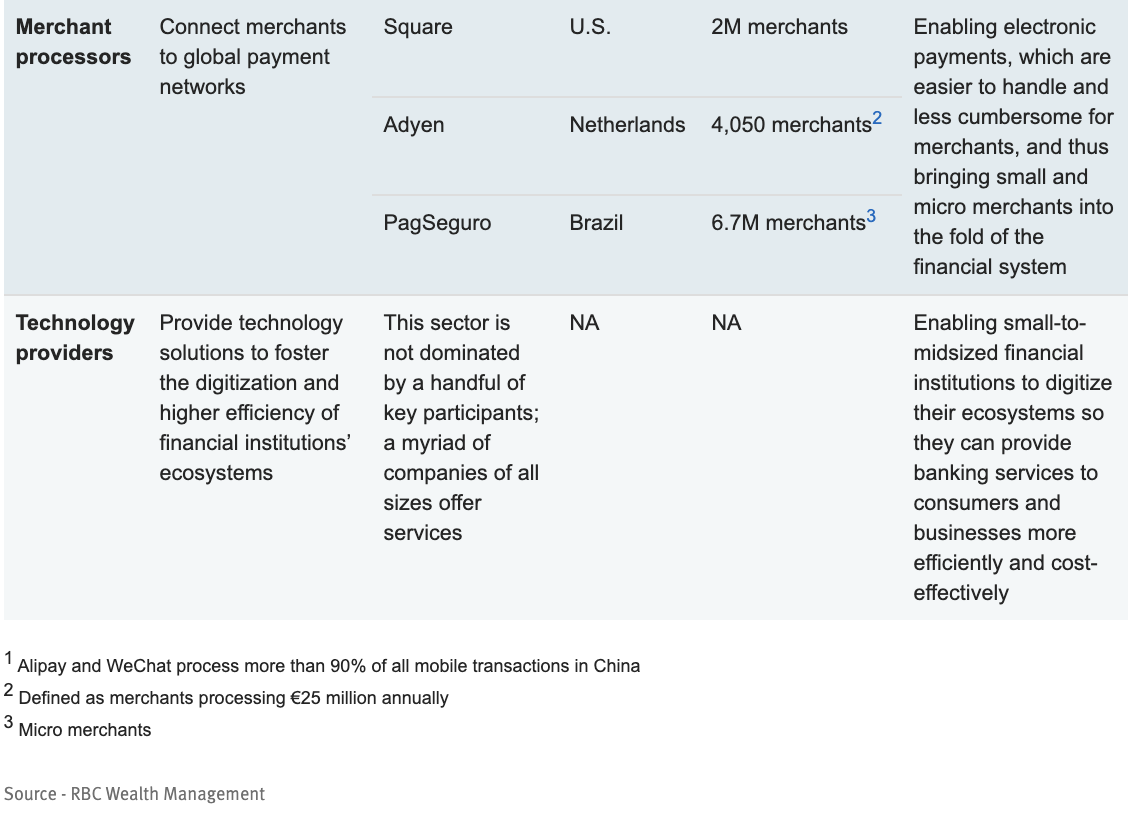

Beyond these, FinTech offers a wide range of services, and we highlight four key segments.

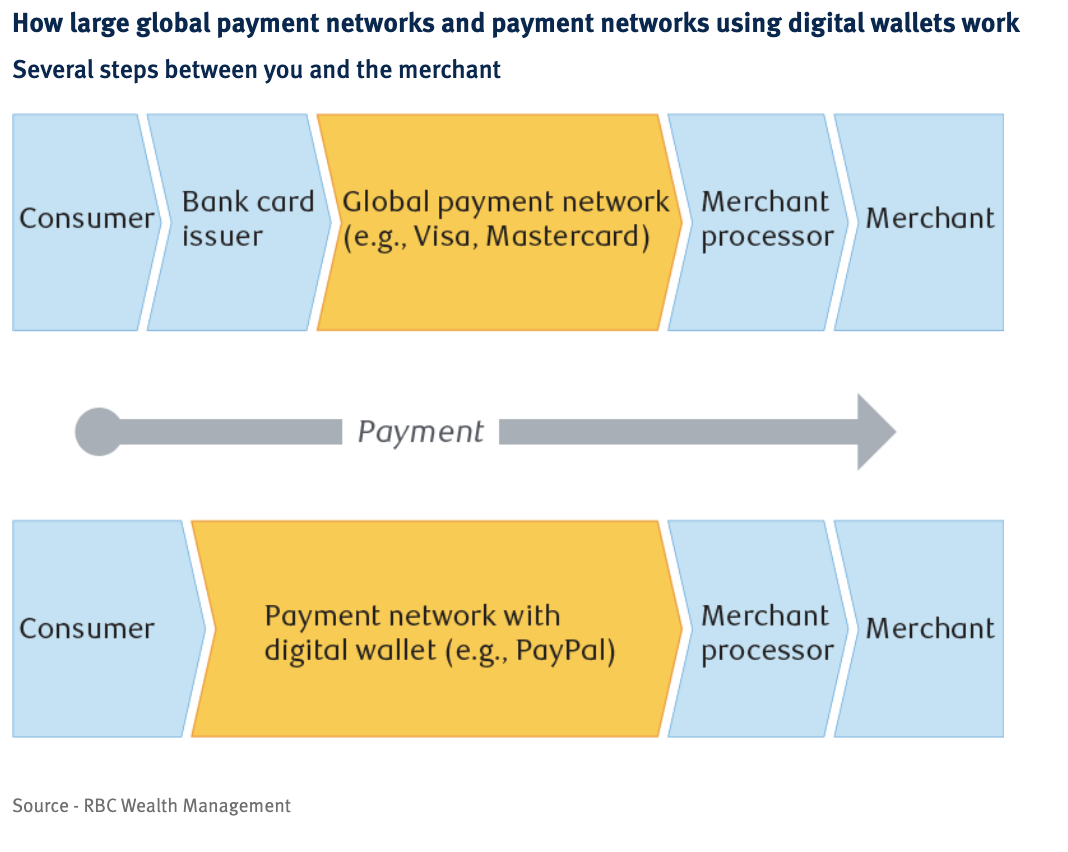

Large global payment networks

Provide payment processing services to merchants who accept credit and debit cards

When paying with a credit card, consumers use a bank-issued card that is linked to a global payment network, such as Visa or Mastercard. The merchant, in turn, works with a merchant processor who manages the credit card transaction process and is an intermediary between the merchant and the financial institution involved, authorizing transactions and helping merchants get paid on time by facilitating the transfer of funds.

Global payment networks enable consumers and merchants to smoothly conduct commerce on a global scale and to utilize digital mobile devices, opening up new opportunities for merchants. They can also enhance overall efficiency and working capital management for businesses of all sizes by digitizing business-to-business payments.

Payment networks using digital wallets

Provide direct connection between consumers and merchant processors, operating via software-based systems that store users’ payment information

Digital wallets allow a party to make electronic transactions and bypass traditional banks. According to market data provider Statista, digital wallets accounted for 44.5% of all global e-commerce transactions in 2020. Solutions within a consumer digital wallet can include merchant payments, peer-to-peer payments, international money transfers, bank accounts, lending, and cryptocurrency trading.

Merchant processors

Manage the credit card transaction process and act as an intermediary between the merchant and the financial institution involved

Merchant processors can have a large impact for small merchants by enabling them to accept electronic payments so they do not have to handle cumbersome cash and checks.

Technology providers

A FinTech opportunity: Improving financial inclusion can unleash growth

Financial inclusion is a key challenge across the globe. A lack of access to basic financial services can create crippling financial problems for individuals and businesses, in turn holding back an economy’s growth potential.

According to the World Bank, more than 1.6 billion adults, or just over a quarter of the world’s adult population, do not have a checking or savings account, access to credit, or insurance. This leaves them unable to store, send, and receive payments, unprotected from theft and loss, and without safeguards if they lose their jobs or fall ill, making them vulnerable to predatory lenders.

Substandard infrastructure ranging from an inadequate supply of electricity to poor internet access (particularly in remote areas), the struggle to maintain minimum balance requirements, the lack of identification documentation (which affects one billion people worldwide and 45 percent of women in low-income countries), the lack of a financial track record, and prohibitive costs are typically the reasons why adults do not have a bank account.

However, per the World Bank, more than two-thirds of adults who do not have access to a bank account, do have a mobile phone. Today’s technology enables the delivery of financial services through even a basic mobile phone (i.e., non-smartphone).

Low financial inclusion also affects small and microbusinesses. In 2016, the International Finance Corporation estimated that more than 160 million of these entities lacked access to finance and another 160 million were underbanked—meaning they might have a bank account but do not have access to banks’ term loans or working capital loans.

Not exclusively an emerging market issue

The unbanked adults are predominantly in emerging economies. Some emerging market governments that are alert to this issue have invested in infrastructure and encouraged banks and startups to look to seize the opportunity this state of affairs presents.

China strove to address the urban/rural differences at the root of its large unbanked population as it recognized the economic potential of closing this gap. It encouraged the development of infrastructure such as broadband networks alongside allowing a growing role for the private sector to advance financial services, hence the progress of Alibaba’s Alipay and Tencent’s Tenpay (including WeChat Pay). Together these online payment platforms process more than 90 percent of all mobile transactions in the country.

But poor access to banking services is also a problem faced by an uncomfortably large population in developed economies, particularly the underbanked who have a bank account but no access to credit or other financial services.

The Federal Deposit Insurance Corporation’s 2019 survey “How America Banks” found that 7.1 million (or 5.4 percent) U.S. households had no bank account, while a report by the Federal Reserve the same year calculated that 16 percent of U.S. adults were underbanked. Mintel, a market research firm, reports that six percent of Canadians are unbanked, without a checking or savings account of any kind, and a further 28 percent are underbanked. In the UK, the Financial Conduct Authority estimates 1.3 million adults are unbanked, while the European Central Bank (ECB) calculates that some four percent of households in the EU do not have a bank account.

Central banks and regulators need to adapt …

RBC Global Asset Management Inc.’s Julie Thomas, a senior portfolio manager specializing in global financials, points out that while the traditional financial system is regulated, offering safety and security for savings, and thus a high level of comfort to users, FinTech sits outside this regulation, affording no such security.

Moreover, for central banks, unregulated newcomers can make delivering monetary policy more difficult. How can central banks control the risk to the economy from increased leverage as FinTech represents a growing share of financial services?

Concern over the loss of control over the economy explains the recent flurry of activity by many central banks to create their own digital currencies. A central bank-backed digital currency would be a digital version of cash, equivalent to a deposit with a nation’s central bank.

China launched the e-yuan in 2020; the ECB aims to launch its own digital currency in 2025, while the Bank of England and the Fed are actively exploring the issue. A January 2021 survey by the Bank for International Settlements (the bank for central banks) reported that most central banks are considering digital currencies. The survey found that central banks representing a combined 20 percent of the world’s population are likely to launch their own digital currencies within three years.

Increased regulatory scrutiny on FinTech is also likely, particularly with the advent of “super apps,” which are popular in emerging countries. These platforms started out by being a dominant provider of a service used daily by customers, such as ride-hailing services (e.g., Grab in Singapore) or e-commerce (e.g., Mercado Libre in Latin America), and expanded from there into financial services including payments, insurance, and investment. Super apps are blurring the lines between financial services and other industries. Regulatory authorities will likely focus on who controls the data and how it is used. This will be a key issue particularly in Europe where protecting data privacy is a primary concern.

… as will traditional banks

Some traditional banks, concerned about the newcomers encroaching on their territory, are adopting some of these FinTech approaches. Technological capability is not an issue: most banks have been delivering progressively more online access to services for the past 20 years. But FinTech entrants, unencumbered by legacy systems and traditional banking practices, not to mention regulation, have successfully gained ground in market segments that banks traditionally regarded as uneconomic, lacking potential, or too risky. They have also pushed into offering some “high-touch” services, usually delivered person-to-person, with a “clickable” ecosystem featuring decision-making algorithms.

Some traditional banks have opted to create hubs external to their main businesses so that these new approaches can be properly nurtured. Once mature, these processes may be adopted into the core businesses. This should be a low-risk way to integrate new technology into a traditional bank, mitigating threats to branding or customer confidence while closing the technological marketing gap with FinTech companies.

Others may choose to buy established new entrants, much like JPMorgan’s recent acquisition of Nutmeg, a successful and well-known UK robo-adviser.

Embrace the evolution

The face of finance is changing rapidly, and regulators and central banks alike are taking notice. The arrival of a wider range of participants in financial services makes their task more complex. They will have to adapt, as will traditional banks in order to fend off the approach of newcomers into their territory.

FinTech will not single-handedly lift all of the “bottom two billions”—the poorest individuals in the world—out of poverty. But to the extent that it can reach a portion of them and give them access to financial services, economies will likely benefit and the companies that make inroads into this market segment with a well-thought-out strategy should see bright prospects.

We believe the disruption can create investment opportunities in those FinTech companies that gain staying power, as well as in the traditional banks and financial services providers that are able to effectively embrace this new paradigm.

With contributions from Jason Deleeuw, CFA, U.S. Equities Portfolio Advisor, RBC Wealth Management Portfolio Advisory Group – U.S. and Stephen Chang, CFA, U.S. Equities Portfolio Advisor, RBC Wealth Management Portfolio Advisory Group – Equities, RBC Dominion Securities Inc.

This article is the fourth part in our ongoing SusTech series, which is exploring the confluence of sustainability and technology and why this concept matters as an investment theme.

Previous articles in the SusTech series ...

- What is sustainable technology?

- SusTech: Sustainability through technology

- GreenTech: Transformation to a clean energy world

- HealthTech: How technology can help fix health care