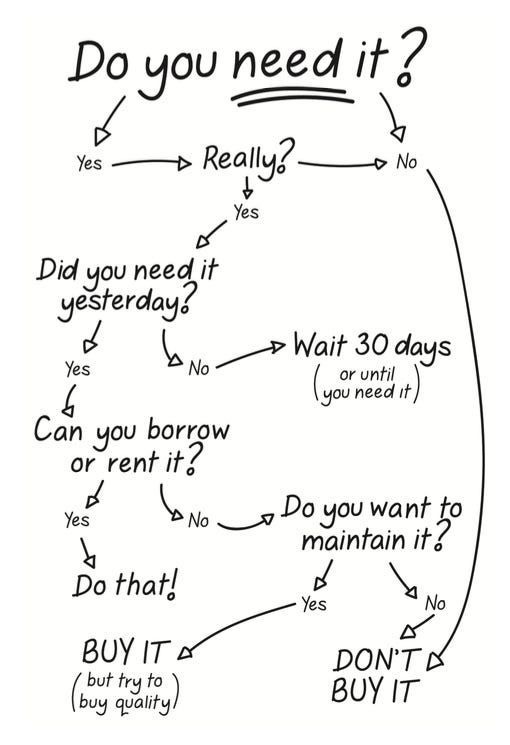

Before my recent exposure to the world of finance, I seldom planned and saved my income. As a student, I would fritter my money away on weekends and lived beyond my means. While that $80 Aritzia skirt offered me instant gratification, the impending doom of falling into debt was not worth the stress of keeping up with trends.

Since joining Borelli Private Wealth, I have been enriched with financial knowledge that has since greatly benefited my personal life; I learned the importance of self-care through my wealth and the value of saving for my future. But first, it was time to admit my financial sins in order to save for the life I wanted to build.

As I began pondering on my next steps, multiple questions came to mind. What do I invest in? Should I save into an RRSP or TFSA? If so, how much do I contribute? With the wealth of information on the Internet, where do I even begin? These are the types of questions many ask themselves when confronted with the same reality.

The idea of budgeting and investing seemed overwhelming to me. Luckily, I am surrounded by experienced professionals who enlighten me with answers to my pestering questions. Hence, with the newfound wisdom that I gained from Dario, Simon and Michelle, here are a few things I wish to share with our readers.

Budgeting

With the cost of living on the rise and saving money seemingly more challenging than ever, how do the younger generations manage their spending and saving today?

As our team’s expert in financial planning, Michelle’s role is to set expectations that align with one’s monetary goals. One of the first things that I learned and what is possibly the most difficult part was the notion of paying myself first by saving a portion of every paycheck for the future.

But just like how a good pair of shoes is all about finding the right fit, so should be your budgeting structure. Look at your paycheck each month and evaluate how much of your take-home pay is going towards your needs, your wants, and your savings.

Here is a little breakdown on what those points mean:

-

Needs: Housing, food, transportation, health care, all non-discretionary spending.

-

Wants: Vacations, dining out, entertainment and streaming, etc.

-

Savings: Retirement fund, emergency fund, or a personal goal.

The traditional budgeting formula has always been:

Income - Expenses = Savings

Ideally, however, you should be paying yourself first. Making savings a line item in your monthly budget can help ensure you will stick to your objectives over the course of a calendar year. In a sense, you’re tricking yourself into achieving your goals by automating part of the process as I will explain in a moment. A little tip for those starting to save; try to set up an automatic savings plan directly from your bank account to make this a case of “out of sight, out of mind”!

I had always assumed that my savings would equate to whatever I had left over after paying my bills and spending my money on fun things. Although to be honest, that usually left me with very little to almost nothing for my savings at the end of each month. As much as I’d love to YOLO* my way through life, I learned from paying an unexpected parking ticket, that this savings strategy was not an effective one.

According to Michelle, you should be determining your savings backwards. Ask yourself, how much do I want to save for my dream vacation? Or if I want to purchase a home, how much do I want to put as a down payment? And later when I retire, how much do I want to spend during my retirement? These are all crucial questions to ask yourself at different stages of your life and career. In our next article, we will delve into the power of compounding. You would be surprised to learn how accumulating a modest amount of savings today can significantly increase the growth potential of your portfolio when applying the power of compounding.

By implementing a budgeting strategy and creating a savings plan that suits your means, you will find yourself achieving financial success as you will begin prioritizing your future goals.

For a more detailed understanding on financial planning, stay tuned for our next chapter as I dive deeper with Michelle.

*You Only Live Once