Looking back at my monthly summer expenses, I wonder whether straying off my monthly budget was a wise move. Was religiously dining out and booking a #EuroSummer trip worth the exchange of financial freedom in the next 20-30 years? To my own dismay, I look at the potential value of my investments and immediately crumble in fear.

When I first started the conversation of savings with my friends, I was incessantly given the same advice by my older peers- “start saving early, because catching up won’t be so easy”. I have met many advisors who go into detail about investments while trying to illustrate concepts I can scarcely understand. Here I am, still eating instant noodles and these well-dressed professionals want me to envision my life 40 years into the future, when I can hardly keep my head above water now. Like many of our youth, the future seems daunting when most of us launched our careers at the onset of the Covid pandemic.

In the financial world, there is a popular aphorism that the rich get richer. While this may seem unfair, the idea likely stemmed from the power of compounding. Have you ever had someone tell you to save your money early but not understand why? Within investments, compound interest refers to an arithmetic method* that does wonders for your savings. Before we dive further into the actual theory of compounding, allow me to introduce you to some terminology.

Principal (P): initial investment

Interest (i): the monetary charge for lending or borrowing money

Term (n): number of compounding periods

Compound interest is a concept that plays a critical role in making money grow over time. Say you leave money (principal) alone in your investment account earning 8% interest annual. Over time, you will notice your funds grow based off your principal and interest. This increase stems from the interest that was earned from the initial principal, but also on the accumulated interest from previous periods. The key idea is that compound interest grows faster than simple interest. Over a long period, compound interest can significantly increase the value of your investment. As this process continuously rolls, your money really grows without any work on your end. Let us visualize this concept with an example.

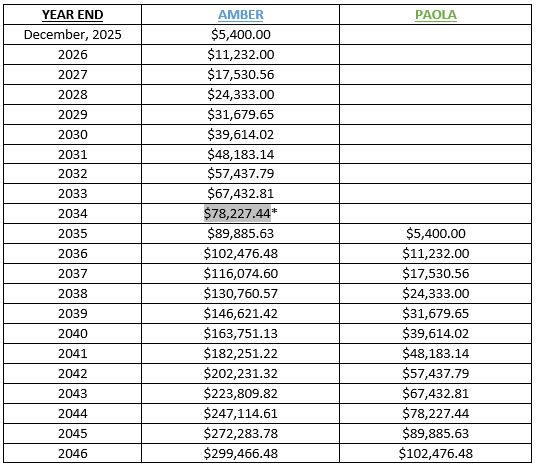

My friends Paola and Amber are both currently in their mid-20s and share the same long-term goal of saving for retirement at 65. They decide to save an initial principal of $5000 and contribute $5000/year into their RRSP* account earning 8% annually. However, as much as Paola is in denial, she tends to be the bigger spender and believes she can make up for any lost time by delaying her savings plan for another 10 years. After all, she genuinely trusts there is no harm in waiting 10 years as she is saving the same amount as Amber. In contrast, my astute and frugal friend Amber, lives moderately and only goes out on the weekends. Do you think deferring the start date for your investments will create a bigger impact on the ending investment value? Absolutely. By the time Paola invests in her first $5000, Amber would already have accumulated an amount of $78,227.44* within 10 years! In other words, for the $50k that she invested, she created almost $30k of new wealth for herself, thanks to compound interest and discipline.

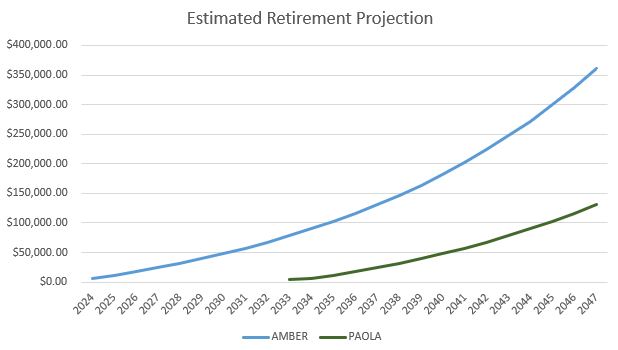

There is a catch to compound interest that is hard to accept- you must give it time! This won’t work if you pull your savings prematurely before they have time to grow. As shown in our graph, you can visualize the investment growing exponentially as opposed to linearly. By leveraging the power of compound interest, Amber is now better positioned to enjoy a well-funded retirement. At 65, she may be soaking in the sun by the beach, while Paola is still working in the bitter cold to make up for the years that she missed. If you learn to delay indulgences and flex your patience muscles, you’ll find that your money will ultimately do the work for you.

The beauty of compound interest is for those who are young and have a long-time horizon, you have the greatest advantage on your side: time. It is a great teacher of patience as you do not see results overnight. In retrospect, perhaps I should have followed Amber’s footsteps instead of accepting Paola’s dinner invitations. Now, my green hued eyes can only wish I had lived a summer as modestly as Amber’s. Though it might take me years to enjoy living lavishly, I may enjoy the fruits of my labor in retirement knowing I made passive income from my incremental monthly savings.

Footnote

Compound Interest Equation* = A = P (1 + r/n) nt

RRSP* = Registered Retirement Savings Plan: The Navigator (rbcwealthmanagement.com)

Consider using the following future value calculator to estimate the value of your investments: https://www.rbcroyalbank.com/investments/future-value-calculator.html