Dear partners,

As most of you know, our family’s entire portfolio is invested in exactly the same manner as yours. We own the same stocks and bonds as you, and adjusted for our risk tolerance (high) we hold them in the same proportions. We even pay the same fees as you, just to ensure that we don’t miss out on any part of the experience.

This is very purposeful; it ensures two key characteristics:

1. That our family’s economic interests are directly aligned with yours; and,

2. That we experience the same up’s & down’s as you do.

It is not lost on me, therefore, that the past three months have been moderately unpleasant for our portfolios. Having happily chosen a vocation that keeps me immersed in financial markets day-to-day, I am very comfortable with periods like these. Many of you enjoy spending your time on other (better) things however, so I thought that you might value some Holiday reading outlining: a) what has occurred; b) how our portfolios have fared; and, c) what 2019 is likely to hold.

For those short on time or interest, the rest of this email can be summarized in three main points:

1. This year your portfolio has meaningfully outperformed the market;

2. The recent sell-off is sharp, but it is easily within historical norms; and

3. The set-up for 2019 isn’t perfect, but it is very attractive.

Some of you may wish to stop reading here. If that is the case, the entire team here wishes you a very Happy New Year, and please expect to hear from us in the coming weeks to schedule your Annual Review. For those of you so inclined, please read on…

What has occurred:

From a gut-feel perspective, the October to December decline has been the worst feeling period of market performance since the European debt crisis seven years ago. December has been particularly bad: of the 17 trading days to-date, only 5 began with what I would consider to be positive news and only two of those managed to end up without losses. Perhaps worse, risks that previously appeared to be remote emerged with ferocity.

Reflecting this, the S&P 500 has fallen 16% since the start of October and is down 8% for the year. The less diversified TSX has fared worse, down 13% for 2018.

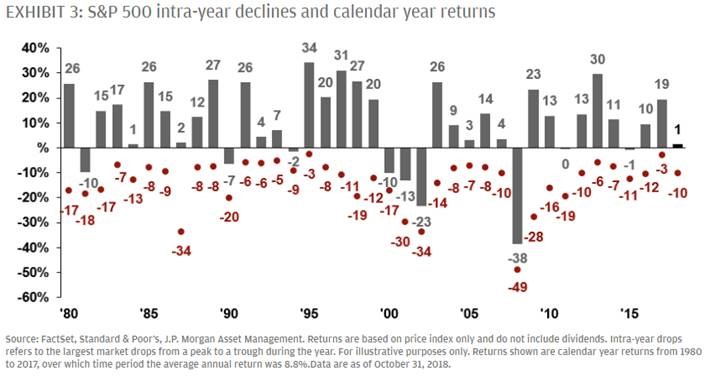

From a quantitative perspective though, while these numbers are notable they are also well within normal ranges. For example, look at the graph below: it shows that in over 1/3rd of the years since 1980, the stock market has experienced a decline of similar or greater magnitude to the 16% peak-to-trough selloff that we have just witnessed.

(Annual return in grey, largest price decline for that year in red;

all numbers are %. Annualized return since 1980 = +13%)

The causes of these selloffs are generally unique and always feel acute in the moment, even if they are eventually overcome. In 2015 it was China devaluing their currency together with oil prices dropping 65%. In the winter of 2011/12 it was the Greek sovereign debt crisis; 1998 was Long Term Capital Management collapsing; etc.

This year’s circumstances have been standard economic concerns following two years of US interest rate hikes, combined with non-standard fears about the impact of a US-China trade war. In recent weeks, particularly wild political unpredictability has compounded these factors.

What is interesting is that both of these factors are reasonably quantifiable. For example, using a fairly well-reputed piece of economic theory called the Taylor Rule, current US interest and inflation rates imply that GDP growth should slow to about 3% from its current 4% rate. On the trade side, this excellent article by Nobel-laureate Paul Krugman pegs the impact of a global trade war (not just US-China) to be a drag of about 3% on GDP, spread over multiple years.

The ability to quantify these risk is important because dramatic market shocks tend to occur when the risks are deemed undefinable. Think of 2000-2002 (“how do I actually value these dot-com companies that have no earnings, and what if every company is just a fraud like Enron anyway?”), or 2008-09 (“the world’s largest banks might be insolvent and there is no way to disprove it because their balance sheets are so complex”). By contrast, garden-variety market corrections and bear markets occur when conditions change for the worse but in a definable fashion.

How have your portfolio fared:

We have benefited from some successful market calls this year, specifically: 1) buying equities when markets sold-off sharply in February; and, 2) taking profits on some positions in August and holding the proceeds in cash. As a result, the performance of those portfolios that have been invested with us for the full year have been meaningfully ahead of market returns.

To be precise, as of yesterday’s close a “market portfolio” owning a mix of the TSX and S&P 500 would have been down about 10% for 2018. By contrast, those of you with entirely equity portfolios have experienced returns of down only ~3%, while those of you with some allocation to fixed income have returns ranging from +2% (Conservative) to flat (Balanced/Growth). As always, return numbers are net.

These percentages change every day, so I would suggest that the key takeaway here is not the absolute returns, but rather that our portfolios are performing well on a relative basis and that their risk profile has acted in a superior fashion during a sharp sell-off.

As a modest additional benefit, we have taken advantage of the market decline to swap some holdings within the portfolio to create tax losses as a result. Your accountant will be able to apply these to past capital gains in order to lower your tax bill or to capture a refund for you. Failing that, the losses can be carried forward indefinitely to shield you from future capital gains.

What is 2019 likely to hold:

The summary at the beginning of this email conveyed it well: the set-up for 2019 isn’t perfect, but it is very attractive.

The starting point for this view is that the current risks are generally quantifiable, as described above. In addition, unemployment rates in the US, Canada, and most of developed Europe are at multi-decade lows. With consumer spending accounting for 70% of US GDP, an unemployment rate below 4% makes the risk of a recession appear remote. Adding to this is the fact that banks globally are as well capitalized as they have been since the Great Depression; and that the stimulus benefits of this year’s US tax cut will continue well into 2019.

That said, there are a number of offsetting factors. In early 2019 we will face the likely conclusion of Brexit, a potential reigniting of the US-China trade war, and a possible further shut-down of US government operations. However, none of these issues are new at this point, suggesting that they may now be reasonably priced in to the market.

To that end, valuations have dropped significantly. The US tax cuts helping lead corporate earnings to grow by over 20% this year. Since the S&P 500’s price has fallen during the same period, the result is that the P/E ratio for the S&P has dropped from 20x to just under 16x. The P/E for the TSX is even lower, at less than 15x. These multiples are about average on a long-term historical basis, and have been consistent with subsequent double-digit equity returns, particularly in years where the global economy continues to grow.

Conclusion

As stated above, this email can be summarized in three main points:

1. This year your portfolio has meaningfully outperformed the market;

2. The recent sell-off is sharp, but it is easily within historical norms; and

3. The set-up for 2019 isn’t perfect, but it is very attractive.

Those of you interested in further reading can review RBC's official Investment Outlook for 2019. I am available to talk through the remainder of the Holidays, and as always would be delighted to speak with you about markets, your portfolio, and/or any financial items that are on your mind.

If we do not talk before, please expect to hear from us in the coming weeks to schedule your Annual Review, where applicable. In the meantime, all the best for the remainder of the Holiday stretch, and we look forward to sharing a prosperous 2019 with you.